Academic Profile

Statistics

Similar Authors

Papers on arXiv

We consider a singular control problem where the reward function depends on the state of the process. The main objective of this paper is to establish sufficient conditions for determining the optim...

This work presents a new Distributionally Robust Optimization approach, using $p$-Wasserstein metrics, to analyze a stochastic program in a general context. The ambiguity set in this approach depend...

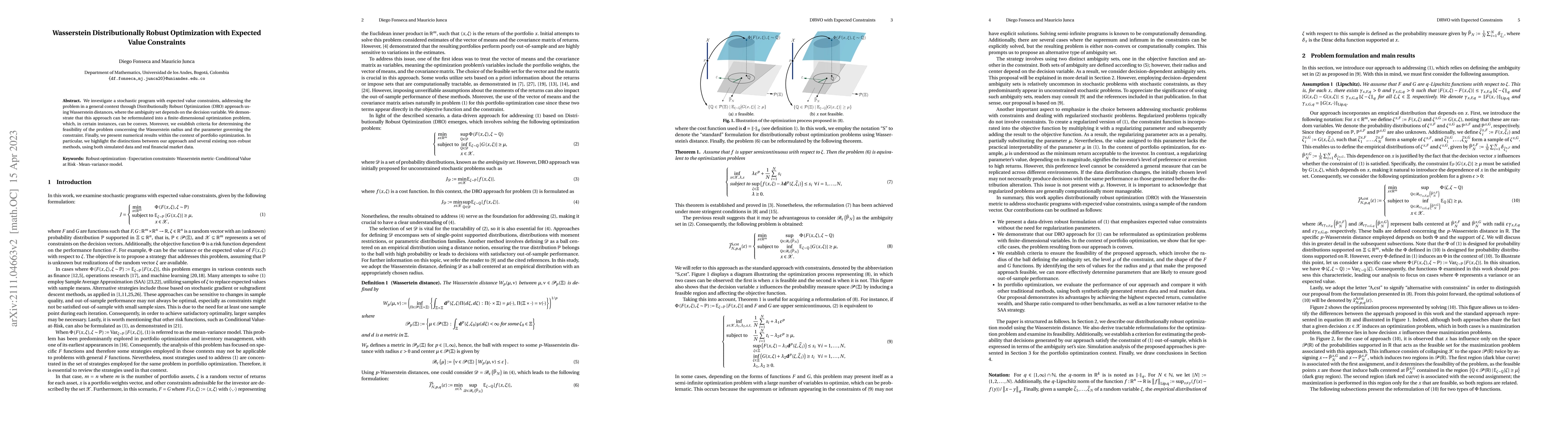

We investigate a stochastic program with expected value constraints, addressing the problem in a general context through Distributionally Robust Optimization (DRO) approach using Wasserstein distanc...

The moment sum of squares (moment-SOS) hierarchy produces sequences of upper and lower bounds on functionals of the exit time solution of a polynomial stochastic differential equation with polynomia...

We consider a Markov control model in discrete time with countable both state space and action space. Using the value function of a suitable long-run average reward problem, we study various reachab...

We consider de Finetti's problem for spectrally one-sided L\'evy risk models with control strategies that are absolutely continuous with respect to the Lebesgue measure. Furthermore, we consider the...

The relationship between inverse reinforcement learning (IRL) and inverse optimization (IO) for Markov decision processes (MDPs) has been relatively underexplored in the literature, despite addressing...

We propose a flexible scenario-based regularized Sample Average Approximation (SBR-SAA) framework for stochastic optimization. This work is motivated by challenges in standard Wasserstein Distribution...