Academic Profile

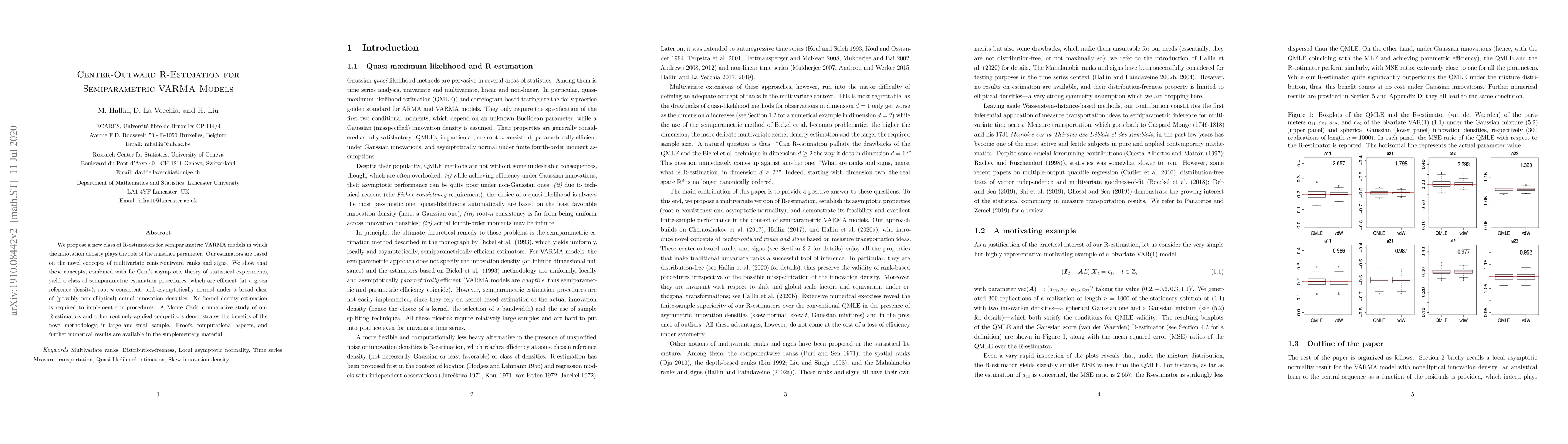

Statistics

Similar Authors

Papers on arXiv

We propose a family of tests of the validity of the assumptions underlying independent component analysis methods. The tests are formulated as L2-type procedures based on characteristic functions an...

Quantiles are a fundamental concept in probability and theoretical statistics and a daily tool in their applications. While the univariate concept of quantiles is quite clear and well understood, it...

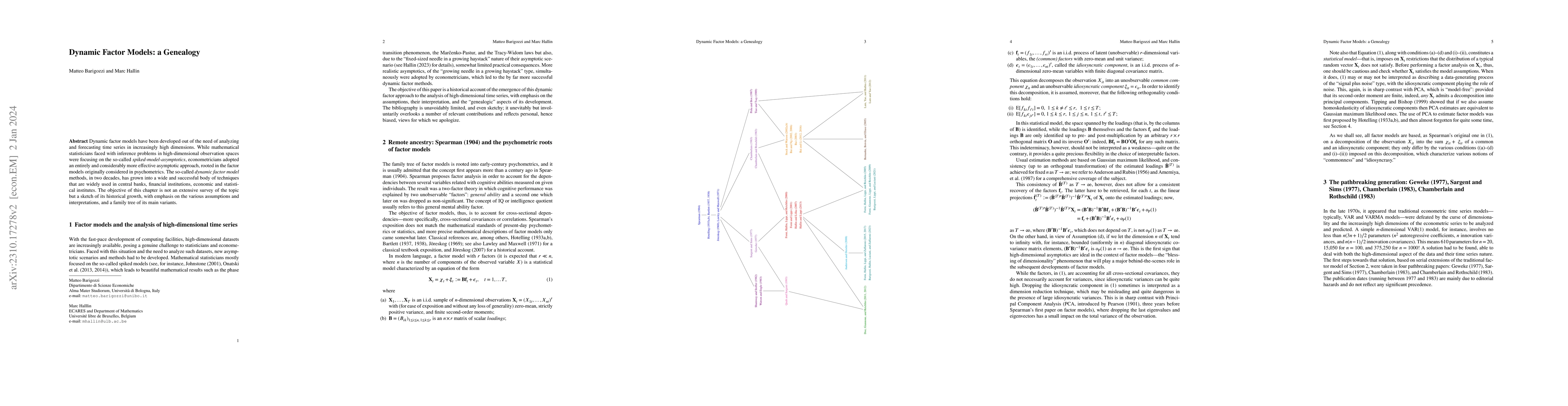

Dynamic factor models have been developed out of the need of analyzing and forecasting time series in increasingly high dimensions. While mathematical statisticians faced with inference problems in ...

The classical concept of bounded completeness and its relation to sufficiency and ancillarity play a fundamental role in unbiased estimation, unbiased testing, and the validity of inference in the p...

The contribution of this work is twofold. The first part deals with a Hilbert-space version of McCann's celebrated result on the existence and uniqueness of monotone measure-preserving maps: given t...

This paper proposes various nonparametric tools based on measure transportation for directional data. We use optimal transports to define new notions of distribution and quantile functions on the hy...

Based on measure transportation ideas and the related concepts of center-outward quantile functions, we propose multiple-output center-outward generalizations of the traditional univariate concepts ...

