Academic Profile

Statistics

Similar Authors

Papers on arXiv

Risk management is particularly concerned with extreme events, but analysing these events is often hindered by the scarcity of data, especially in a multivariate context. This data scarcity complica...

This paper proposes a regression tree procedure to estimate conditional copulas. The associated algorithm determines classes of observations based on covariate values and fits a simple parametric co...

In extreme value theory and other related risk analysis fields, probability weighted moments (PWM) have been frequently used to estimate the parameters of classical extreme value distributions. This...

Parametric insurance has emerged as a practical way to cover risks that may be difficult to assess. By introducing a parameter that triggers compensation and allows the insurer to determine a paymen...

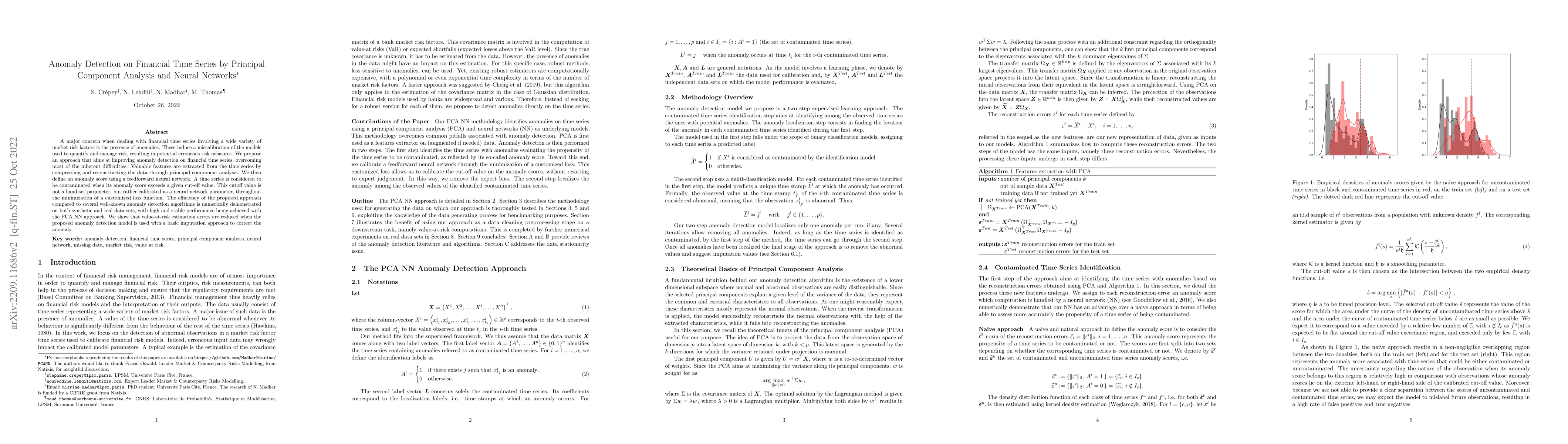

A major concern when dealing with financial time series involving a wide variety ofmarket risk factors is the presence of anomalies. These induce a miscalibration of the models used toquantify and m...

In this paper, we provide finite sample results to assess the consistency of Generalized Pareto regression trees, as tools to perform extreme value regression. The results that we provide are obtain...

Inference in extreme value theory relies on a limited number of extreme observations, making estimation challenging. To address this limitation, we propose a non-parametric bootstrap procedure, the mu...