Academic Profile

Statistics

Similar Authors

Papers on arXiv

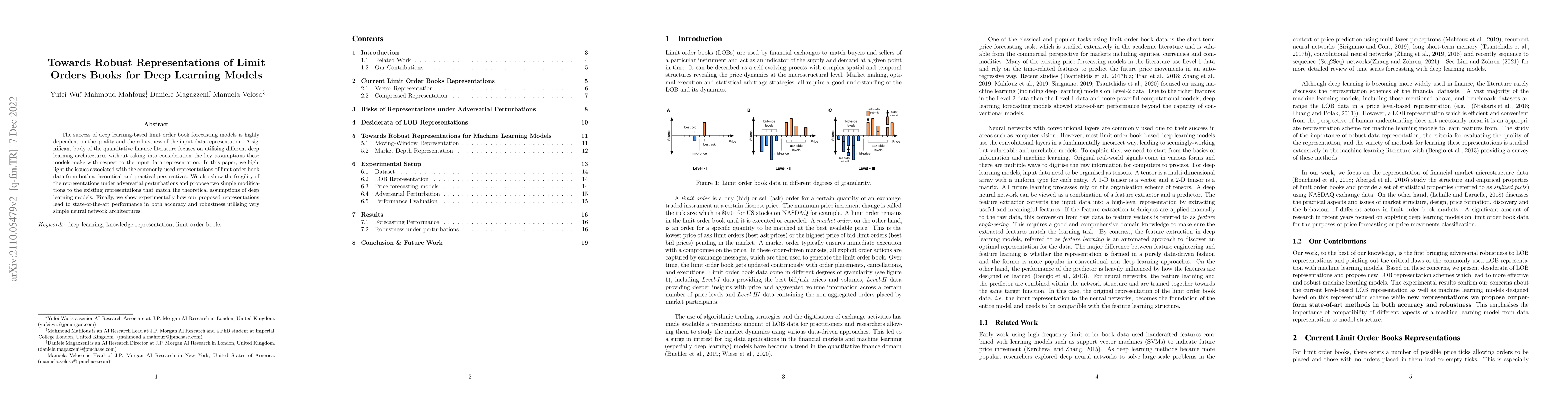

The success of deep learning-based limit order book forecasting models is highly dependent on the quality and the robustness of the input data representation. A significant body of the quantitative ...

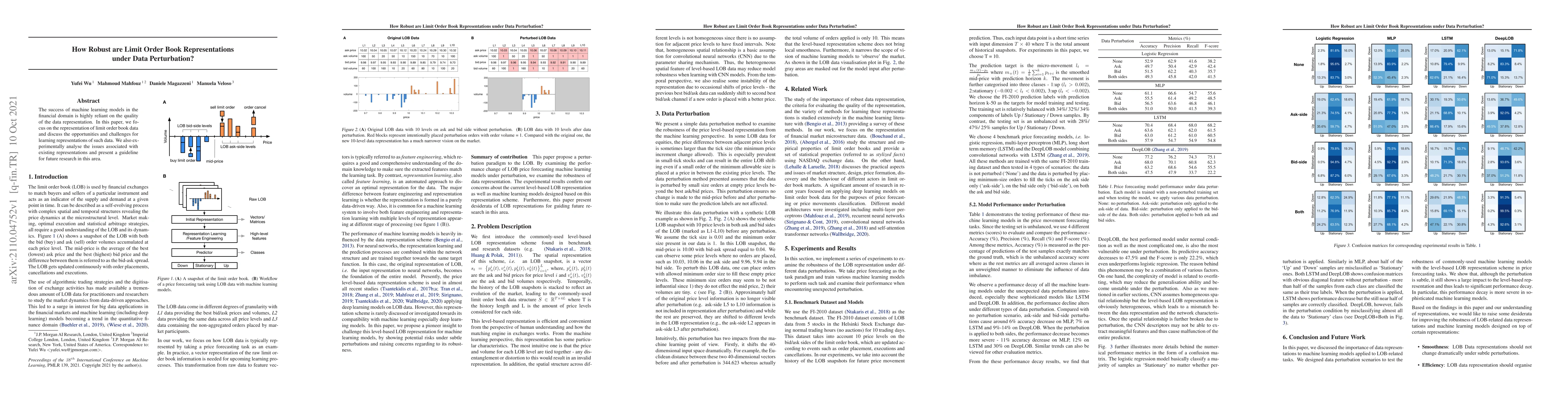

The success of machine learning models in the financial domain is highly reliant on the quality of the data representation. In this paper, we focus on the representation of limit order book data and...

