Academic Profile

Statistics

Similar Authors

Papers on arXiv

The dual attainment of the Monge--Kantorovich transport problem is analyzed in a general setting. The spaces $X, Y$ are assumed to be polish and equipped with Borel probability measures $\mu$ and $\...

Causal optimal transport and adapted Wasserstein distance have applications in different fields from optimization to mathematical finance and machine learning. The goal of this article is to provide...

Change of numeraire is a classical tool in mathematical finance. Campi-Laachir-Martini established its applicability to martingale optimal transport. We note that the results of Campi-Laachir-Martin...

Random variables $X^i$, $i=1,2$ are 'probabilistically equivalent' if they have the same law. Moreover, in any class of equivalent random variables it is easy to select canonical representatives. ...

A basic and natural coupling between two probabilities on $\mathbb R^N$ is given by the Knothe-Rosenblatt coupling. It represents a multiperiod extension of the quantile coupling and is simple to ca...

In classical optimal transport, the contributions of Benamou$-$Brenier and McCann regarding the time-dependent version of the problem are cornerstones of the field and form the basis for a variety o...

The increasing availability of granular and big data on various objects of interest has made it necessary to develop methods for condensing this information into a representative and intelligible ma...

Adapted or causal transport theory aims to extend classical optimal transport from probability measures to stochastic processes. On a technical level, the novelty is to restrict to couplings which a...

Hamza-Klebaner posed the problem of constructing martingales with Brownian marginals that differ from Brownian motion, so called fake Brownian motions. Besides its theoretical appeal, the problem re...

In light of the continuing emergence of new SARS-CoV-2 variants and vaccines, we create a simulation framework for exploring possible infection trajectories under various scenarios. The situations o...

While many questions in (robust) finance can be posed in the martingale optimal transport (MOT) framework, others require to consider also non-linear cost functionals. Following the terminology of G...

Famously mathematical finance was started by Bachelier in his 1900 PhD thesis where - among many other achievements - he also provides a formal derivation of the Kolmogorov forward equation. This fo...

Wasserstein distance induces a natural Riemannian structure for the probabilities on the Euclidean space. This insight of classical transport theory is fundamental for tremendous applications in var...

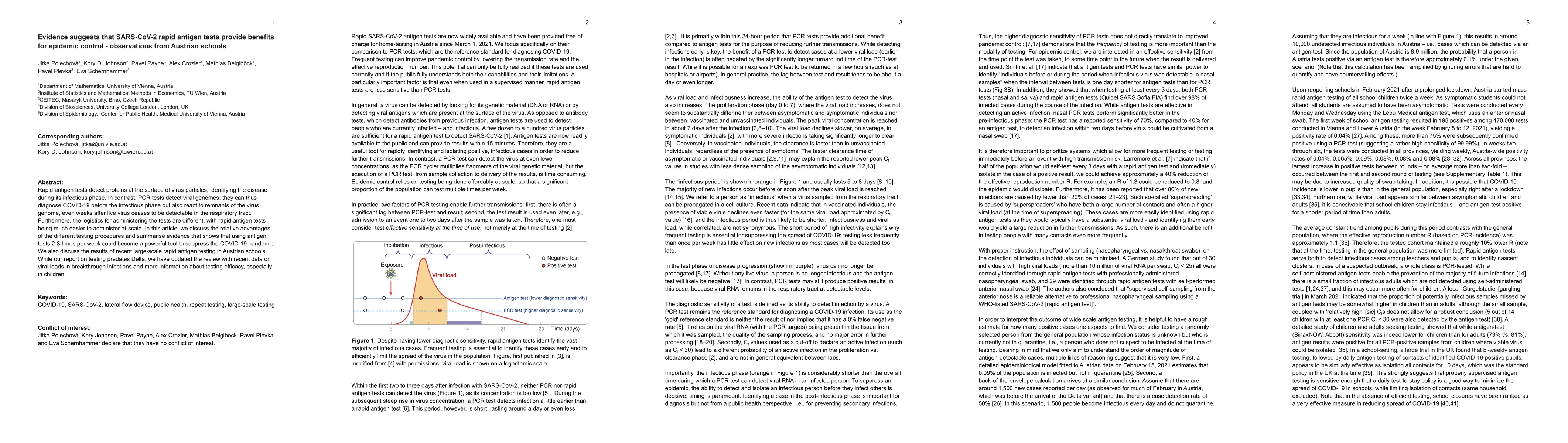

Rapid antigen tests detect proteins at the surface of virus particles, identifying the disease during its infectious phase. In contrast, PCR tests detect viral genomes; they can thus diagnose COVID-...

