Academic Profile

Statistics

Similar Authors

Papers on arXiv

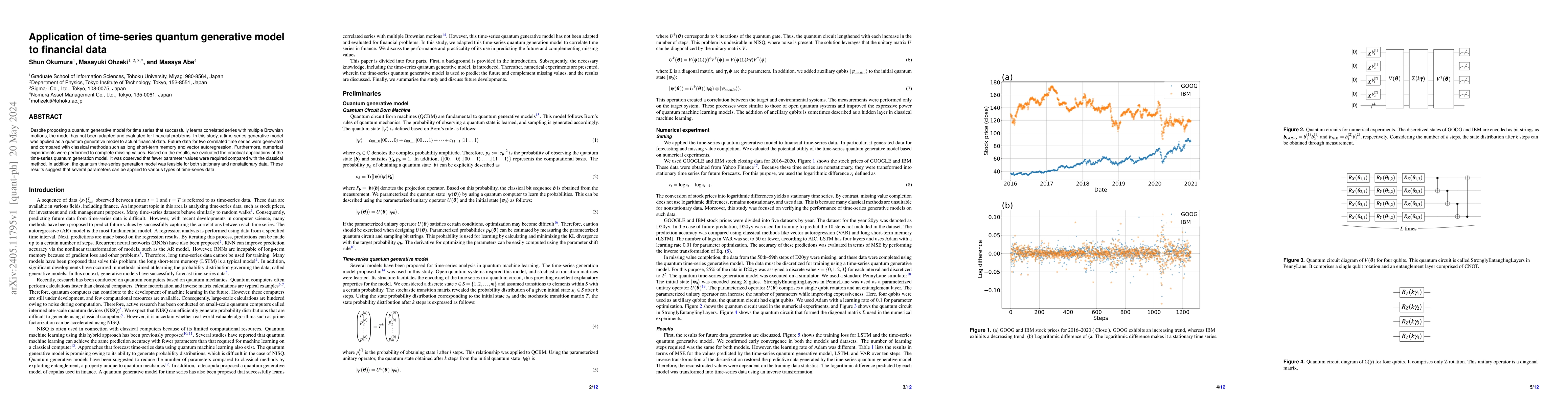

Despite proposing a quantum generative model for time series that successfully learns correlated series with multiple Brownian motions, the model has not been adapted and evaluated for financial pro...

In this study, we address the challenge of portfolio optimization, a critical aspect of managing investment risks and maximizing returns. The mean-CVaR portfolio is considered a promising method due...

Quantum computers are gaining attention for their ability to solve certain problems faster than classical computers, and one example is the quantum expectation estimation algorithm that accelerates ...

We consider controlling the false discovery rate for testing many time series with an unknown cross-sectional correlation structure. Given a large number of hypotheses, false and missing discoveries...

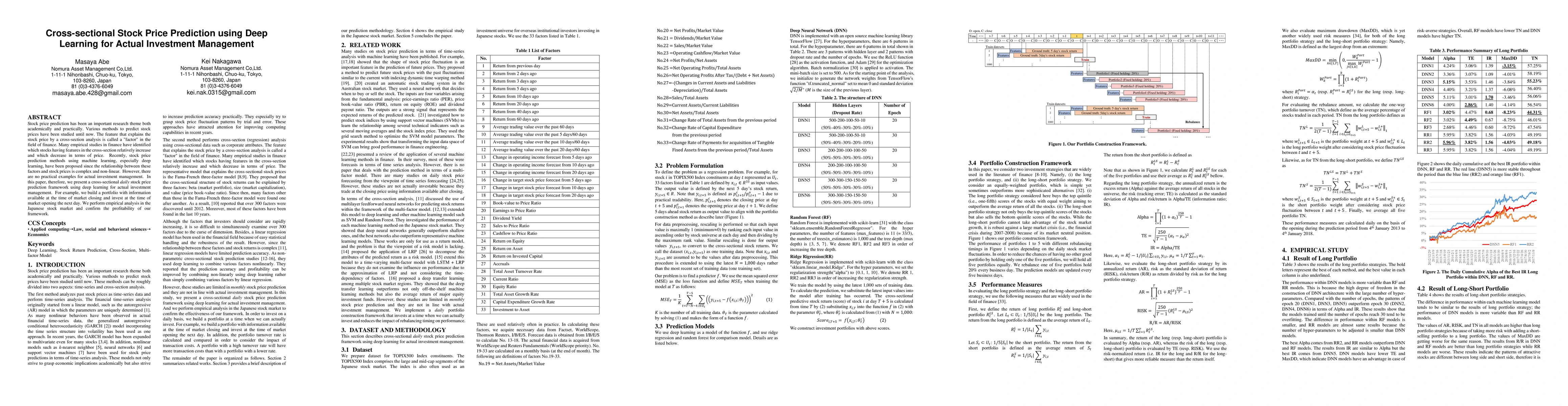

Stock price prediction has been an important research theme both academically and practically. Various methods to predict stock prices have been studied until now. The feature that explains the stoc...

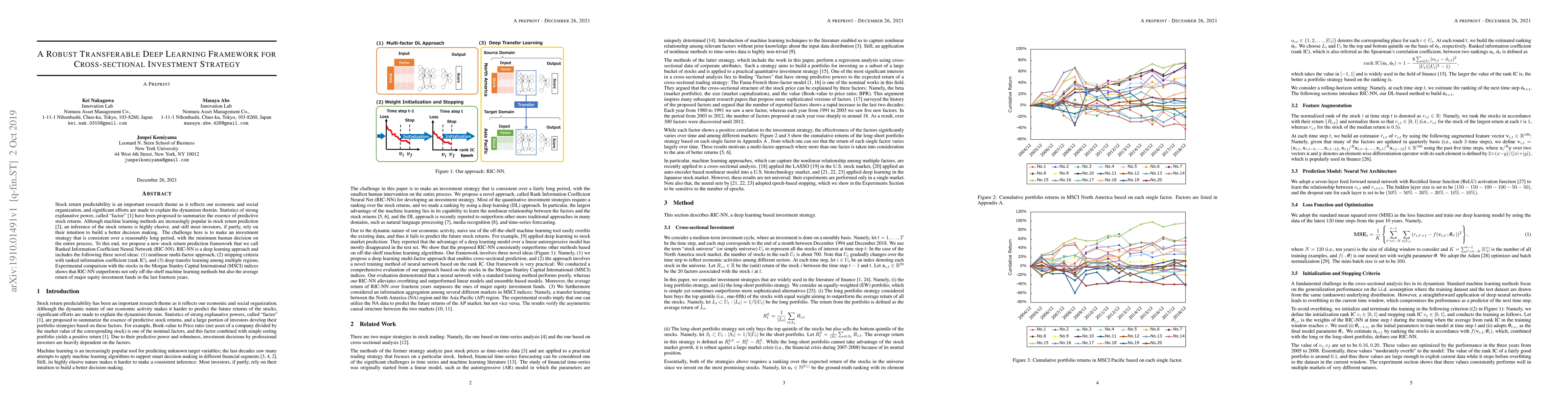

Stock return predictability is an important research theme as it reflects our economic and social organization, and significant efforts are made to explain the dynamism therein. Statistics of strong...