Academic Profile

Statistics

Similar Authors

Papers on arXiv

Weak convergence of maxima of dependent sequences of identically distributed continuous random variables is studied under normalizing sequences arising as subsequences of the normalizing sequences f...

The class of index-mixed copulas is introduced and its properties are investigated. Index-mixed copulas are constructed from given base copulas and a random index vector, and show a rather remarkabl...

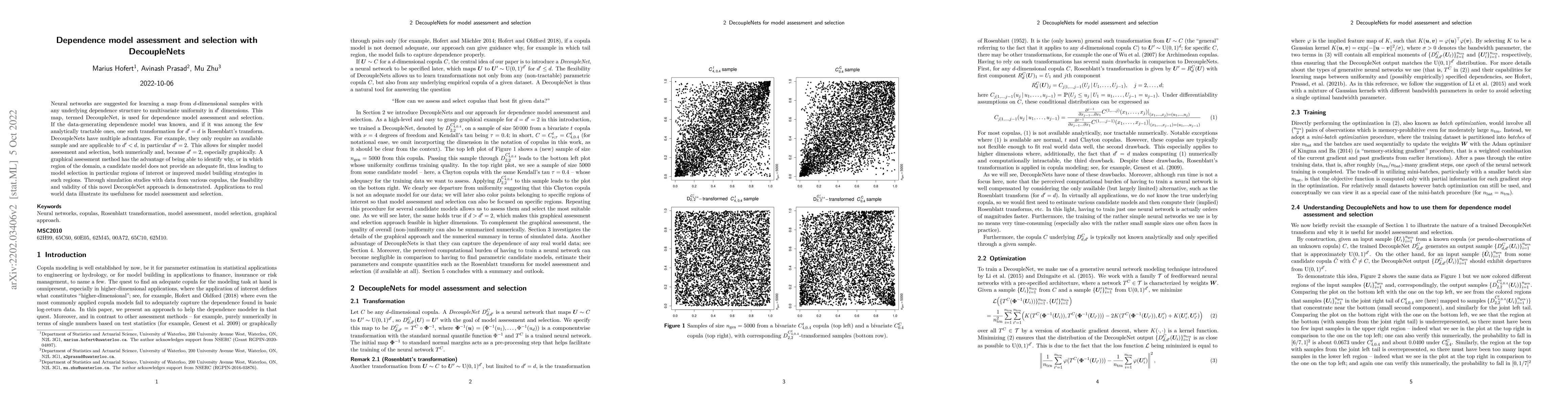

Neural networks are suggested for learning a map from $d$-dimensional samples with any underlying dependence structure to multivariate uniformity in $d'$ dimensions. This map, termed DecoupleNet, is...

