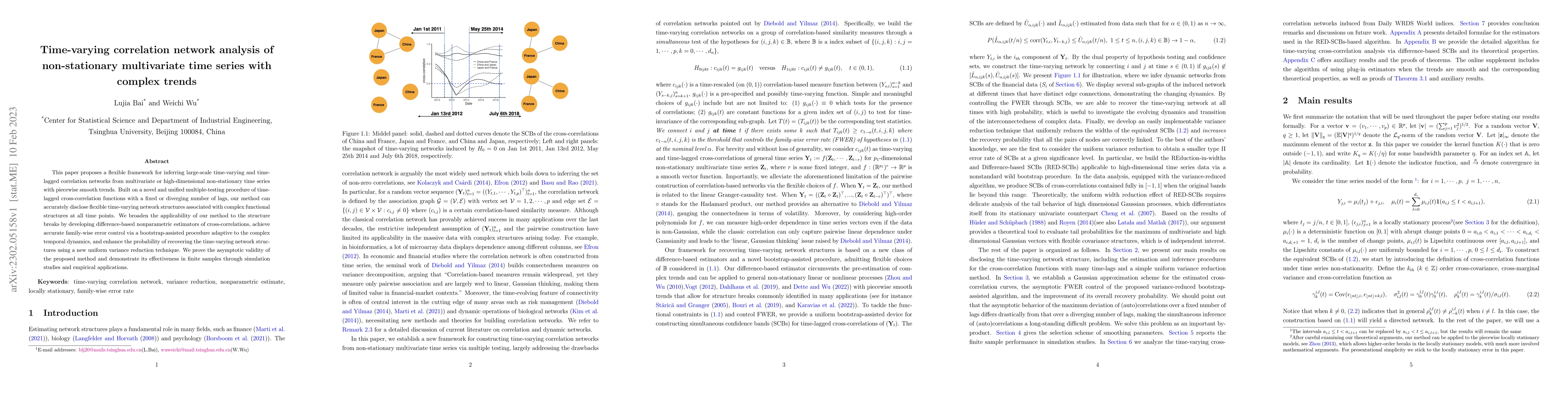

Time-varying correlation network analysis of non-stationary multivariate time series with complex trends

Publication

Metrics

AI Quick Summary

This paper introduces a framework for analyzing time-varying correlation networks from non-stationary multivariate time series, employing a novel multiple-testing procedure and variance reduction techniques to accurately infer dynamic network structures. The method is validated through simulations and real-world applications.

Paper Preview

Abstract

This paper proposes a flexible framework for inferring large-scale time-varying and time-lagged correlation networks from multivariate or high-dimensional non-stationary time series with piecewise smooth trends. Built on a novel and unified multiple-testing procedure of time-lagged cross-correlation functions with a fixed or diverging number of lags, our method can accurately disclose flexible time-varying network structures associated with complex functional structures at all time points. We broaden the applicability of our method to the structure breaks by developing difference-based nonparametric estimators of cross-correlations, achieve accurate family-wise error control via a bootstrap-assisted procedure adaptive to the complex temporal dynamics, and enhance the probability of recovering the time-varying network structures using a new uniform variance reduction technique. We prove the asymptotic validity of the proposed method and demonstrate its effectiveness in finite samples through simulation studies and empirical applications.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0