Our main result is to establish stability of martingale couplings: suppose that $\pi$ is a martingale coupling with marginals $\mu, \nu$. Then, given approximating marginal measures $\tilde \mu \app...

It is well known that given two probability measures $\mu$ and $\nu$ on $\mathbb{R}$ in convex order there exists a discrete-time martingale with these marginals. Several solutions are known (for ex...

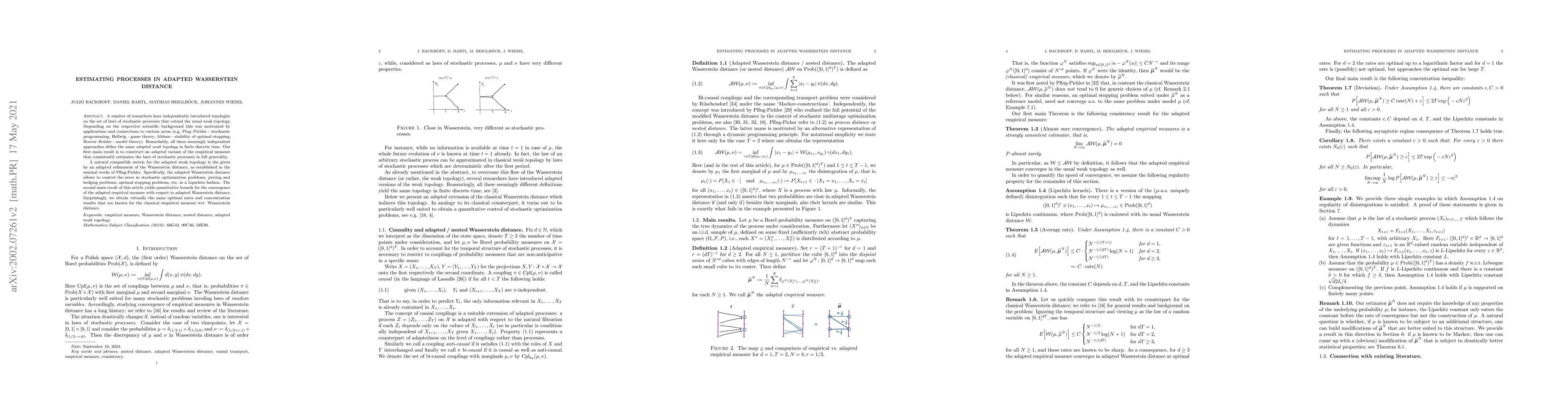

A number of researchers have independently introduced topologies on the set of laws of stochastic processes that extend the usual weak topology. Depending on the respective scientific background thi...

A number of researchers have introduced topological structures on the set of laws of stochastic processes. A unifying goal of these authors is to strengthen the usual weak topology in order to adequ...

We study the problem of stopping a Brownian motion at a given distribution $\nu$ while optimizing a reward function that depends on the (possibly randomized) stopping time and the Brownian motion. O...

Assume that an agent models a financial asset through a measure Q with the goal to price / hedge some derivative or optimize some expected utility. Even if the model Q is chosen in the most skilful ...

It is well known that any pair of random variables $(X,Y)$ with values in Polish spaces, provided that $Y$ is nonatomic, can be approximated in joint law by random variables of the form $(X',Y)$ whe...

Researchers from different areas have independently defined extensions of the usual weak convergence of laws of stochastic processes with the goal of adequately accounting for the flow of information....

The fundamental theorem of classical optimal transport establishes strong duality and characterizes optimizers through a complementary slackness condition. Milestones such as Brenier's theorem and the...

Pinsker's classical inequality asserts that the total variation $TV(\mu, \nu)$ between two probability measures is bounded by $\sqrt{ 2H(\mu|\nu)}$ where $H$ denotes the relative entropy (or Kullback-...

Brenier's fundamental theorem characterizes optimal transport plans for measures $\mu, \nu$ on $\mathbb{R}^d$ and quadratic distance costs in terms of gradients of convex functions. In particular it g...

