Academic Profile

Statistics

Similar Authors

Papers on arXiv

Long-run covariance matrix estimation is the building block of time series inference. The corresponding difference-based estimator, which avoids detrending, has attracted considerable interest due t...

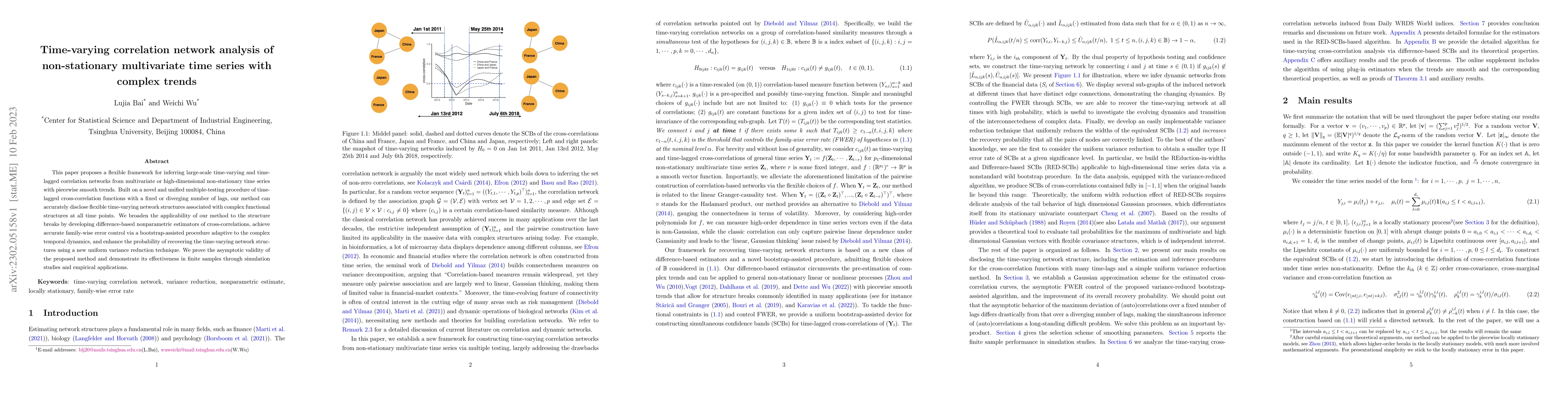

This paper proposes a flexible framework for inferring large-scale time-varying and time-lagged correlation networks from multivariate or high-dimensional non-stationary time series with piecewise s...

Diffusion probabilistic models (DPMs) have demonstrated a very promising ability in high-resolution image synthesis. However, sampling from a pre-trained DPM is time-consuming due to the multiple ev...

We consider the problem of testing for long-range dependence in time-varying coefficient regression models, where the covariates and errors are locally stationary, allowing complex temporal dynamics...

Multivariate locally stationary functional time series provide a flexible framework for modeling complex data structures exhibiting both temporal and spatial dependencies while allowing for time-varyi...

Most of the work on checking spherical symmetry assumptions on the distribution of the $p$-dimensional random vector $Y$ has its focus on statistical tests for the null hypothesis of exact spherical s...

This paper presents a systematic framework for controlling false discovery rate in learning time-varying correlation networks from high-dimensional, non-linear, non-Gaussian and non-stationary time se...

A crucial assumption to reduce computational complexity in spatial-temporal data analysis is separability, which factors the covariance structure into a purely spatial and a purely temporal component....