Academic Profile

Statistics

Similar Authors

Papers on arXiv

The aim of this work is to propose an extension of the Deep BSDE solver by Han, E, Jentzen (2017) to the case of FBSDEs with jumps. As in the aforementioned solver, starting from a discretized versi...

In this paper, we derive a representation for the value process associated to the solutions of FBSDEs in a jump-diffusion setting under multiple probability measures. Motivated by concrete financial...

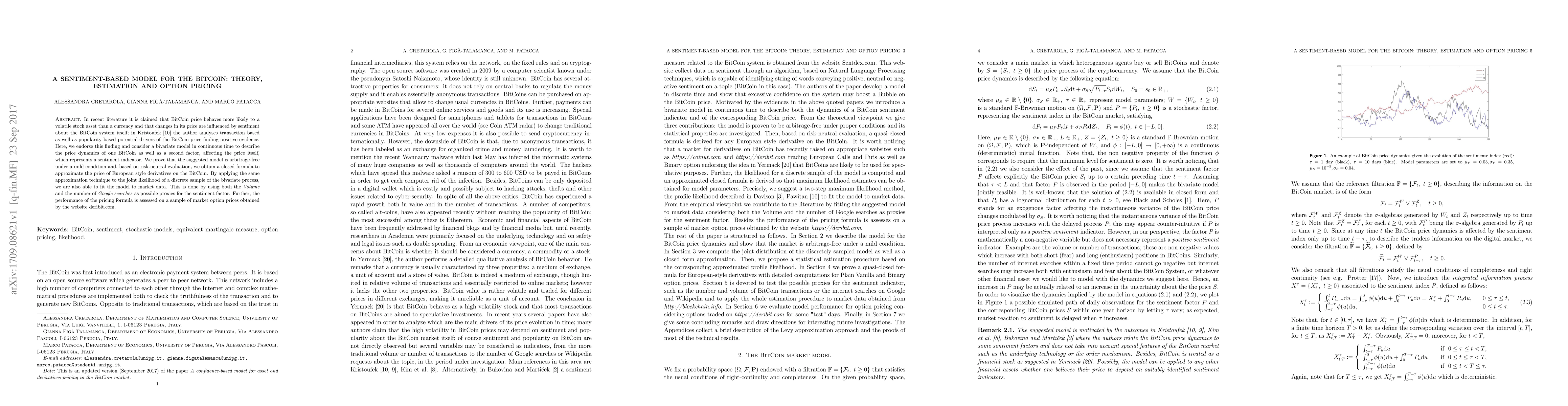

In recent literature it is claimed that BitCoin price behaves more likely to a volatile stock asset than a currency and that changes in its price are influenced by sentiment about the BitCoin system...

Shorting for hedging exposes to risk when the market dynamics is uncertain. Managing uncertainty and risk exposure is key in portfolio management practice. This paper develops a robust framework for d...