Academic Profile

Statistics

Similar Authors

Papers on arXiv

We study a robust utility maximization problem in a general discrete-time frictionless market. The investor is assumed to have a random, nonconcave and nondecreasing utility function, which may or m...

We study a robust utility maximization problem in a general discrete-time frictionless market under quasi-sure no-arbitrage. The investor is assumed to have a random and concave utility function def...

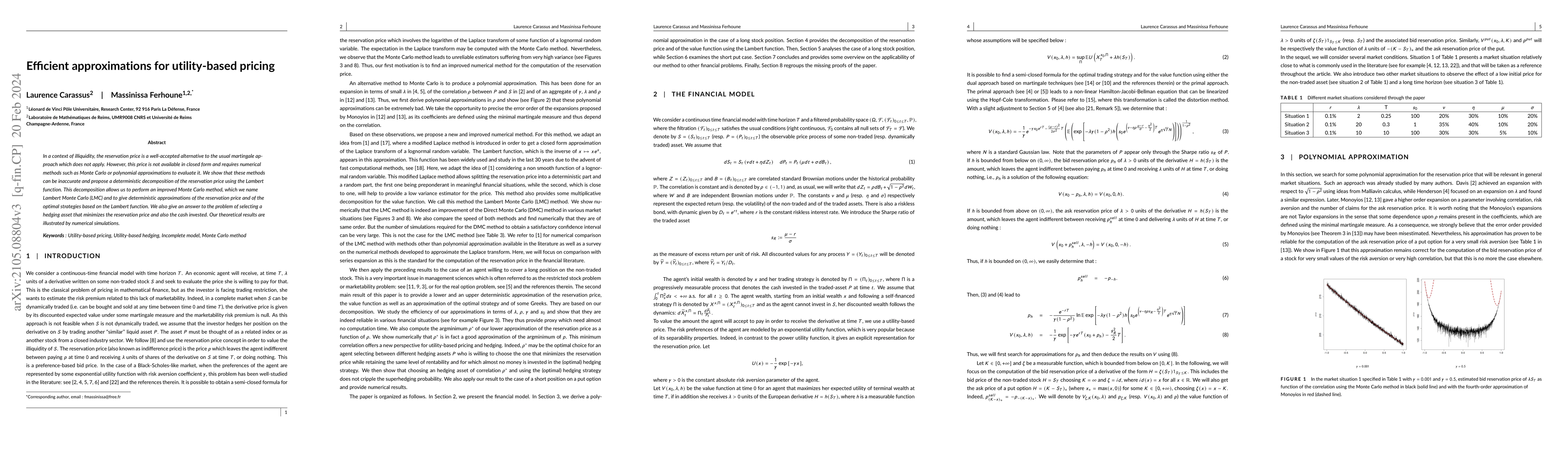

In a context of illiquidity, the reservation price is a well-accepted alternative to the usual martingale approach which does not apply. However, this price is not available in closed form and requi...

We study projective functions. We prove that projective functions generalise lower and upper-semianalytic ones while being stable by composition and difference. We show that the class of projective fu...