Academic Profile

Statistics

Similar Authors

Papers on arXiv

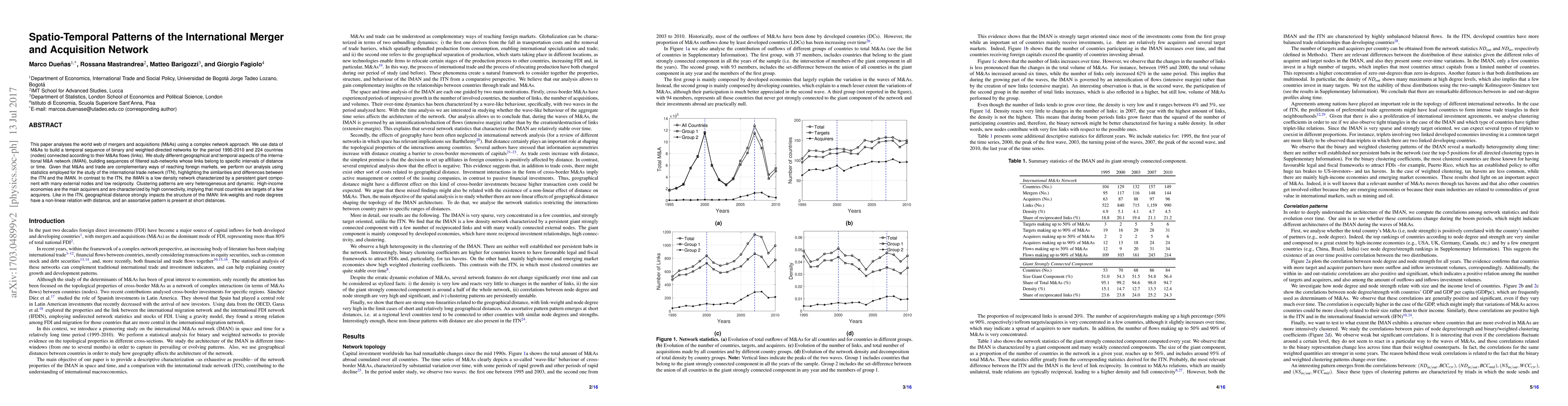

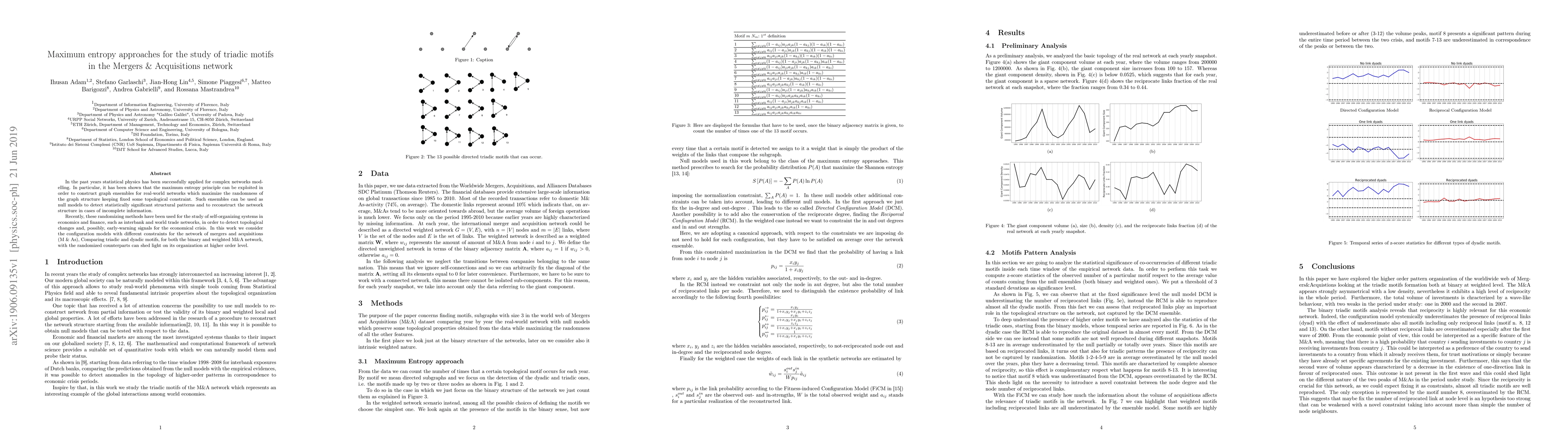

This paper analyses the world web of mergers and acquisitions (M&As) using a complex network approach. We use data of M&As to build a temporal sequence of binary and weighted-directed networks for t...

Motivated by the need for analysing large spatio-temporal panel data, we introduce a novel dimensionality reduction methodology for $n$-dimensional random fields observed across a number $S$ spatial...

Dynamic factor models have been developed out of the need of analyzing and forecasting time series in increasingly high dimensions. While mathematical statisticians faced with inference problems in ...

This paper investigates the properties of Quasi Maximum Likelihood estimation of an approximate factor model for an $n$-dimensional vector of stationary time series. We prove that the factor loading...

