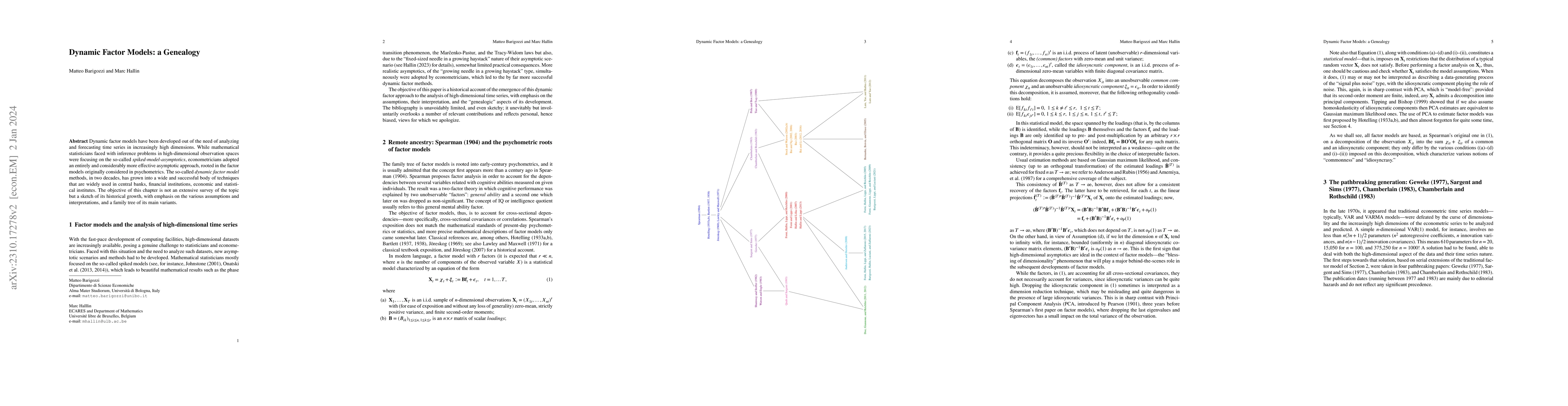

Dynamic factor models have been developed out of the need of analyzing and

forecasting time series in increasingly high dimensions. While mathematical

statisticians faced with inference problems in high-dimensional observation

spaces were focusing on the so-called spiked-model-asymptotics, econometricians

adopted an entirely and considerably more effective asymptotic approach, rooted

in the factor models originally considered in psychometrics. The so-called

dynamic factor model methods, in two decades, has grown into a wide and

successful body of techniques that are widely used in central banks, financial

institutions, economic and statistical institutes. The objective of this

chapter is not an extensive survey of the topic but a sketch of its historical

growth, with emphasis on the various assumptions and interpretations, and a

family tree of its main variants.

Discussion 0