Academic Profile

Statistics

Similar Authors

Papers on arXiv

Combining model-based and model-free reinforcement learning approaches, this paper proposes and analyzes an $\epsilon$-policy gradient algorithm for the online pricing learning task. The algorithm e...

We study the global convergence of a Fisher-Rao policy gradient flow for infinite-horizon entropy-regularised Markov decision processes with Polish state and action space. The flow is a continuous-t...

This report examines Artificial Intelligence (AI) in the financial sector, outlining its potential to revolutionise the industry and identify its challenges. It underscores the criticality of a well...

The emergence of price comparison websites (PCWs) has presented insurers with unique challenges in formulating effective pricing strategies. Operating on PCWs requires insurers to strike a delicate ...

Synthetic data has gained significant momentum thanks to sophisticated machine learning tools that enable the synthesis of high-dimensional datasets. However, many generation techniques do not give ...

Personal data collected at scale promises to improve decision-making and accelerate innovation. However, sharing and using such data raises serious privacy concerns. A promising solution is to produ...

This work uses the entropy-regularised relaxed stochastic control perspective as a principled framework for designing reinforcement learning (RL) algorithms. Herein agent interacts with the environm...

This explainer document aims to provide an overview of the current state of the rapidly expanding work on synthetic data technologies, with a particular focus on privacy. The article is intended for...

We study the global convergence of policy gradient for infinite-horizon, continuous state and action space, and entropy-regularized Markov decision processes (MDPs). We consider a softmax policy wit...

We develop a probabilistic framework for analysing model-based reinforcement learning in the episodic setting. We then apply it to study finite-time horizon stochastic control problems with linear d...

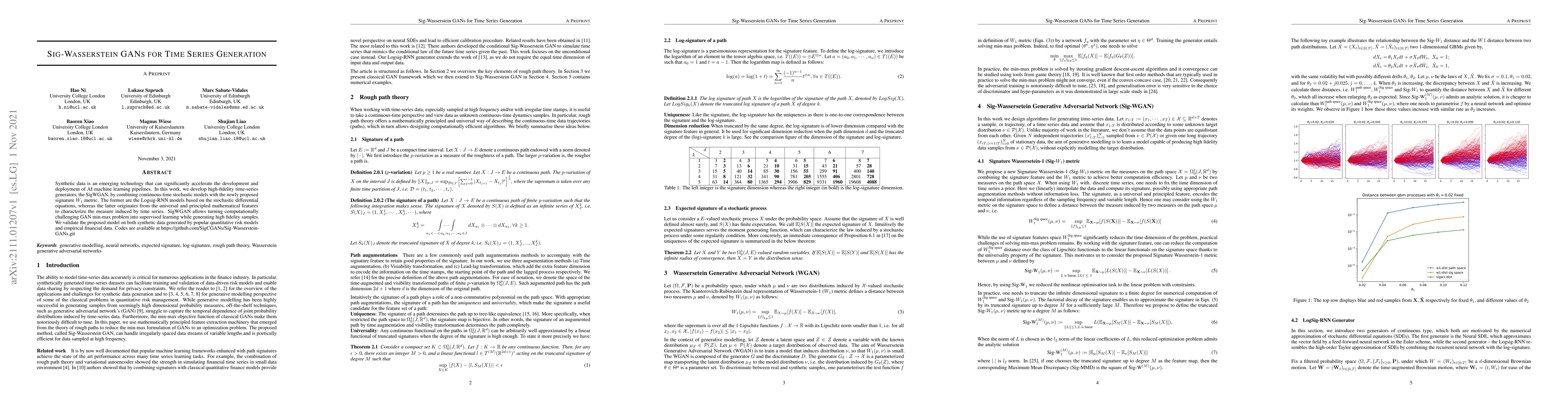

Synthetic data is an emerging technology that can significantly accelerate the development and deployment of AI machine learning pipelines. In this work, we develop high-fidelity time-series generat...

Inverse reinforcement learning attempts to reconstruct the reward function in a Markov decision problem, using observations of agent actions. As already observed in Russell [1998] the problem is ill...

Machine learning models are increasingly used in a wide variety of financial settings. The difficulty of understanding the inner workings of these systems, combined with their wide applicability, ha...

Using a combination of recurrent neural networks and signature methods from the rough paths theory we design efficient algorithms for solving parametric families of path dependent partial differenti...

Mathematical modelling is ubiquitous in the financial industry and drives key decision processes. Any given model provides only a crude approximation to reality and the risk of using an inadequate m...

Generative adversarial networks (GANs) have been extremely successful in generating samples, from seemingly high dimensional probability measures. However, these methods struggle to capture the temp...

