Academic Profile

Statistics

Similar Authors

Papers on arXiv

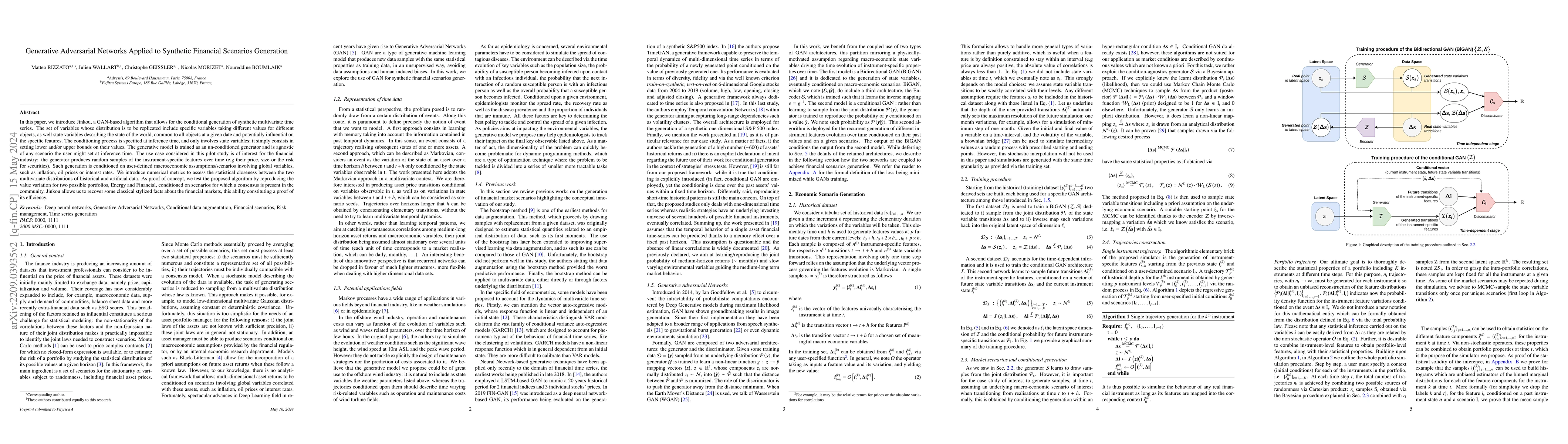

The finance industry is producing an increasing amount of datasets that investment professionals can consider to be influential on the price of financial assets. These datasets were initially mainly...

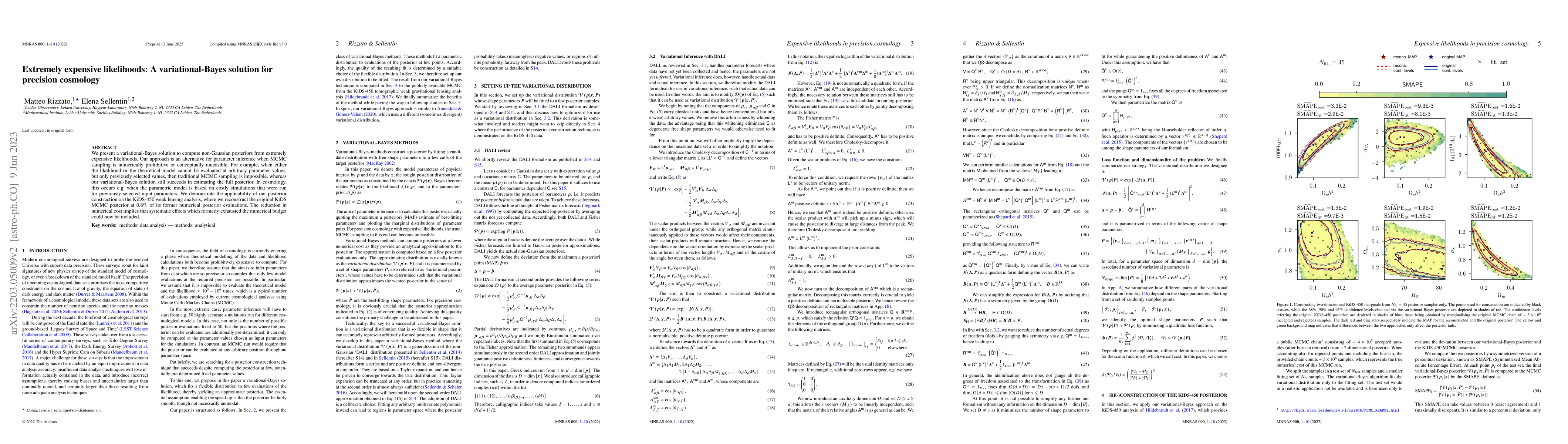

We present a variational-Bayes solution to compute non-Gaussian posteriors from extremely expensive likelihoods. Our approach is an alternative for parameter inference when MCMC sampling is numerica...

Non-Gaussian (NG) statistics of the thermal Sunyaev-Zeldovich (tSZ) effect carry significant information which is not contained in the power spectrum. Here, we perform a joint Fisher analysis of the...