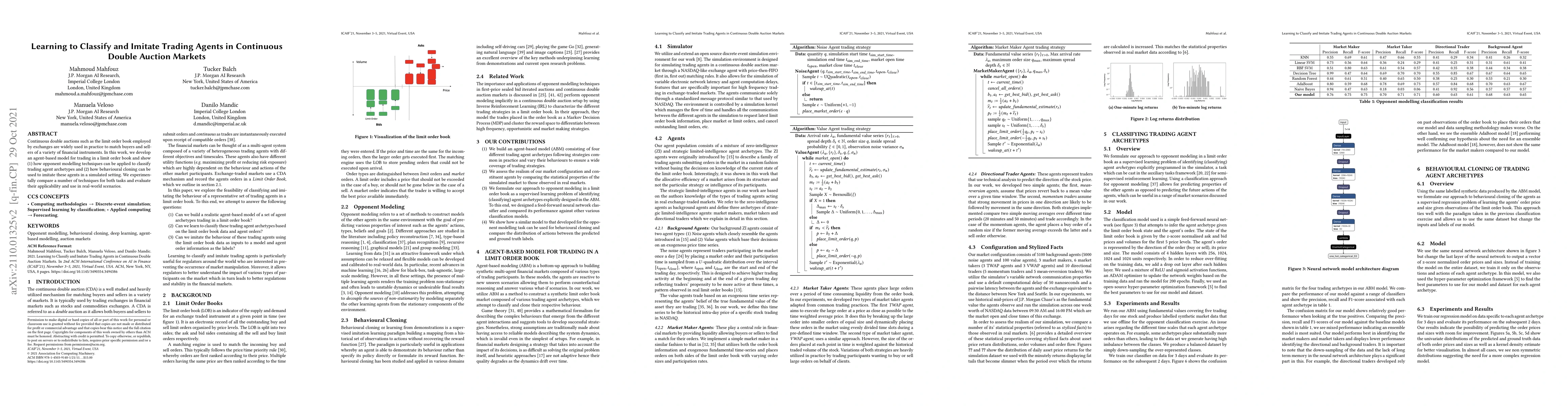

Continuous double auctions such as the limit order book employed by exchanges are widely used in practice to match buyers and sellers of a variety of financial instruments. In this work, we develop ...