We introduce a new HD DCC-HEAVY class of hierarchical-type factor models for conditional covariance matrices of high-dimensional returns, employing the corresponding realized measures built from hig...

We consider (robust) inference in the context of a factor model for tensor-valued sequences. We study the consistency of the estimated common factors and loadings space when using estimators based o...

We review Quasi Maximum Likelihood estimation of factor models for high-dimensional panels of time series. We consider two cases: (1) estimation when no dynamic model for the factors is specified (B...

This paper generalises dynamic factor models for multidimensional dependent data. In doing so, it develops an interpretable technique to study complex information sources ranging from repeated surve...

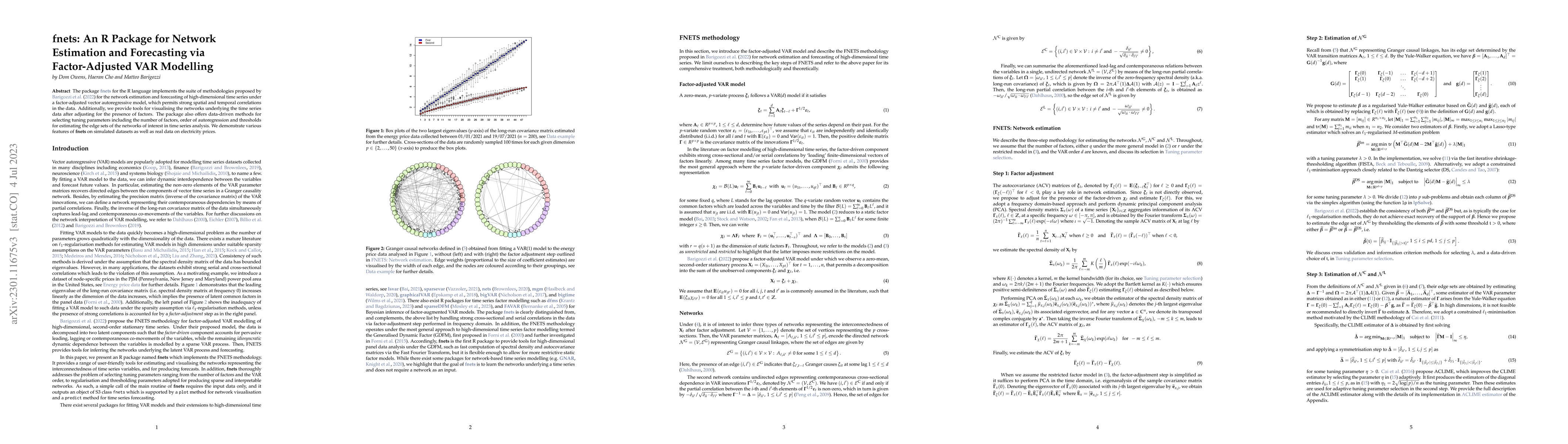

The package fnets for the R language implements the suite of methodologies proposed by Barigozzi et al. (2022) for the network estimation and forecasting of high-dimensional time series under a fact...