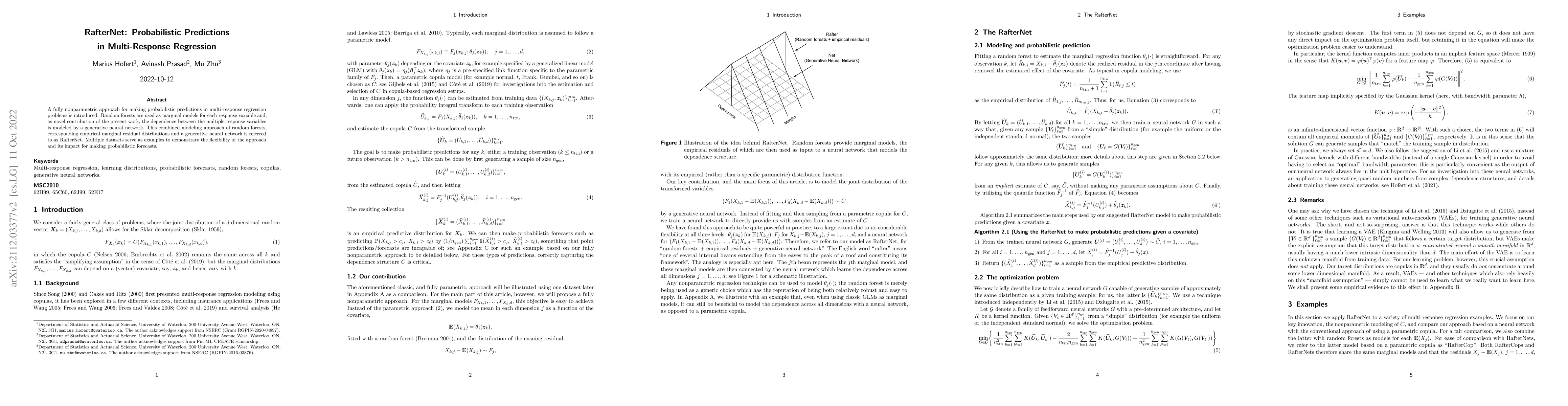

A fully nonparametric approach for making probabilistic predictions in multi-response regression problems is introduced. Random forests are used as marginal models for each response variable and, as...

In many stochastic problems, the output of interest depends on an input random vector mainly through a single random variable (or index) via an appropriate univariate transformation of the input. We...

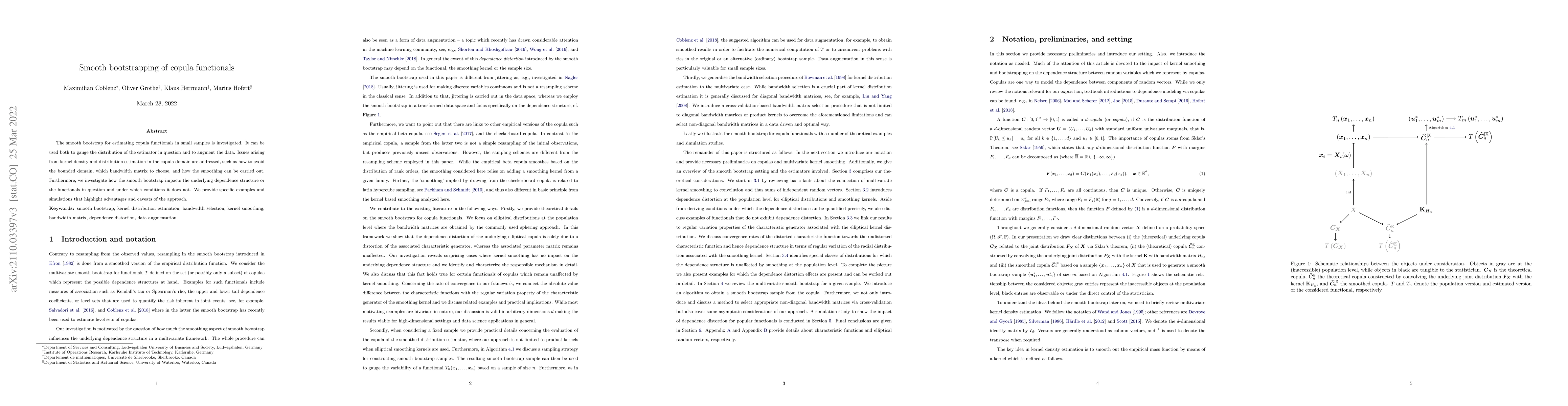

The smooth bootstrap for estimating copula functionals in small samples is investigated. It can be used both to gauge the distribution of the estimator in question and to augment the data. Issues ar...