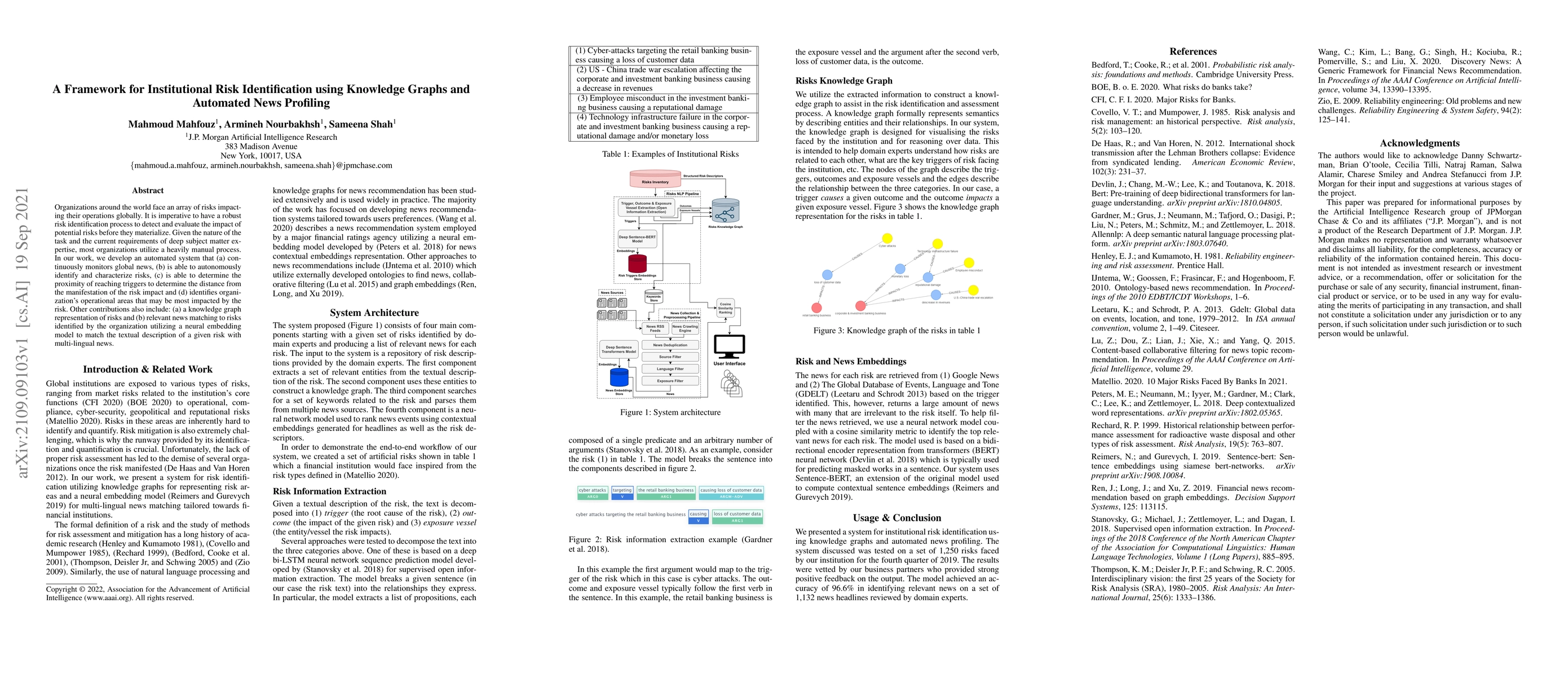

Organizations around the world face an array of risks impacting their operations globally. It is imperative to have a robust risk identification process to detect and evaluate the impact of potentia...

Machine learning (especially reinforcement learning) methods for trading are increasingly reliant on simulation for agent training and testing. Furthermore, simulation is important for validation of...