We provide an alternative derivation of the asymptotic results for the Principal Components estimator of a large approximate factor model. Results are derived under a minimal set of assumptions and,...

We study a novel large dimensional approximate factor model with regime changes in the loadings driven by a latent first order Markov process. By exploiting the equivalent linear representation of t...

We propose a factor network autoregressive (FNAR) model for time series with complex network structures. The coefficients of the model reflect many different types of connections between economic ag...

We propose FNETS, a methodology for network estimation and forecasting of high-dimensional time series exhibiting strong serial- and cross-sectional correlations. We operate under a factor-adjusted ...

We study inference on the common stochastic trends in a non-stationary, $N$-variate time series $y_{t}$, in the possible presence of heavy tails. We propose a novel methodology which does not requir...

We propose a new estimator of high-dimensional spectral density matrices, called UNshrunk ALgebraic Spectral Estimator (UNALSE), under the assumption of an underlying low rank plus sparse structure,...

This paper considers estimation of large dynamic factor models with common and idiosyncratic trends by means of the Expectation Maximization algorithm, implemented jointly with the Kalman smoother. ...

This paper studies Quasi Maximum Likelihood estimation of Dynamic Factor Models for large panels of time series. Specifically, we consider the case in which the autocorrelation of the factors is exp...

In the past years statistical physics has been successfully applied for complex networks modelling. In particular, it has been shown that the maximum entropy principle can be exploited in order to c...

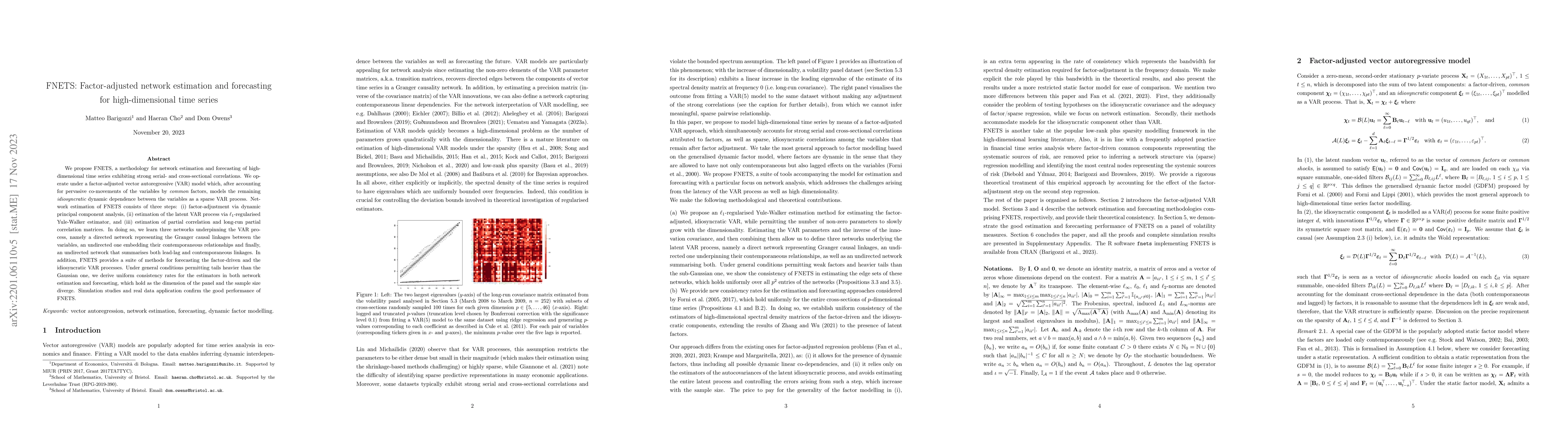

Volatilities, in high-dimensional panels of economic time series with a dynamic factor structure on the levels or returns, typically also admit a dynamic factor decomposition. We consider a two-stag...

