Academic Profile

Statistics

Similar Authors

Papers on arXiv

We propose a new and generic approach for detecting multiple change-points in general dependent data, termed random interval distillation (RID). By collecting random intervals with sufficient streng...

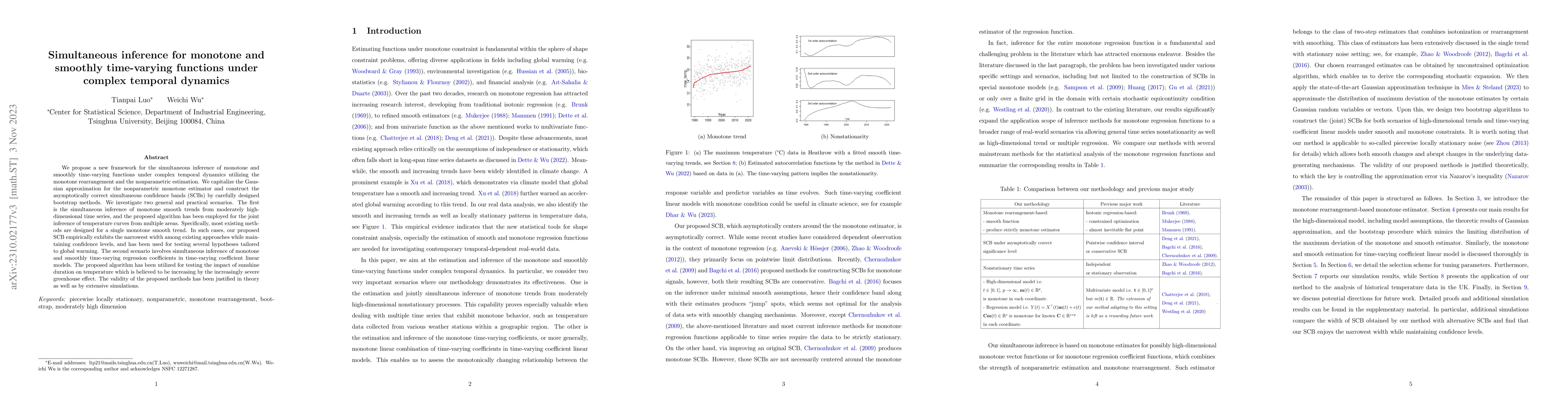

We propose a new framework for the simultaneous inference of monotone and smoothly time-varying functions under complex temporal dynamics utilizing the monotone rearrangement and the nonparametric e...

Contemporary time series data often feature objects connected by a social network that naturally induces temporal dependence involving connected neighbours. The network vector autoregressive model i...

Long-run covariance matrix estimation is the building block of time series inference. The corresponding difference-based estimator, which avoids detrending, has attracted considerable interest due t...

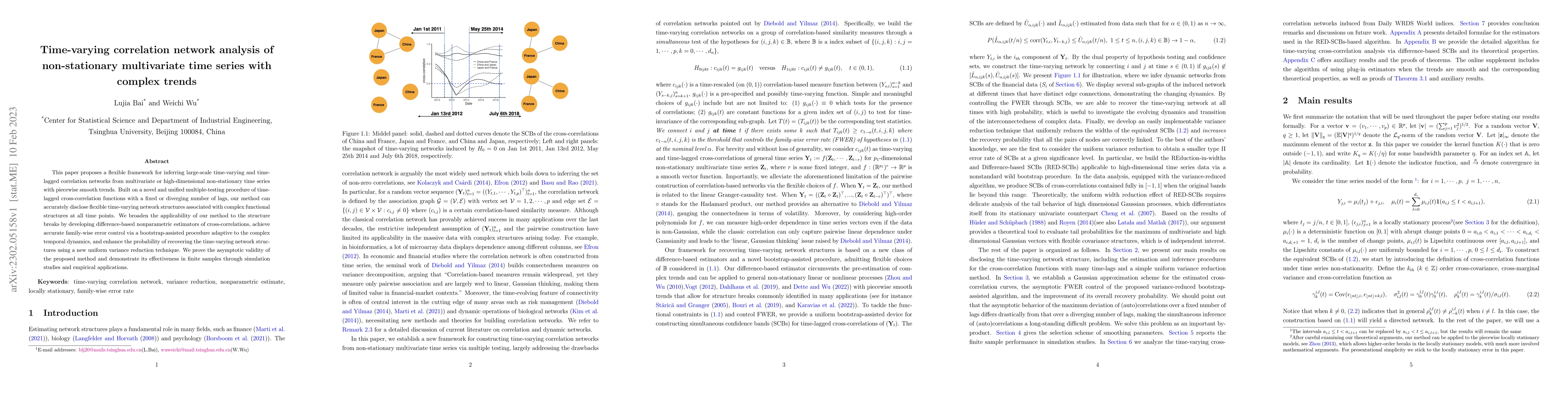

This paper proposes a flexible framework for inferring large-scale time-varying and time-lagged correlation networks from multivariate or high-dimensional non-stationary time series with piecewise s...

