Academic Profile

Statistics

Similar Authors

Papers on arXiv

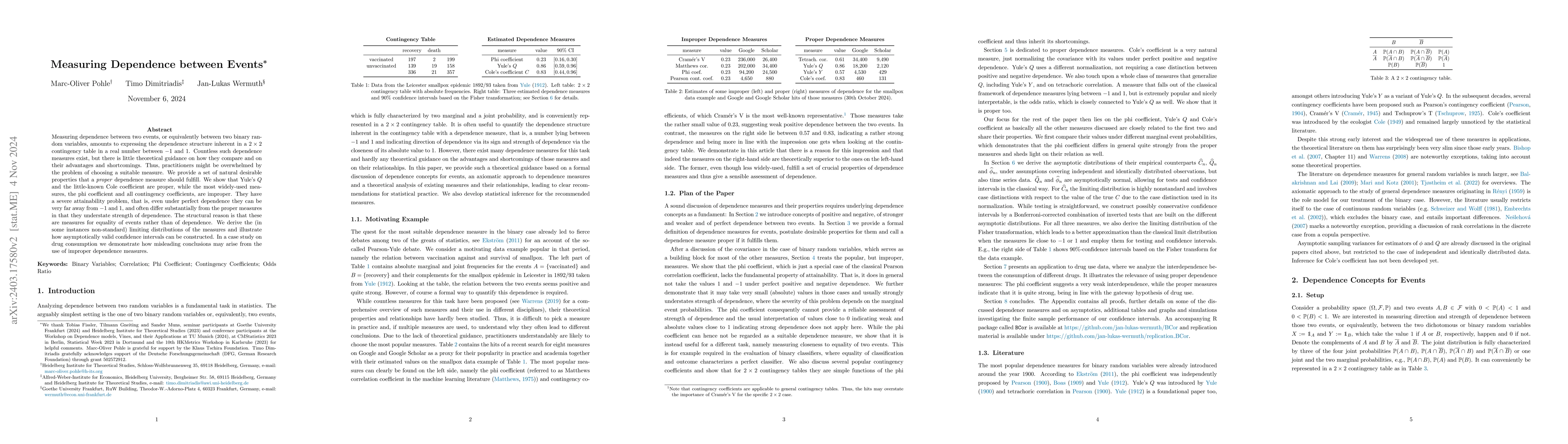

Measuring dependence between two events, or equivalently between two binary random variables, amounts to expressing the dependence structure inherent in a $2\times 2$ contingency table in a real num...

The covariance of two random variables measures the average joint deviations from their respective means. We generalise this well-known measure by replacing the means with other statistical function...

Quantile forecasts made across multiple horizons have become an important output of many financial institutions, central banks and international organisations. This paper proposes misspecification t...

Calibration tests based on the probability integral transform (PIT) are routinely used to assess the quality of univariate distributional forecasts. However, PIT-based calibration tests for multivar...

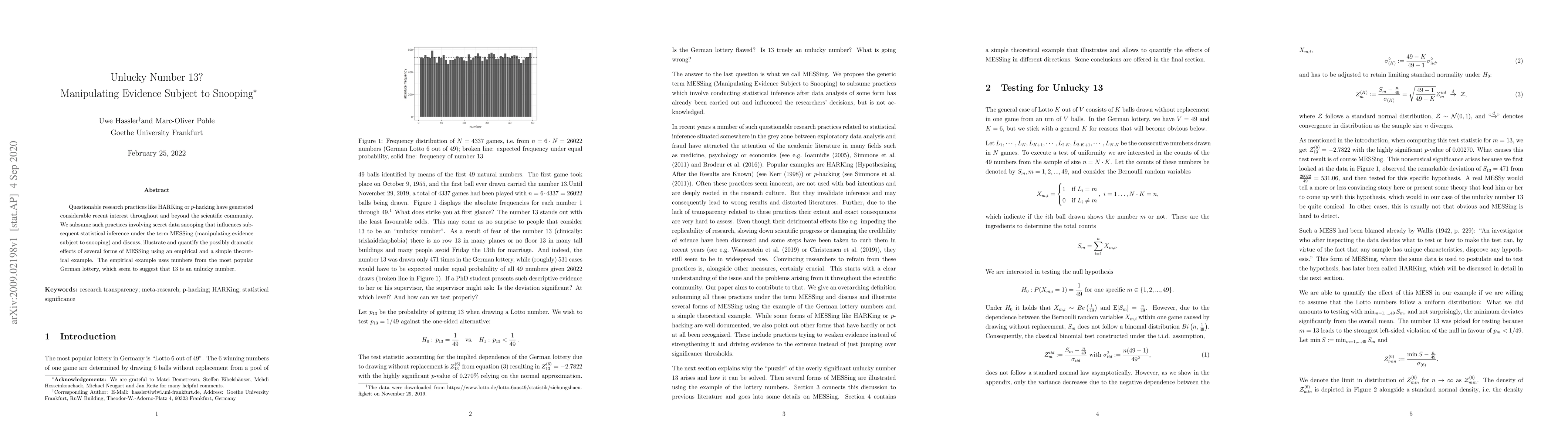

Questionable research practices like HARKing or p-hacking have generated considerable recent interest throughout and beyond the scientific community. We subsume such practices involving secret data ...