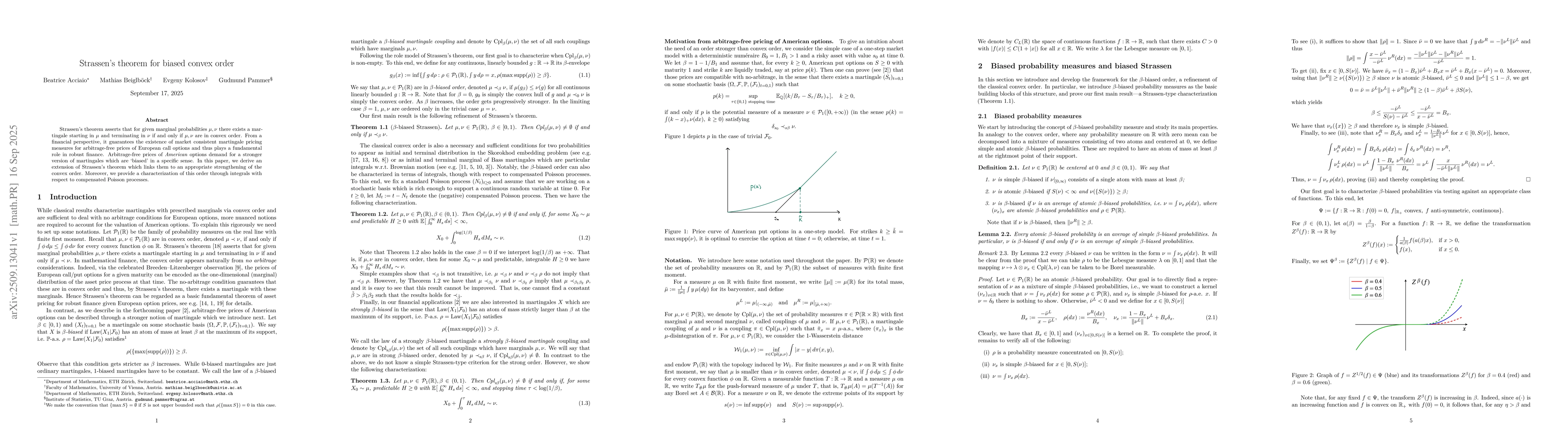

Strassen's theorem asserts that for given marginal probabilities $\mu,\nu$ there exists a martingale starting in $\mu$ and terminating in $\nu$ if and only if $\mu,\nu$ are in convex order. From a fin...

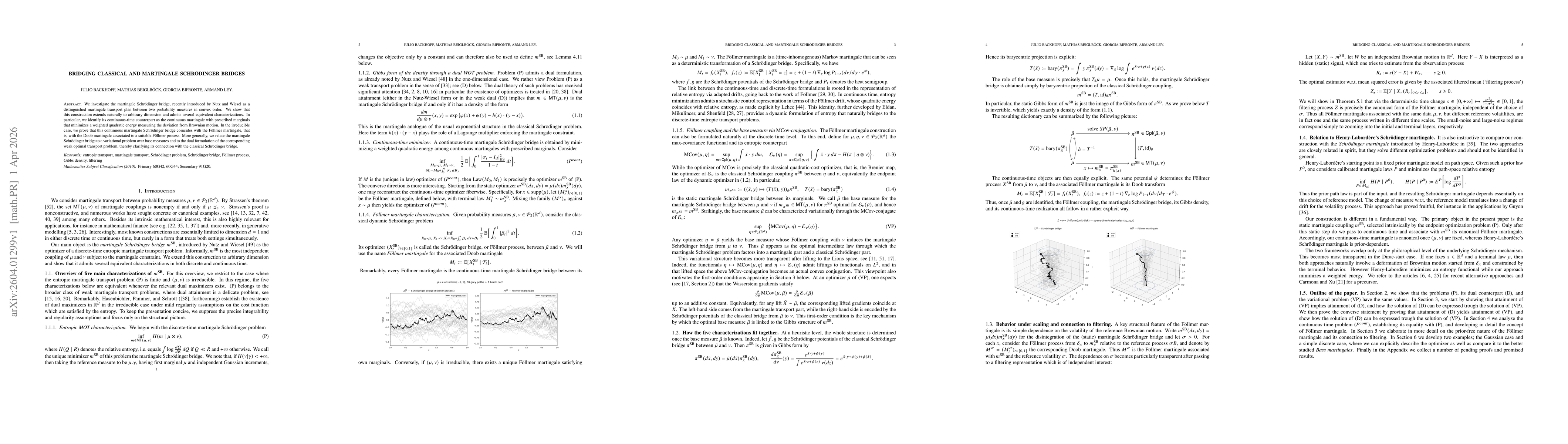

We investigate the martingale Schrödinger bridge, recently introduced by Nutz and Wiesel as a distinguished martingale transport plan between two probability measures in convex order. We show that thi...