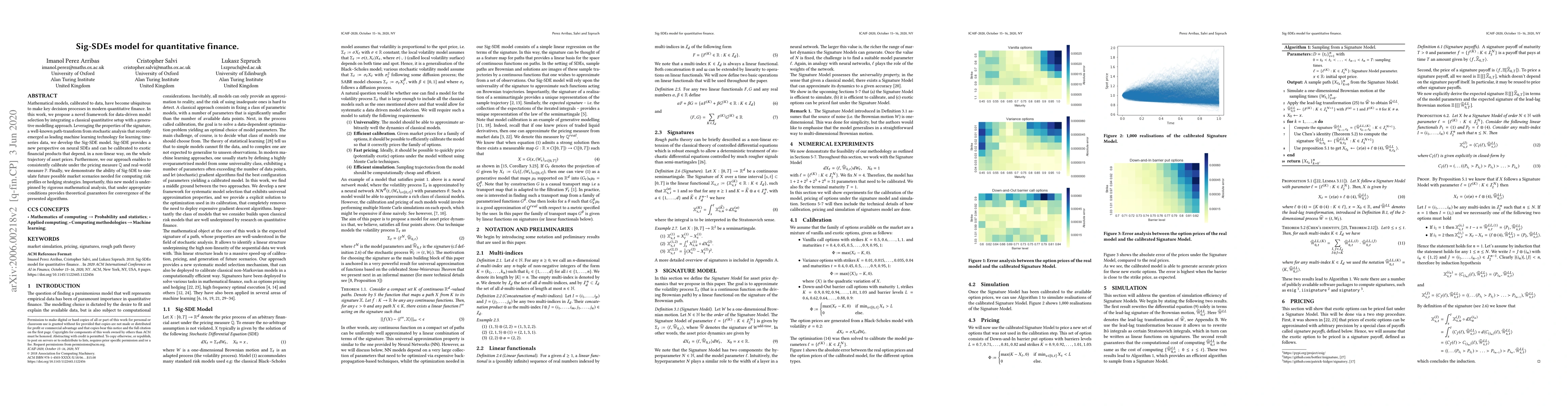

Mathematical models, calibrated to data, have become ubiquitous to make key decision processes in modern quantitative finance. In this work, we propose a novel framework for data-driven model select...

In this paper, we present a generic methodology for the efficient numerical approximation of the density function of the McKean-Vlasov SDEs. The weak error analysis for the projected process motivat...

Our work is motivated by a desire to study the theoretical underpinning for the convergence of stochastic gradient type algorithms widely used for non-convex learning tasks such as training of neura...

Consider the metric space $(\mathcal{P}_2(\mathbb{R}^d),W_2)$ of square integrable laws on $\mathbb{R}^d$ with the topology induced by the 2-Wasserstein distance $W_2$. Let $\Phi: \mathcal{P}_2( \ma...

We develop several deep learning algorithms for approximating families of parametric PDE solutions. The proposed algorithms approximate solutions together with their gradients, which in the context ...

Discrete time analogues of ergodic stochastic differential equations (SDEs) are one of the most popular and flexible tools for sampling high-dimensional probability measures. Non-asymptotic analysis...

We prove the existence of weak solutions to McKean-Vlasov SDEs defined on a domain $D \subseteq \mathbb{R}^d$ with continuous and unbounded coefficients that satisfy Lyapunov type conditions, where ...

We study the loan contracts offered by decentralised loan protocols (DLPs) through the lens of financial derivatives. DLPs, which effectively are clearinghouses, facilitate transactions between option...

We analyse the regret arising from learning the price sensitivity parameter $\kappa$ of liquidity takers in the ergodic version of the Avellaneda-Stoikov market making model. We show that a learning a...

In this work we study the numerical approximation of a class of ergodic Backward Stochastic Differential Equations. These equations are formulated in an infinite horizon framework and provide a probab...

Counterfactual explanations for black-box models aim to pr ovide insight into an algorithmic decision to its recipient. For a binary classification problem an individual counterfactual details which f...

