Academic Profile

Statistics

Similar Authors

Papers on arXiv

The task of analyzing extreme events with censoring effects is considered under a framework allowing for random covariate information. A wide class of estimators that can be cast as product-limit in...

Extremiles provide a generalization of quantiles which are not only robust, but also have an intrinsic link with extreme value theory. This paper introduces an extremile regression model tailored fo...

A novel and comprehensive methodology designed to tackle the challenges posed by extreme values in the context of random censorship is introduced. The main focus is on the analysis of integrals base...

Continuous-time semi-Markov finite state-space jump processes are considered, inspired by a duration-dependent life insurance model. New approximations using grid-conditional homogeneous Markov jump...

We propose an individual claims reserving model based on the conditional Aalen-Johansen estimator, as developed in Bladt and Furrer (2023b). In our approach, we formulate a multi-state problem, wher...

The conditional Aalen--Johansen estimator, a general-purpose non-parametric estimator of conditional state occupation probabilities, is introduced. The estimator is applicable for any finite-state j...

The estimation of absorption time distributions of Markov jump processes is an important task in various branches of statistics and applied probability. While the time-homogeneous case is classic, t...

In this paper we introduce a bivariate distribution on $\mathbb{R}_{+} \times \mathbb{N}$ arising from a single underlying Markov jump process. The marginal distributions are phase-type and discrete...

The setting of a right-censored random sample subject to contamination is considered. In various fields, expert information is often available and used to overcome the contamination. This paper inte...

The statistical censoring setup is extended to the situation when random measures can be assigned to the realization of datapoints, leading to a new way of incorporating expert information into the ...

The study of time-inhomogeneous Markov jump processes is a traditional topic within probability theory that has recently attracted substantial attention in various applications. However, their flexi...

The task of modeling claim severities is addressed when data is not consistent with the classical regression assumptions. This framework is common in several lines of business within insurance and r...

This paper addresses the task of modeling severity losses using segmentation when the data distribution does not fall into the usual regression frameworks. This situation is not uncommon in lines of...

In this paper, we demonstrate through the use of matrix calculus a transparent analysis of fractional inhomogeneous Markov models for life insurance where transition matrices commute. The resulting ...

Phase-type (PH) distributions are a popular tool for the analysis of univariate risks in numerous actuarial applications. Their multivariate counterparts (MPH$^\ast$), however, have not seen such a ...

A phase-type distribution is the distribution of the time until absorption in a finite state-space time-homogeneous Markov jump process, with one absorbing state and the rest being transient. These ...

Stationary and ergodic time series can be constructed using an s-vine decomposition based on sets of bivariate copula functions. The extension of such processes to infinite copula sequences is consi...

We consider estimation of the extreme value index and extreme quantiles for heavy-tailed data that are right-censored. We study a general procedure of removing low importance observations in tail es...

A general framework for the study of regular variation (RV) is that of Polish star-shaped metric spaces, while recent developments in [1] have discussed RV with respect to some properly localised bo...

Products between phase-type distributed random variables and any independent, positive and continuous random variable are studied. Their asymptotic properties are established, and an expectation-max...

The matrixdist R package provides a comprehensive suite of tools for the statistical analysis of matrix distributions, including phase-type, inhomogeneous phase-type, discrete phase-type, and relate...

In this paper we investigate the flexibility of matrix distributions for the modeling of mortality. Starting from a simple Gompertz law, we show how the introduction of matrix-valued parameters via ...

An approach to modelling volatile financial return series using stationary d-vine copula processes combined with Lebesgue-measure-preserving transformations known as v-transforms is proposed. By dev...

We consider the classical Cram\'er-Lundberg risk model with claim sizes that are mixtures of phase-type and subexponential variables. Exploiting a specific geometric compound representation, we prop...

We extend the Kulkarni class of multivariate phase--type distributions in a natural time--fractional way to construct a new class of multivariate distributions with heavy-tailed Mittag-Leffler(ML)-d...

We extend the construction principle of multivariate phase-type distributions to establish an analytically tractable class of heavy-tailed multivariate random variables whose marginal distributions ...

