Combined Tail Estimation Using Censored Data and Expert Information

Publication

Metrics

AI Quick Summary

This paper proposes a novel estimator for tail index estimation in Pareto-like distributions with high right-censored data, integrating expert information. The method, based on an entropy-perturbed likelihood, often outperforms existing estimators in simulations and is applied to a motor liability insurance claim dataset.

Paper Preview

Abstract

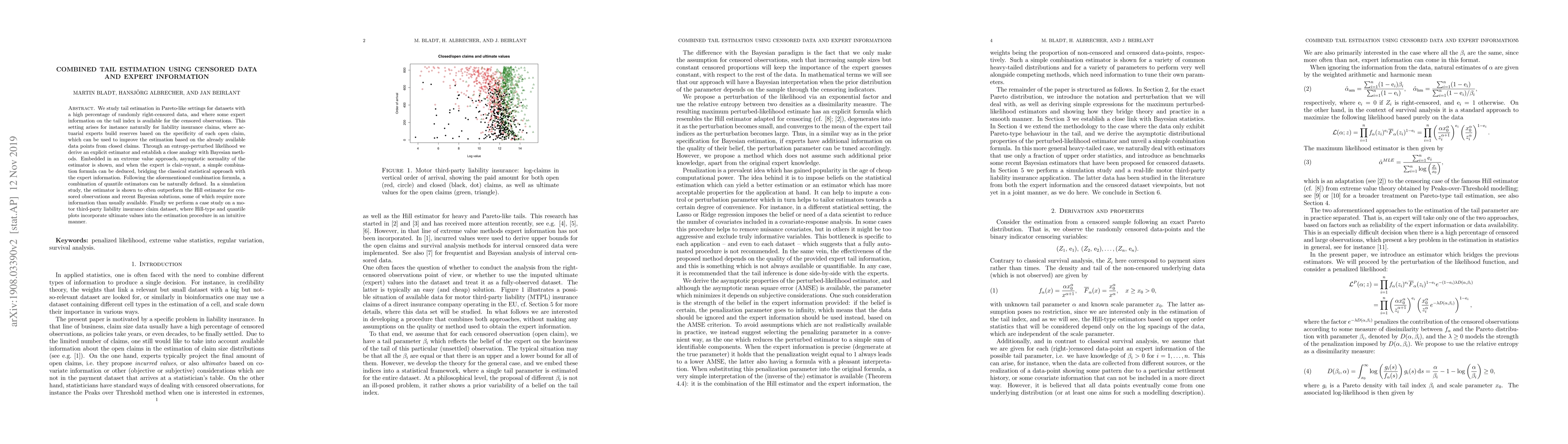

We study tail estimation in Pareto-like settings for datasets with a high percentage of randomly right-censored data, and where some expert information on the tail index is available for the censored observations. This setting arises for instance naturally for liability insurance claims, where actuarial experts build reserves based on the specificity of each open claim, which can be used to improve the estimation based on the already available data points from closed claims. Through an entropy-perturbed likelihood we derive an explicit estimator and establish a close analogy with Bayesian methods. Embedded in an extreme value approach, asymptotic normality of the estimator is shown, and when the expert is clair-voyant, a simple combination formula can be deduced, bridging the classical statistical approach with the expert information. Following the aforementioned combination formula, a combination of quantile estimators can be naturally defined. In a simulation study, the estimator is shown to often outperform the Hill estimator for censored observations and recent Bayesian solutions, some of which require more information than usually available. Finally we perform a case study on a motor third-party liability insurance claim dataset, where Hill-type and quantile plots incorporate ultimate values into the estimation procedure in an intuitive manner.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0