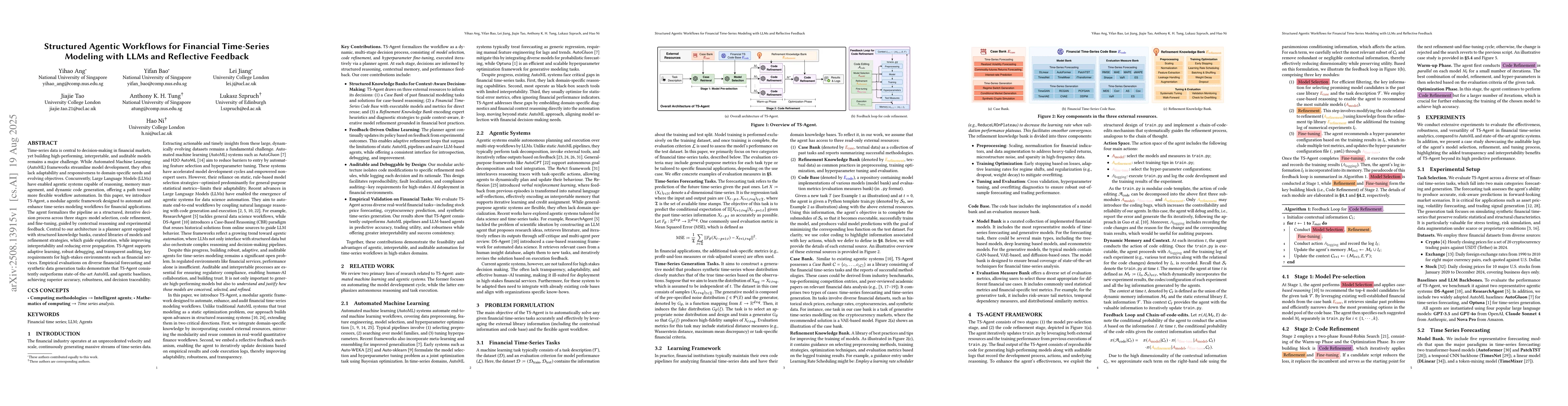

Time-series data is central to decision-making in financial markets, yet building high-performing, interpretable, and auditable models remains a major challenge. While Automated Machine Learning (Auto...

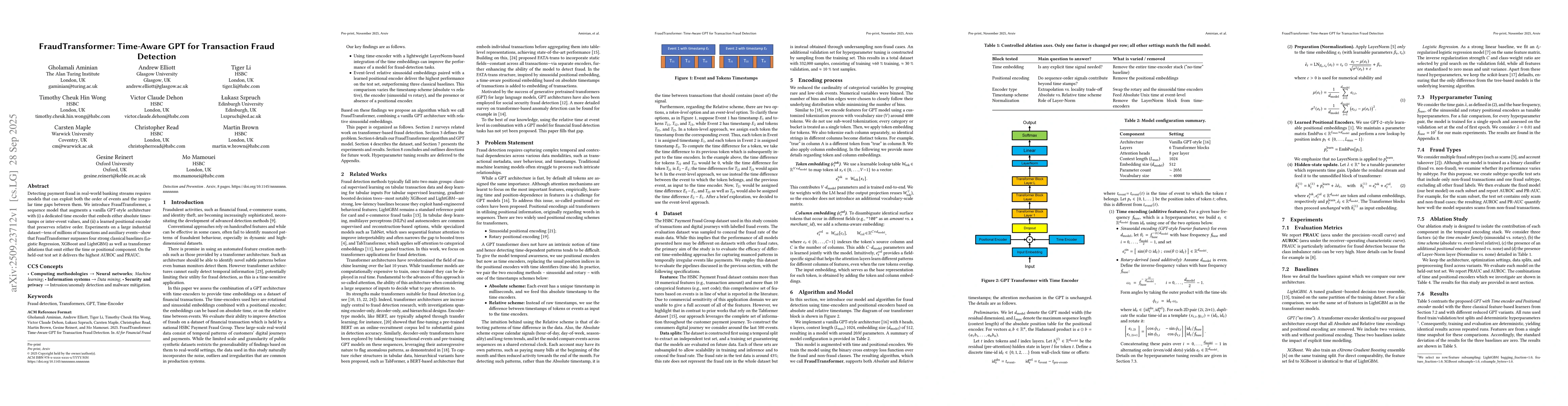

Detecting payment fraud in real-world banking streams requires models that can exploit both the order of events and the irregular time gaps between them. We introduce FraudTransformer, a sequence mode...

We prove the stability and global convergence of a coupled actor-critic gradient flow for infinite-horizon and entropy-regularised Markov decision processes (MDPs) in continuous state and action space...

We provide theoretical guarantees for convergence of discrete-time policy mirror descent with inexact advantage functions updated using temporal difference (TD) learning for entropy regularised MDPs i...

We study the global convergence of policy gradient for infinite-horizon entropy-regularized Markov decision processes (MDPs) with continuous state and action spaces. We consider log-linear softmax pol...