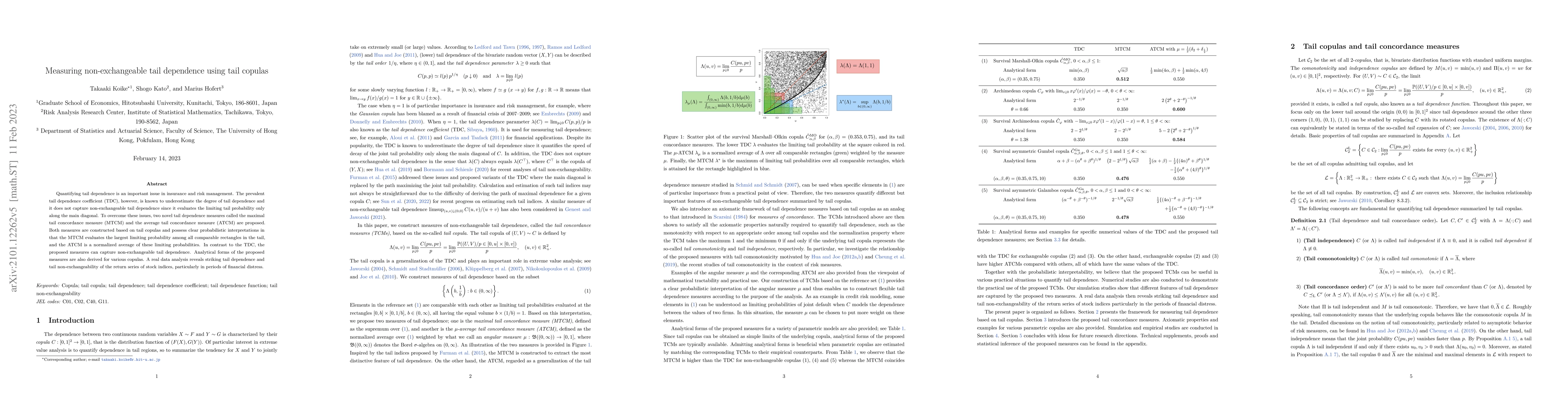

Quantifying tail dependence is an important issue in insurance and risk management. The prevalent tail dependence coefficient (TDC), however, is known to underestimate the degree of tail dependence ...

Generative moment matching networks (GMMNs) are suggested for modeling the cross-sectional dependence between stochastic processes. The stochastic processes considered are geometric Brownian motions...

Representations of measures of concordance in terms of Pearson' s correlation coefficient are studied. All transforms of random variables are characterized such that the correlation coefficient of t...

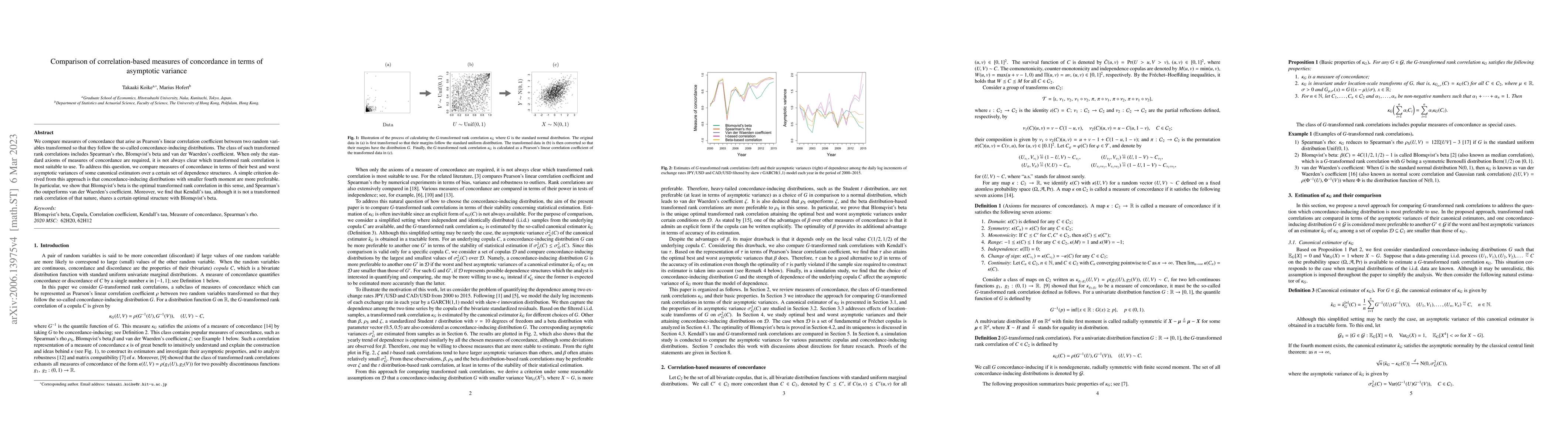

We compare measures of concordance that arise as Pearson's linear correlation coefficient between two random variables transformed so that they follow the so-called concordance-inducing distribution...