I provide a unifying perspective on forecast evaluation, characterizing accurate forecasts of all types, from simple point to complete probabilistic forecasts, in terms of two fundamental underlying...

Long memory in the sense of slowly decaying autocorrelations is a stylized fact in many time series from economics and finance. The fractionally integrated process is the workhorse model for the ana...

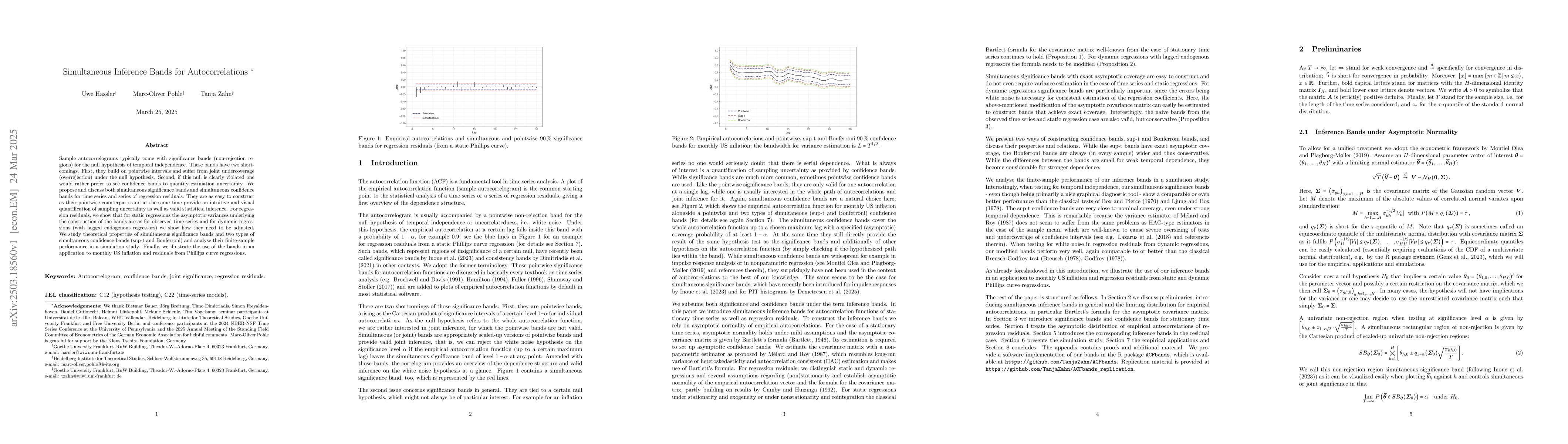

Sample autocorrelograms typically come with significance bands (non-rejection regions) for the null hypothesis of temporal independence. These bands have two shortcomings. First, they build on pointwi...

Kendall's tau and Spearman's rho are widely used tools for measuring dependence. Surprisingly, when it comes to asymptotic inference for these rank correlations, some fundamental results and methods h...

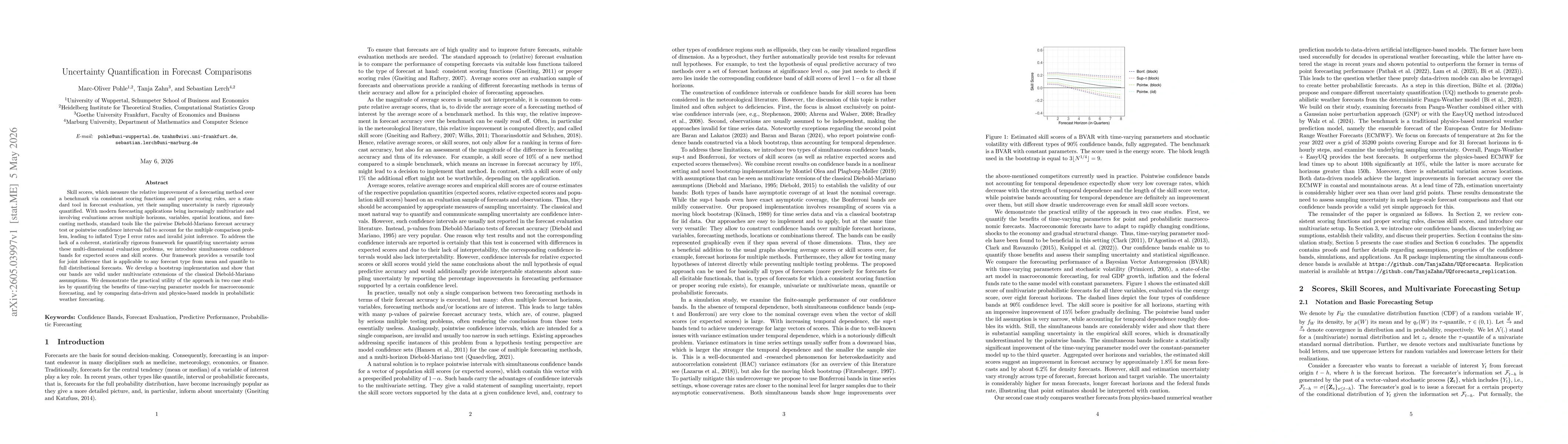

Skill scores, which measure the relative improvement of a forecasting method over a benchmark via consistent scoring functions and proper scoring rules, are a standard tool in forecast evaluation, yet...