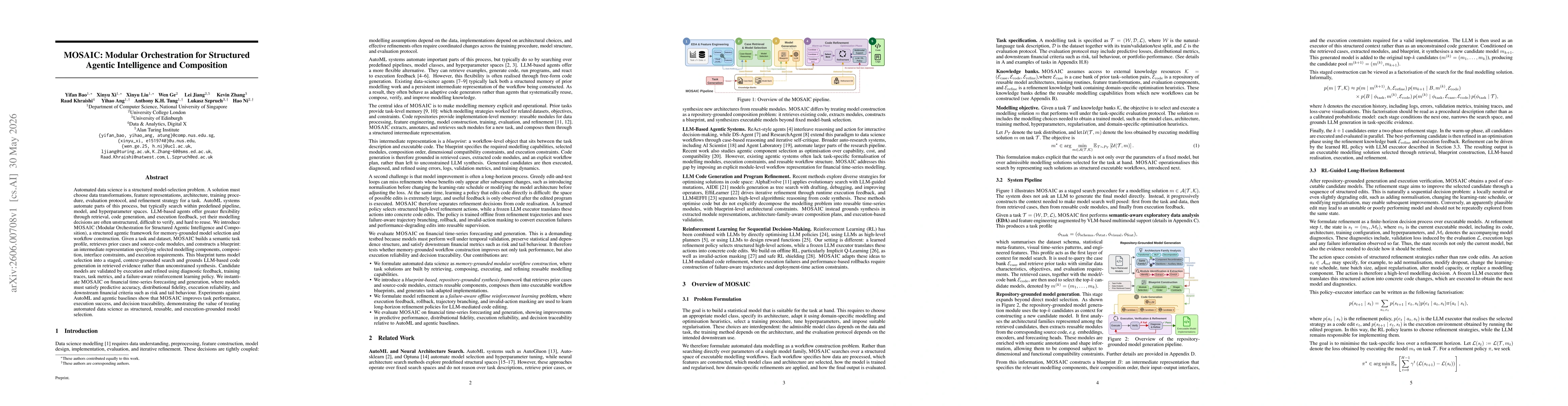

Automated data science is a structured model-selection problem. A solution must choose data transformations, feature representations, architecture, training procedure, evaluation protocol, and refinem...

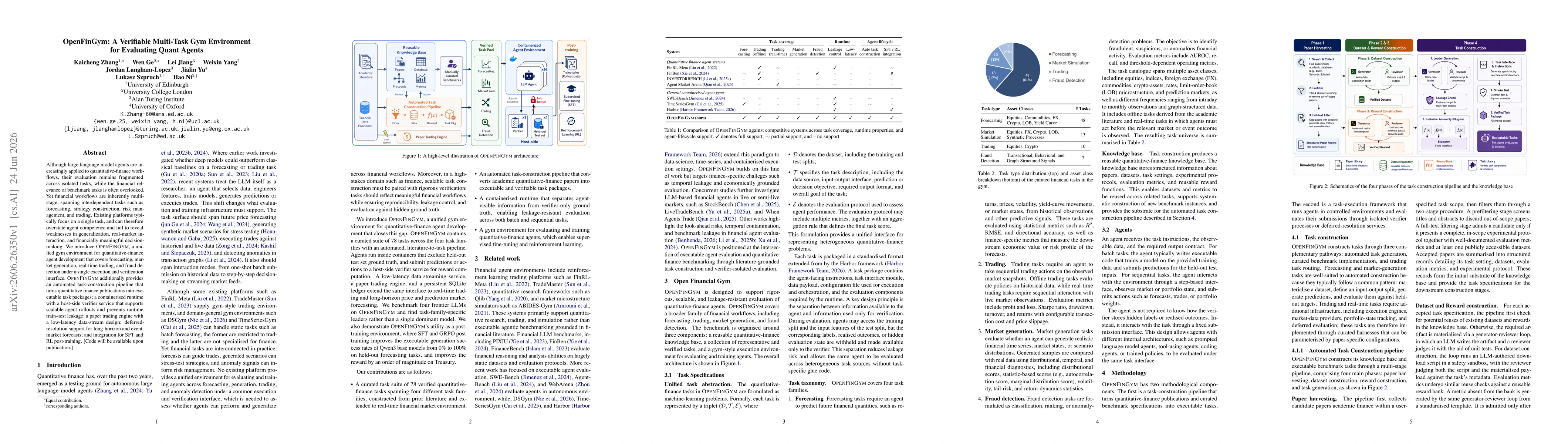

Although large language model agents are increasingly applied to quantitative-finance workflows, their evaluation remains fragmented across isolated tasks, while the financial relevance of benchmark t...

From maritime trade to commercial nuclear power, insurance has been the enabler of major economic and technological developments by pricing risk, limiting downside, and spreading best practices. The e...