The copulas of random vectors with standard uniform univariate margins truncated from the right are considered and a general formula for such right-truncated conditional copulas is derived. This for...

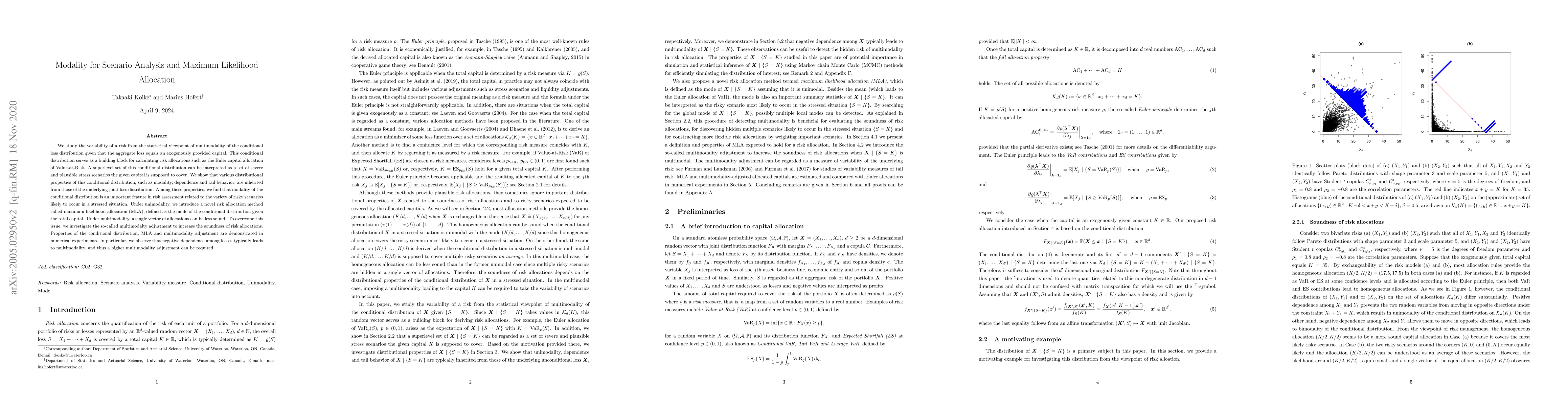

We study the variability of a risk from the statistical viewpoint of multimodality of the conditional loss distribution given that the aggregate loss equals an exogenously provided capital. This con...

It seems surprising that when applying widely used random number generators to generate one million random numbers on modern architectures, one obtains, on average, about 116 collisions. This articl...

Generative moment matching networks (GMMNs) are introduced as dependence models for the joint innovation distribution of multivariate time series (MTS). Following the popular copula-GARCH approach f...

Normal variance mixtures are a class of multivariate distributions that generalize the multivariate normal by randomizing (or mixing) the covariance matrix via multiplication by a non-negative rando...

An approach to amputation, the process of introducing missing values to a complete dataset, is presented. It allows to construct missingness indicators in a flexible and principled way via copulas and...

An adaptive bandwidth selection procedure for the mixture kernel in the maximum mean discrepancy (MMD) for fitting generative moment matching networks (GMMNs) is introduced, and its ability to improve...

W-transforms are introduced as uniformity-preserving univariate transformations on the unit interval induced by distribution functions and piecewise strictly monotone functions, and their properties a...

The classical tail dependence coefficient (TDC) may fail to capture non-exchangeable features of tail dependence due to its restrictive focus on the diagonal of the underlying copula. To address this ...

The classical tail dependence coefficient (TDC) may fail to capture non-exchangeable features of bivariate tail dependence since it evaluates the underlying copula only along the diagonal. To address ...