Academic Profile

Statistics

Similar Authors

Papers on arXiv

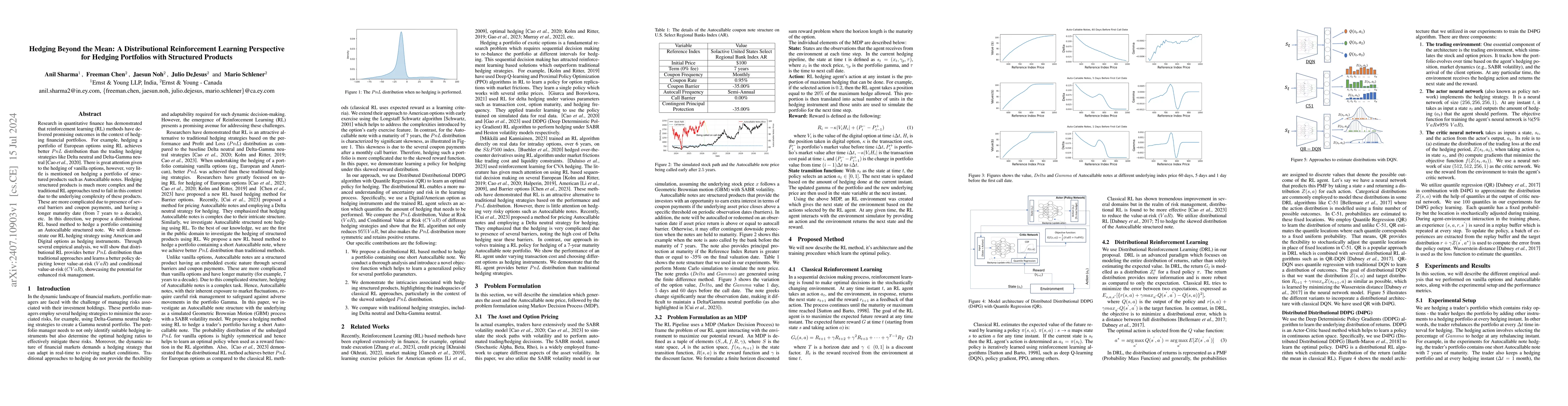

Research in quantitative finance has demonstrated that reinforcement learning (RL) methods have delivered promising outcomes in the context of hedging financial portfolios. For example, hedging a port...

This article leverages deep reinforcement learning (DRL) to hedge American put options, utilizing the deep deterministic policy gradient (DDPG) method. The agents are first trained and tested with G...

In the past few years, Artificial Intelligence (AI) has garnered attention from various industries including financial services (FS). AI has made a positive impact in financial services by enhancing...

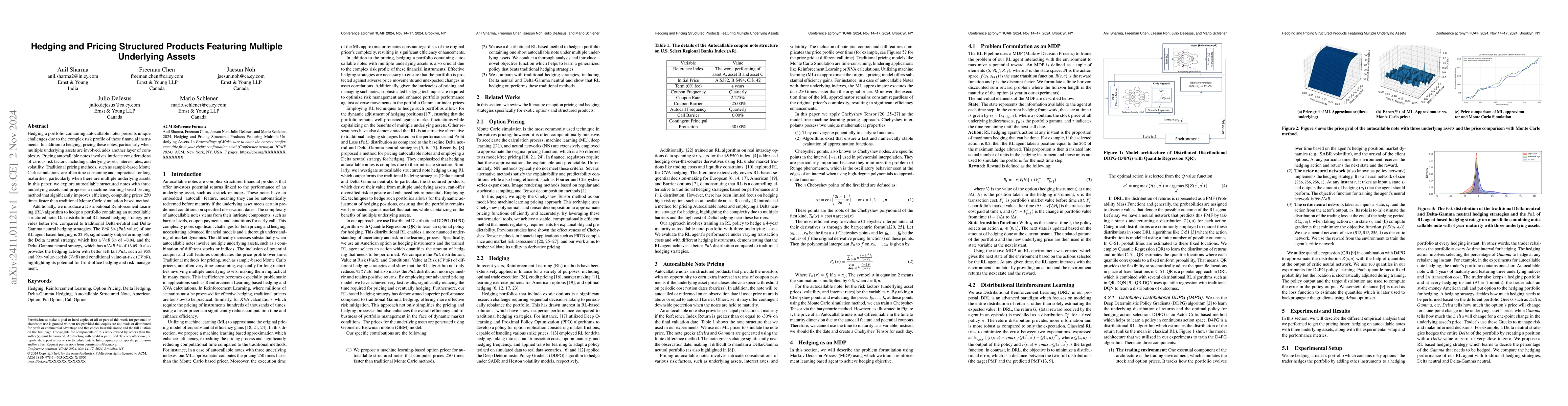

Hedging a portfolio containing autocallable notes presents unique challenges due to the complex risk profile of these financial instruments. In addition to hedging, pricing these notes, particularly w...