Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper considers estimation of large dynamic factor models with common and idiosyncratic trends by means of the Expectation Maximization algorithm, implemented jointly with the Kalman smoother. ...

This paper studies Quasi Maximum Likelihood estimation of Dynamic Factor Models for large panels of time series. Specifically, we consider the case in which the autocorrelation of the factors is exp...

We introduce methodology to bridge scenario analysis and model-based risk forecasting, leveraging their respective strengths in policy settings. Our Bayesian framework addresses the fundamental challe...

We measure the Euro Area (EA) output gap and potential output using a non-stationary dynamic factor model estimated on a large dataset of macroeconomic and financial variables. From 2012 to 2024, we e...

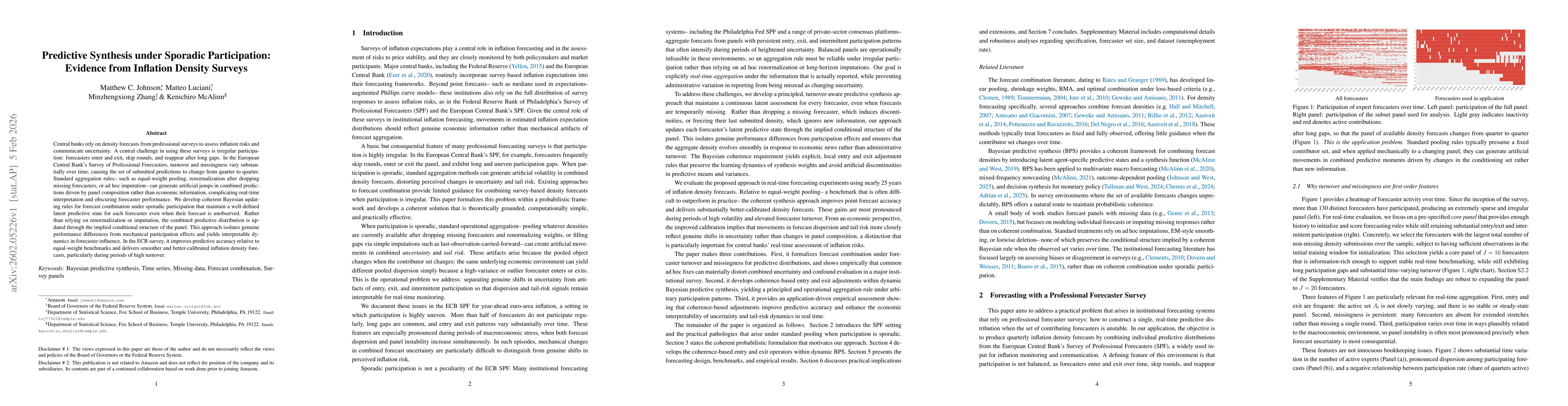

Central banks rely on density forecasts from professional surveys to assess inflation risks and communicate uncertainty. A central challenge in using these surveys is irregular participation: forecast...

We discuss probabilistic measures of concordance between two probability distributions based on the expected misclassification rate (EMR). The focus is on comparing a given reference distribution with...

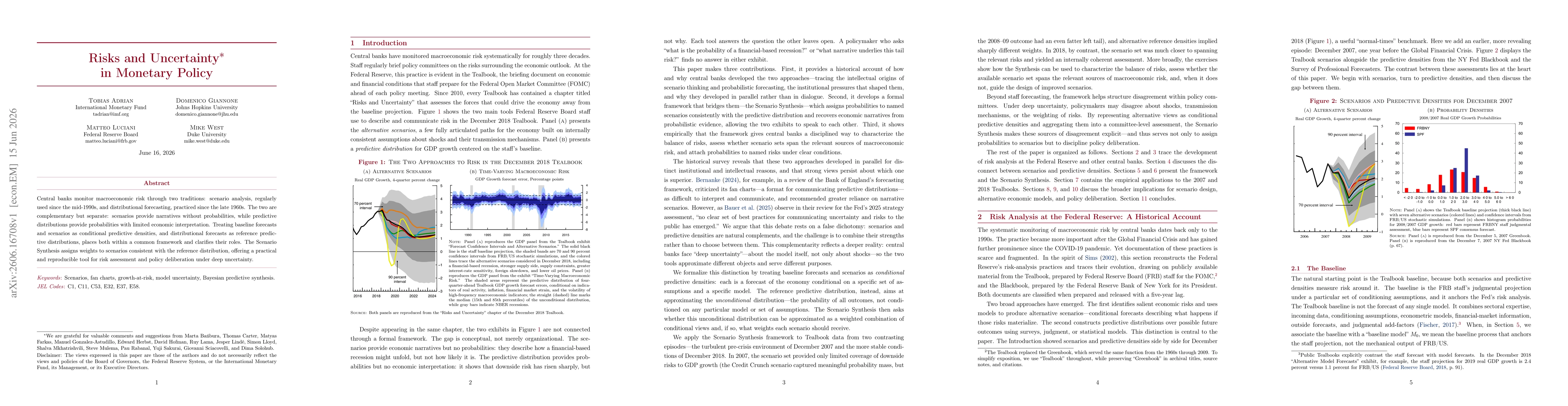

Central banks monitor macroeconomic risk through two traditions: scenario analysis, regularly used since the mid-1990s, and distributional forecasting, practiced since the late 1960s. The two are comp...