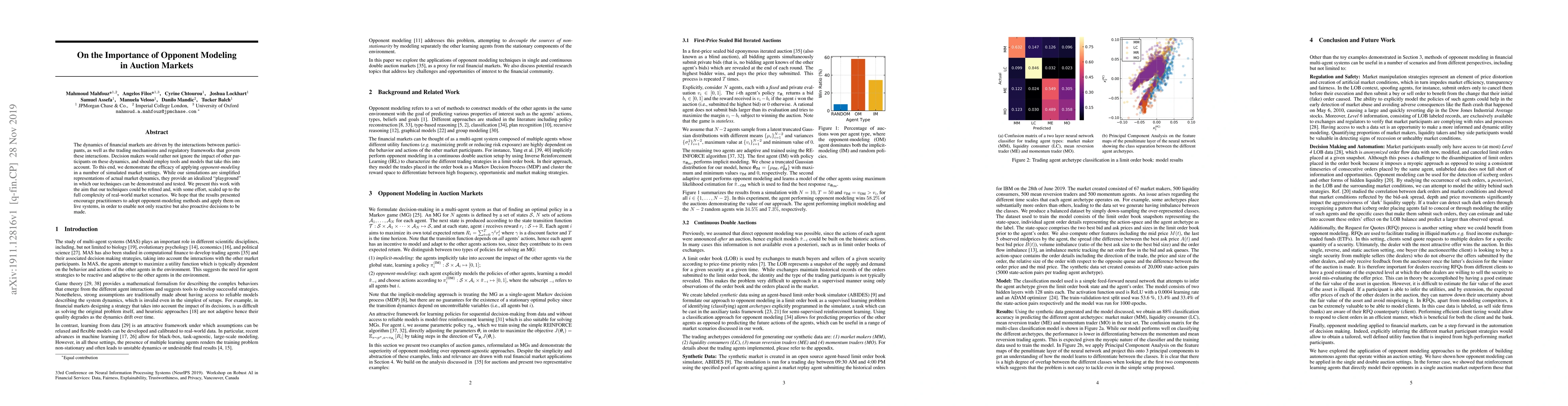

The dynamics of financial markets are driven by the interactions between participants, as well as the trading mechanisms and regulatory frameworks that govern these interactions. Decision-makers wou...

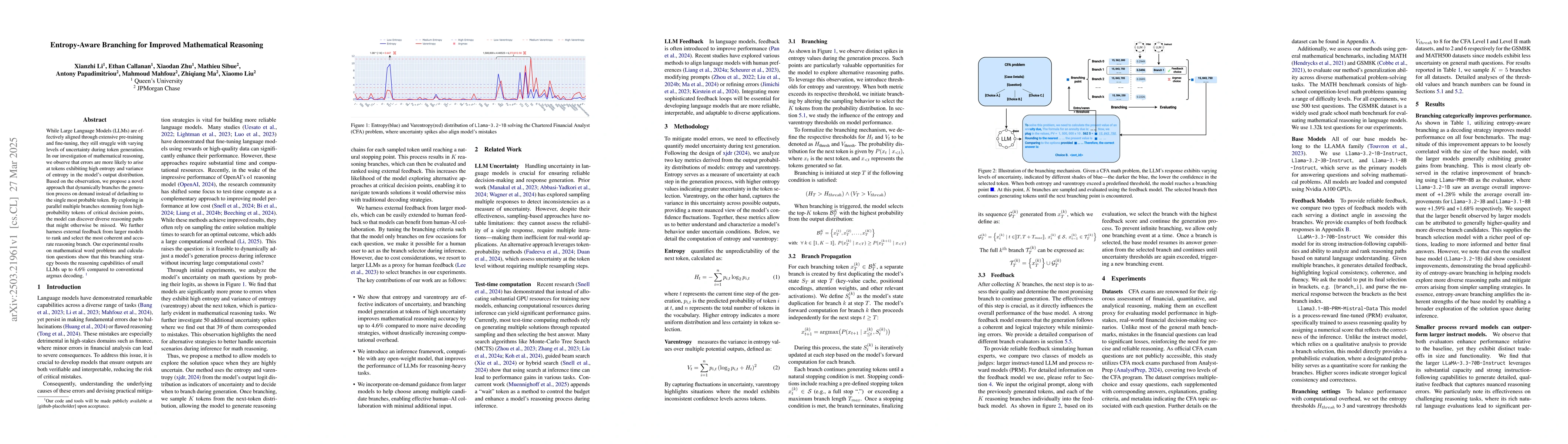

While Large Language Models (LLMs) are effectively aligned through extensive pre-training and fine-tuning, they still struggle with varying levels of uncertainty during token generation. In our invest...