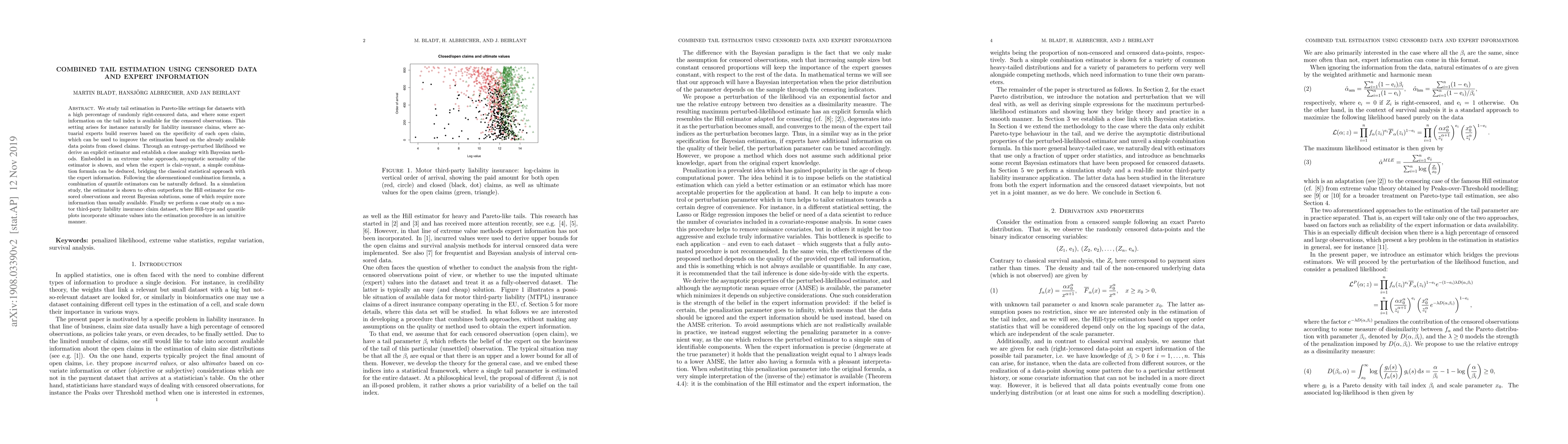

We study tail estimation in Pareto-like settings for datasets with a high percentage of randomly right-censored data, and where some expert information on the tail index is available for the censore...

In this paper we define the class of matrix Mittag-Leffler distributions and study some of its properties. We show that it can be interpreted as a particular case of an inhomogeneous phase-type dist...

We consider removing lower order statistics from the classical Hill estimator in extreme value statistics, and compensating for it by rescaling the remaining terms. Trajectories of these trimmed sta...

It is a well-known fact that an exchangeable sequence has empirical distributions that form a reverse-martingale. This paper is devoted to proof of the converse statement. As a byproduct of the proo...

This paper establishes the functional convergence of the Extreme Nelson--Aalen and Extreme Kaplan--Meier estimators, which are designed to capture the heavy-tailed behaviour of censored losses. The re...

We introduce a novel class of bivariate common-shock discrete phase-type (CDPH) distributions to describe dependencies in loss modeling, with an emphasis on those induced by common shocks. By construc...

A Bayesian non-parametric framework for studying time-to-event data is proposed, where the prior distribution is allowed to depend on an additional random source, and may update with the sample size. ...

In survival analysis, the estimation of the proportion of subjects who will never experience the event of interest, termed the cure rate, has received considerable attention recently. Its estimation c...

We study the consistency and weak convergence of the conditional tail function and conditional Hill estimators under broad dependence assumptions for a heavy-tailed response sequence and a covariate s...

We introduce a class of continuous-time bivariate phase-type distributions for modeling dependencies from common shocks. The construction uses continuous-time Markov processes that evolve identically ...

We study the conditional expert Kaplan-Meier estimator, an extension of the classical Kaplan--Meier estimator designed for time-to-event data subject to both right-censoring and contamination. Such co...

We study various types of consistency of honest decision trees and random forests in the regression setting. In contrast to related literature, our proofs are elementary and follow the classical argum...

Cure rate models address survival data in which a proportion of individuals will never experience the event of interest. Existing parametric approaches are predominantly based on finite mixtures, whic...

This paper proposes a scoring-rule-based method for ranking predictive distributions in the Fréchet domain that is able to distinguish between different tail indices. The approach is built on normaliz...

We investigate the Poisson regression method for Markov and semi-Markov jump processes from a nonparametric angle, allowing the lengths of the time and duration intervals in the partition to vary with...

Insurance payments may depend on latent micro states although only macro states and realized payments are observed. We study a sojourn-payment model for such aggregated multi-state systems under left-...