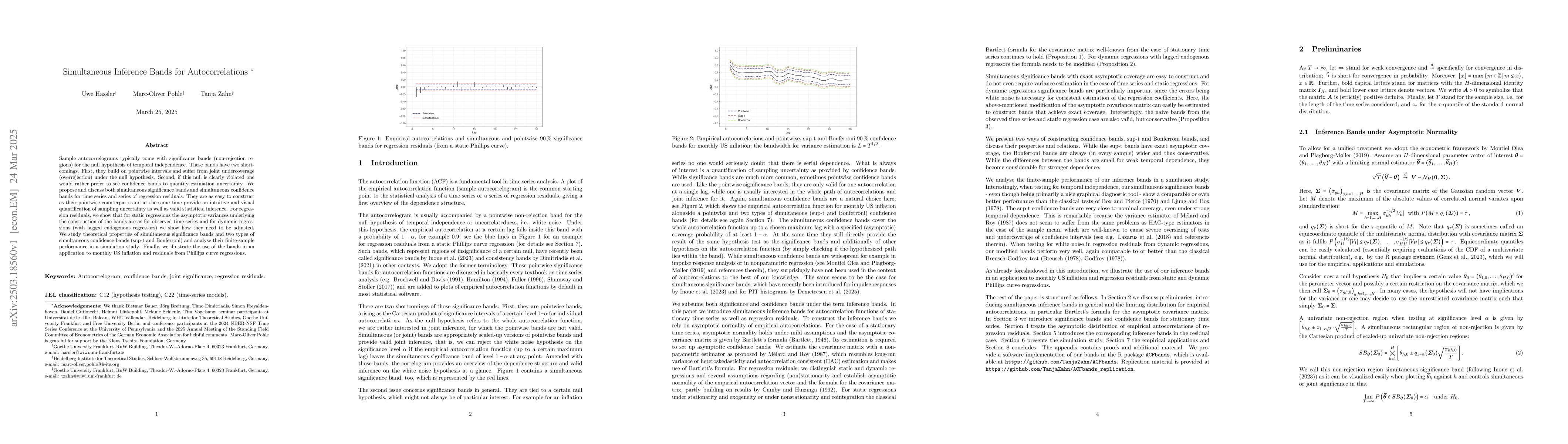

Sample autocorrelograms typically come with significance bands (non-rejection

regions) for the null hypothesis of temporal independence. These bands have two

shortcomings. First, they build on pointwise intervals and suffer from joint

undercoverage (overrejection) under the null hypothesis. Second, if this null

is clearly violated one would rather prefer to see confidence bands to quantify

estimation uncertainty. We propose and discuss both simultaneous significance

bands and simultaneous confidence bands for time series and series of

regression residuals. They are as easy to construct as their pointwise

counterparts and at the same time provide an intuitive and visual

quantification of sampling uncertainty as well as valid statistical inference.

For regression residuals, we show that for static regressions the asymptotic

variances underlying the construction of the bands are as for observed time

series and for dynamic regressions (with lagged endogenous regressors) we show

how they need to be adjusted. We study theoretical properties of simultaneous

significance bands and two types of simultaneous confidence bands (sup-t and

Bonferroni) and analyse their finite-sample performance in a simulation study.

Finally, we illustrate the use of the bands in an application to monthly US

inflation and residuals from Phillips curve regressions.

Discussion 0