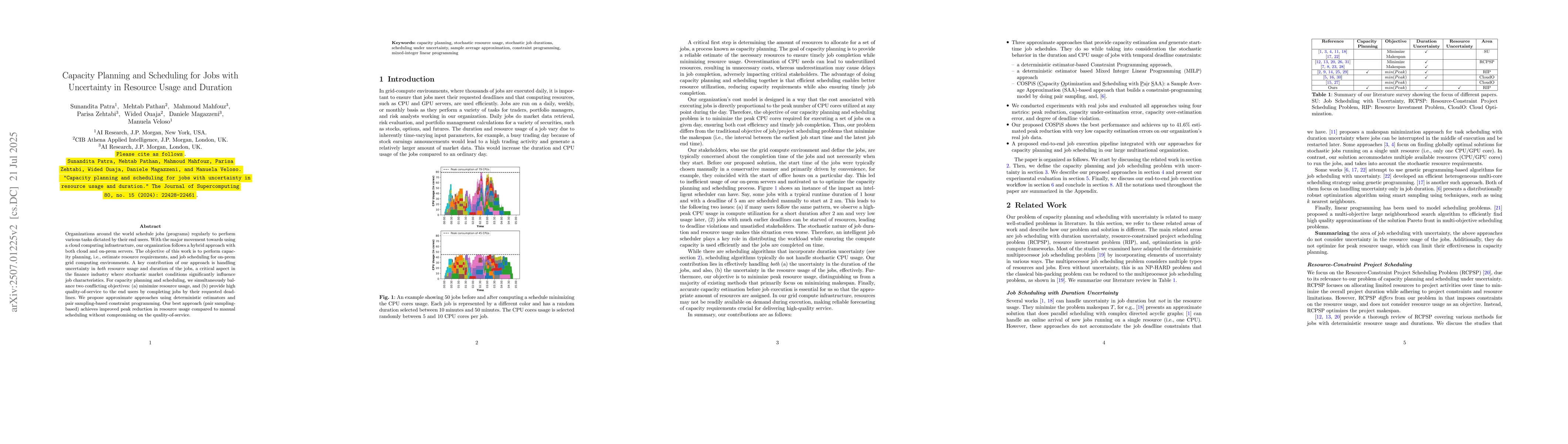

Organizations around the world schedule jobs (programs) regularly to perform various tasks dictated by their end users. With the major movement towards using a cloud computing infrastructure, our orga...

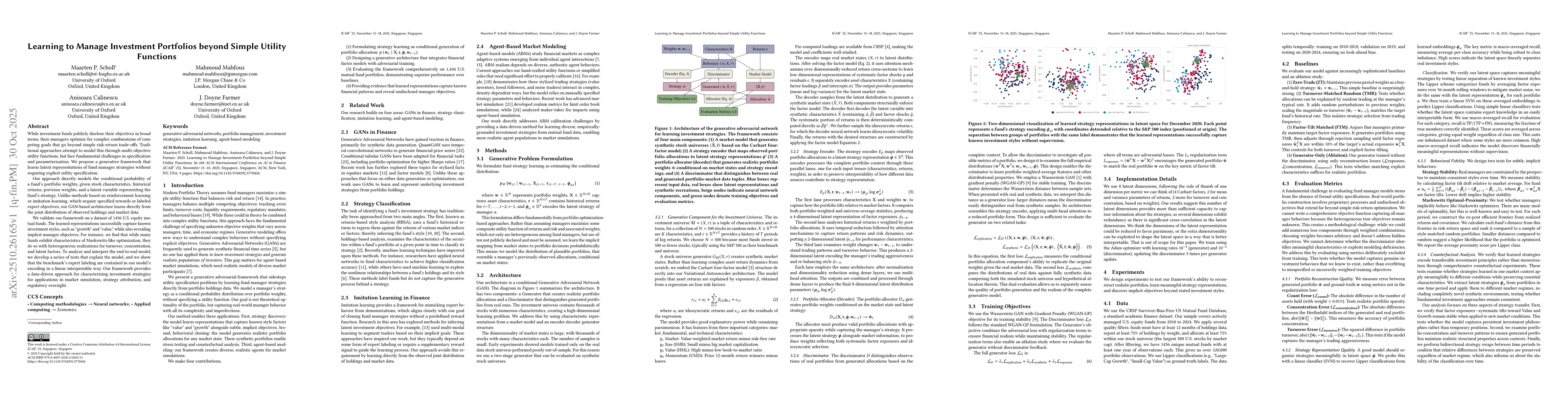

While investment funds publicly disclose their objectives in broad terms, their managers optimize for complex combinations of competing goals that go beyond simple risk-return trade-offs. Traditional ...