We develop a monitoring procedure to detect changes in a large approximate factor model. Letting $r$ be the number of common factors, we base our statistics on the fact that the $\left( r+1\right) $...

We present and describe a new publicly available large dataset which encompasses quarterly and monthly macroeconomic time series for both the Euro Area (EA) as a whole and its ten primary member count...

The paper proposes a moving sum methodology for detecting multiple change points in high-dimensional time series under a factor model, where changes are attributed to those in loadings as well as emer...

We study the problem of factor modelling vector- and tensor-valued time series in the presence of heavy tails in the data, which produce anomalous observations with non-negligible probability. For thi...

Several fundamental and closely interconnected issues related to factor models are reviewed and discussed: dynamic versus static loadings, rate-strong versus rate-weak factors, the concept of weakly c...

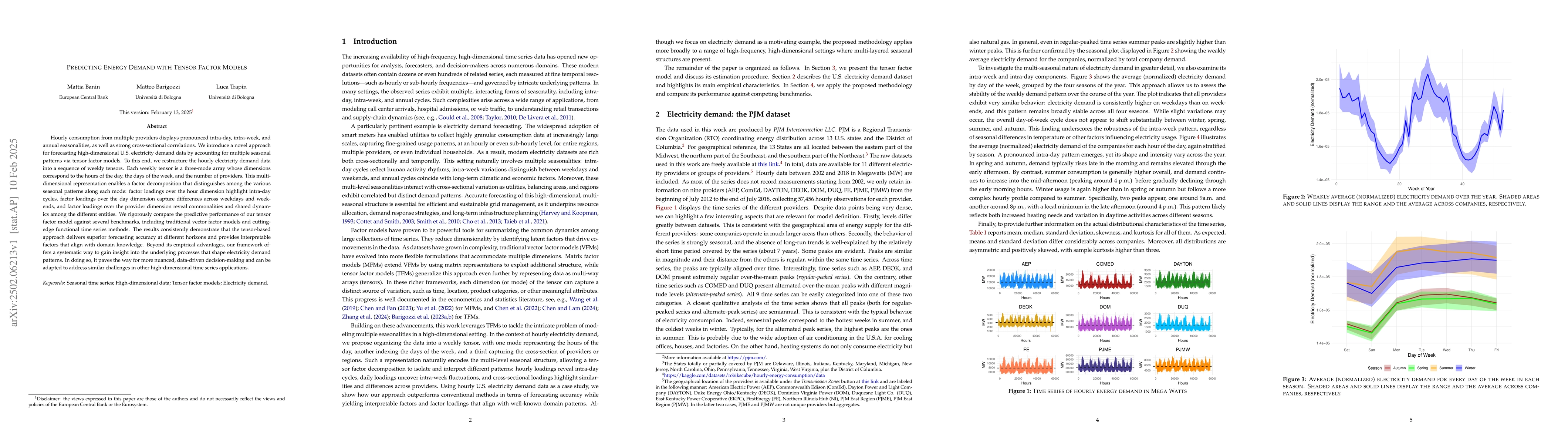

Hourly consumption from multiple providers displays pronounced intra-day, intra-week, and annual seasonalities, as well as strong cross-sectional correlations. We introduce a novel approach for foreca...

This paper considers an approximate dynamic matrix factor model that accounts for the time series nature of the data by explicitly modelling the time evolution of the factors. We study Quasi Maximum L...

We measure the Euro Area (EA) output gap and potential output using a non-stationary dynamic factor model estimated on a large dataset of macroeconomic and financial variables. From 2012 to 2024, we e...

Factor extraction from systems of variables with a large cross-sectional dimension, $N$, is often based on either Principal Components (PC)-based procedures, or Kalman filter (KF)-based procedures. Me...