Academic Profile

Statistics

Similar Authors

Papers on arXiv

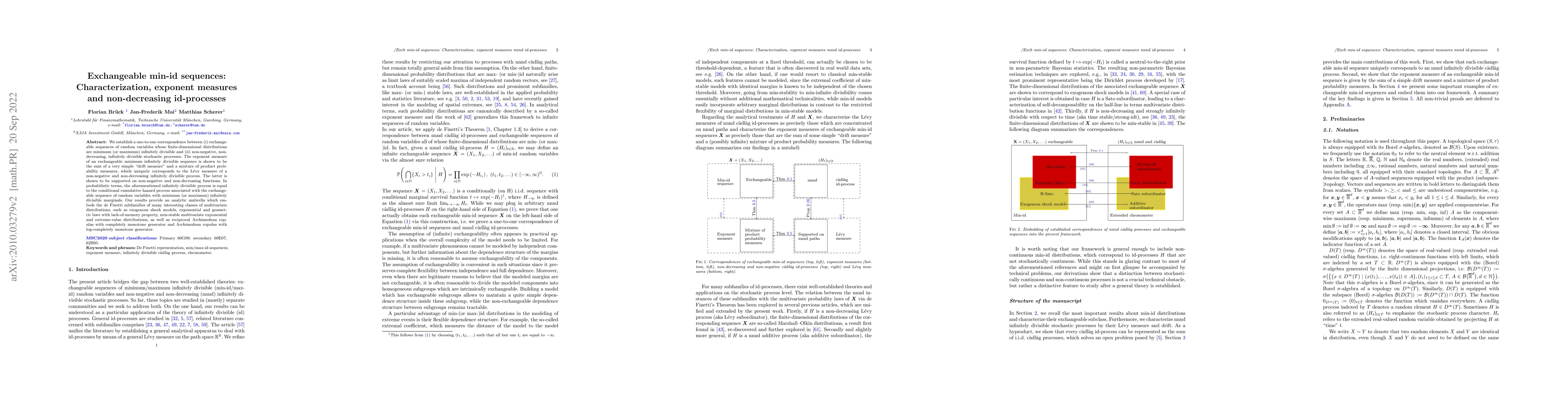

We establish a one-to-one correspondence between (i) exchangeable sequences of random variables whose finite-dimensional distributions are minimum (or maximum) infinitely divisible and (ii) non-nega...

Two stochastic representations of multivariate geometric distributions are analyzed, both are obtained by lifting the lack-of-memory (LM) property of the univariate geometric law to the multivariate...

We show that the set of $d$-variate symmetric stable tail dependence functions, uniquely associated with exchangeable $d$-dimensional extreme-value copulas, is a simplex and determine its extremal b...

The concept of a L\'evy subordinator is generalized to a family of non-decreasing stochastic processes, which are parameterized in terms of two Bernstein functions. Whereas the independent increment...

Payments in parametric insurance solutions are linked to an index and thus decoupled from policyholders' true losses. While this principle has appealing operational benefits compared to traditional in...

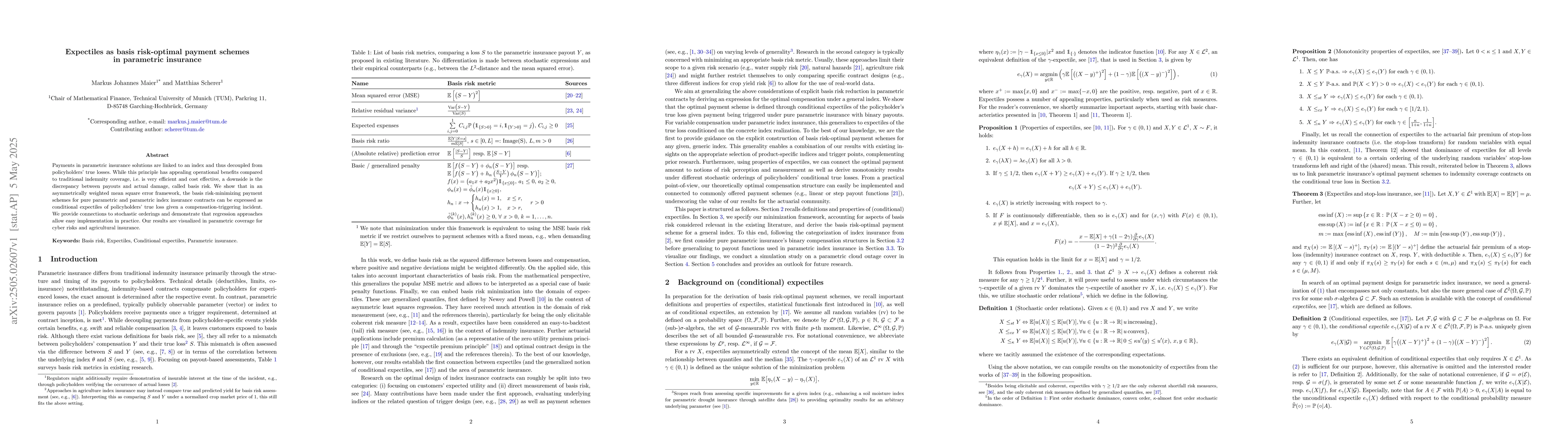

Parametric insurance contracts translate index measurements to compensation for policyholders' losses using predefined payment schemes. These need to be designed carefully to keep basis risk, i.e. the...