The pseudo-Gaussian portmanteau tests of Chitturi, Hosking, and Li and McLeod for VARMA models are revisited from a Le Cam perspective, providing a precise and more rigorous description of the asymp...

Based on the novel concept of multivariate center-outward quantiles introduced recently in Chernozhukov et al. (2017) and Hallin et al. (2021), we are considering the problem of nonparametric multip...

Frequency domain methods form a ubiquitous part of the statistical toolbox for time series analysis. In recent years, considerable interest has been given to the development of new spectral methodol...

Due to the lack of a canonical ordering in ${\mathbb R}^d$ for $d>1$, defining multivariate generalizations of the classical univariate ranks has been a long-standing open problem in statistics. Opt...

Extending to dimension 2 and higher the dual univariate concepts of ranks and quantiles has remained an open problem for more than half a century. Based on measure transportation results, a solution...

We develop a class of tests for semiparametric vector autoregressive (VAR) models with unspecified innovation densities, based on the recent measure-transportation-based concepts of multivariate {\i...

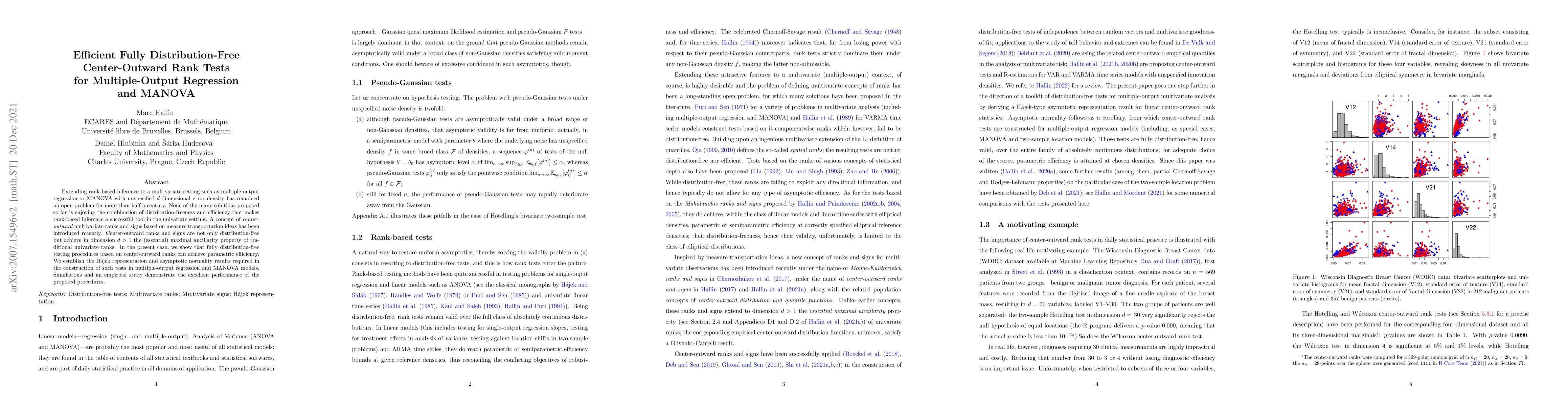

Extending rank-based inference to a multivariate setting such as multiple-output regression or MANOVA with unspecified d-dimensional error density has remained an open problem for more than half a c...

Goodness-of-fit tests based on the empirical Wasserstein distance are proposed for simple and composite null hypotheses involving general multivariate distributions. For group families, the procedur...

We consider a class of M-estimators of the parameters of a GARCH (p,q) model. These estimators involve score functions and, for adequate choices of the score functions, are asymptotically normal und...

We provide sufficient conditions under which the center-outward distribution and quantile functions introduced in Chernozhukov et al.~(2017) and Hallin~(2017) are homeomorphisms, thereby extending a...

All multivariate extensions of the univariate theory of risk measurement run into the same fundamental problem of the absence, in dimension d > 1, of a canonical ordering of Rd. Based on measure tra...

Although the assumption of elliptical symmetry is quite common in multivariate analysis and widespread in a number of applications, the problem of testing the null hypothesis of ellipticity so far h...

We propose a new class of R-estimators for semiparametric VARMA models in which the innovation density plays the role of the nuisance parameter. Our estimators are based on the novel concepts of mul...

In this paper, we set up the theoretical foundations for a high-dimensional functional factor model approach in the analysis of large cross-sections (panels) of functional time series (FTS). We firs...

Volatilities, in high-dimensional panels of economic time series with a dynamic factor structure on the levels or returns, typically also admit a dynamic factor decomposition. We consider a two-stag...

Increased attention has been given recently to the statistical analysis of variables with values on nonlinear manifolds. A natural but nontrivial problem in that context is the definition of quantile ...

Time-reversibility is a crucial feature of many time series models, while time-irreversibility is the rule rather than the exception in real-life data. Testing the null hypothesis of time-reversibilty...

Several fundamental and closely interconnected issues related to factor models are reviewed and discussed: dynamic versus static loadings, rate-strong versus rate-weak factors, the concept of weakly c...

Prediction is a key issue in time series analysis. Just as classical mean regression models, classical autoregressive methods, yielding L$^2$ point-predictions, provide rather poor predictive summarie...

Restricting statistical experiments via nuisance-ancillary $σ$-fields yields nuisance-free experiments. However, a moot point with ancillarity is that maximal ancillary $σ$-fields are typically not un...