Academic Profile

Statistics

Similar Authors

Papers on arXiv

The TrendLSW R package has been developed to provide users with a suite of wavelet-based techniques to analyse the statistical properties of nonstationary time series. The key components of the pack...

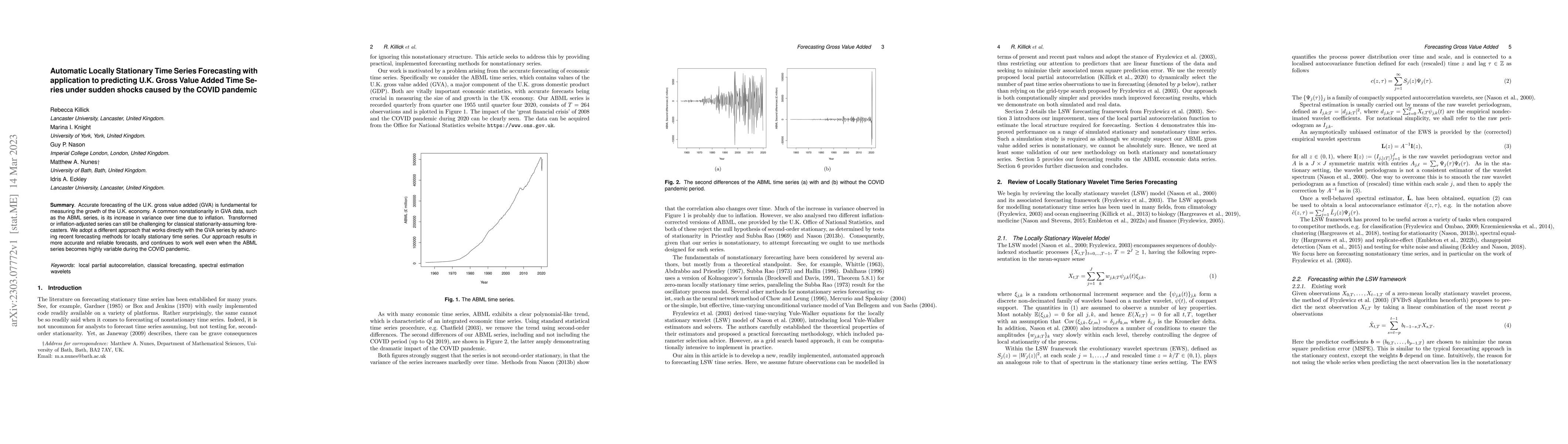

Accurate forecasting of the U.K. gross value added (GVA) is fundamental for measuring the growth of the U.K. economy. A common nonstationarity in GVA data, such as the ABML series, is its increase i...

Most time series observed in practice exhibit time-varying trend (first-order) and autocovariance (second-order) behaviour. Differencing is a commonly-used technique to remove the trend in such seri...

Many scientific areas, from computer science to the environmental sciences and finance, give rise to multivariate time series which exhibit long memory, or loosely put, a slow decay in their autocorre...

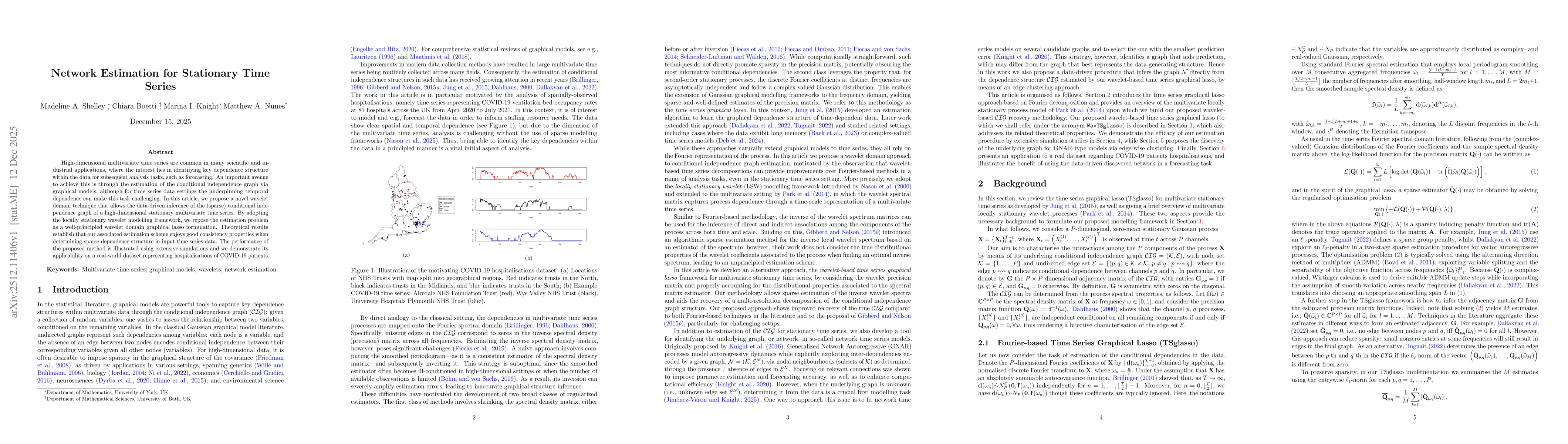

High-dimensional multivariate time series are common in many scientific and industrial applications, where the interest lies in identifying key dependence structure within the data for subsequent anal...

Realized volatility has become a standard tool for measuring latent variation in financial assets, and its forecasting is crucial for a wide range of financial applications. We propose a network-based...

In numerous scientific and industrial settings, observed multivariate time series are often nonstationary in nature, i.e., comprise data whose second order properties vary over time. An additional fea...