Publication

Metrics

AI Quick Summary

This paper proposes a sentiment-based bivariate model for Bitcoin price dynamics, incorporating a sentiment indicator alongside Bitcoin's price. The model is arbitrage-free and provides a closed formula for pricing European style derivatives on Bitcoin, which is validated using market data and option prices.

Paper Preview

Abstract

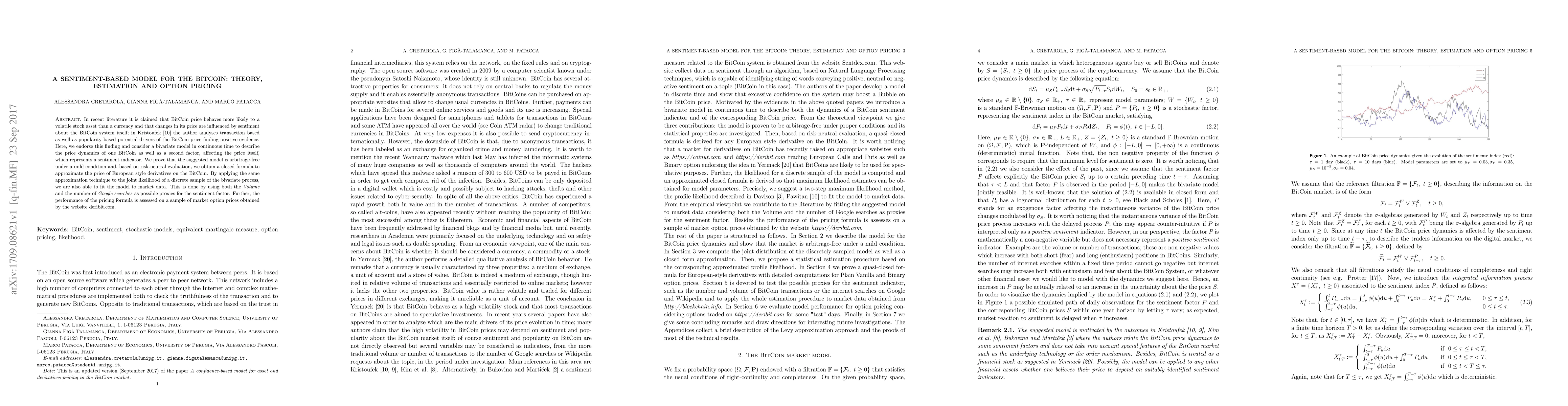

In recent literature it is claimed that BitCoin price behaves more likely to a volatile stock asset than a currency and that changes in its price are influenced by sentiment about the BitCoin system itself; in Kristoufek [10] the author analyses transaction based as well as popularity based potential drivers of the BitCoin price finding positive evidence. Here, we endorse this finding and consider a bivariate model in continuous time to describe the price dynamics of one BitCoin as well as a second factor, affecting the price itself, which represents a sentiment indicator. We prove that the suggested model is arbitrage-free under a mild condition and, based on risk-neutral evaluation, we obtain a closed formula to approximate the price of European style derivatives on the BitCoin. By applying the same approximation technique to the joint likelihood of a discrete sample of the bivariate process, we are also able to fit the model to market data. This is done by using both the Volume and the number of Google searches as possible proxies for the sentiment factor. Further, the performance of the pricing formula is assessed on a sample of market option prices obtained by the website deribit.com.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0