We consider the problem of testing for long-range dependence in time-varying coefficient regression models, where the covariates and errors are locally stationary, allowing complex temporal dynamics...

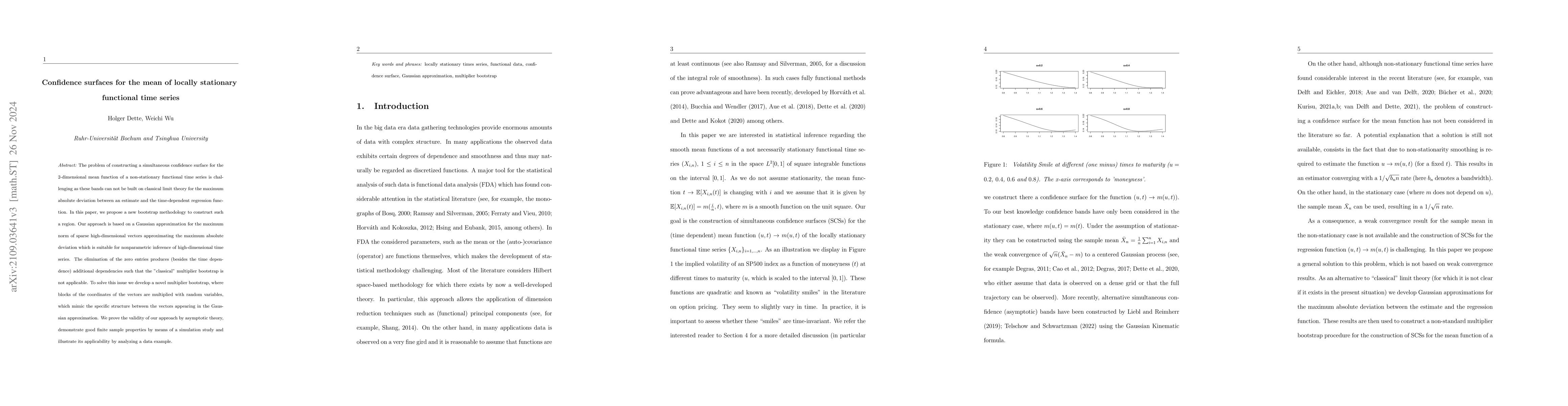

The problem of constructing a simultaneous confidence band for the mean function of a locally stationary functional time series $ \{ X_{i,n} (t) \}_{i = 1, \ldots, n}$ is challenging as these bands ...

This paper considers the estimation and testing of a class of locally stationary time series factor models with evolutionary temporal dynamics. In particular, the entries and the dimension of the fa...

This article investigates whether time-varying quantile regression curves are the same up to the horizontal shift or not. The errors and the covariates involved in the regression model are allowed t...

We propose a general framework for modelling network data that is designed to describe aspects of non-exchangeable networks. Conditional on latent (unobserved) variables, the edges of the network ar...

We develop an estimator for the high-dimensional covariance matrix of a locally stationary process with a smoothly varying trend and use this statistic to derive consistent predictors in non-station...

We consider the problem of detecting jumps in an otherwise smoothly evolving trend whilst the covariance and higher-order structures of the system can experience both smooth and abrupt changes over ...

This article studies the problem whether two convex (concave) regression functions modelling the relation between a response and covariate in two samples differ by a shift in the horizontal and/or v...

Most high dimensional changepoint detection methods assume the error process is stationary and changepoints occur synchronously across dimensions. The violation of these assumptions, which in applied ...

Multivariate locally stationary functional time series provide a flexible framework for modeling complex data structures exhibiting both temporal and spatial dependencies while allowing for time-varyi...

The graphon is a powerful framework for modeling large-scale networks, but its estimation remains a significant challenge. In this paper, we propose a novel approach that directly leverages a low-rank...

In randomized controlled trials without interference, regression adjustment is widely used to enhance the efficiency of treatment effect estimation. This paper extends this efficiency principle to set...

Fine-grained time series data are crucial for accurate and timely online change detection. While both collective anomalies and change points can coexist in such data, their joint online detection has ...

This paper presents a systematic framework for controlling false discovery rate in learning time-varying correlation networks from high-dimensional, non-linear, non-Gaussian and non-stationary time se...

Second-order characteristics including covariance and spectral density functions are fundamentally important for both statistical applications and theoretical analysis in functional time series. In th...

Quantile regression is a fundamental tool for distributional learning but poses significant optimization challenges for deep models due to the non-smoothness of the pinball loss. We propose ConquerNet...