Academic Profile

Statistics

Similar Authors

Papers on arXiv

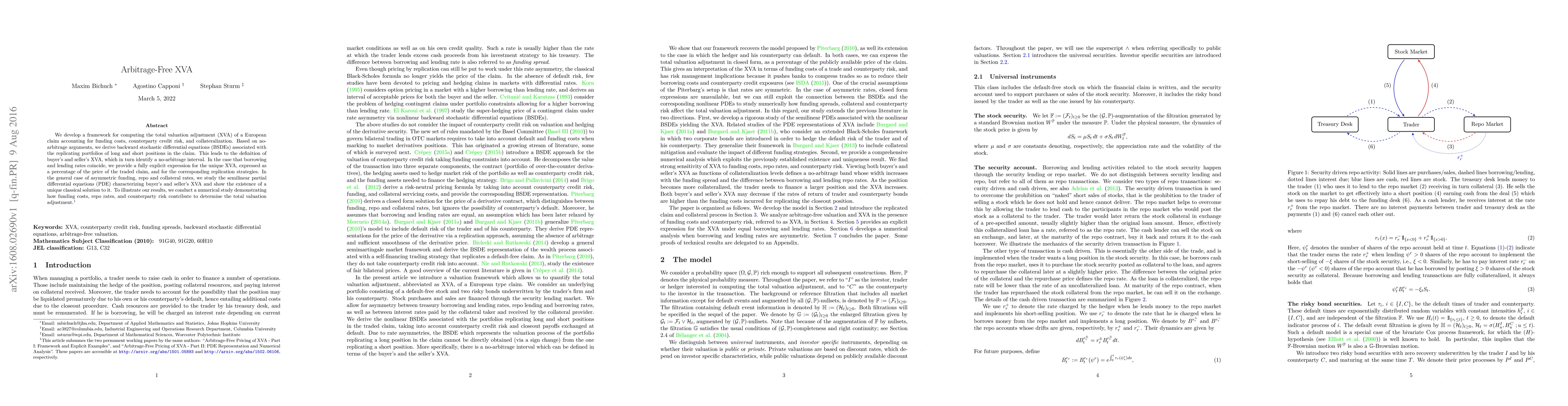

We develop a framework for computing the total valuation adjustment (XVA) of a European claim accounting for funding costs, counterparty credit risk, and collateralization. Based on no-arbitrage arg...

Prediction markets allow traders to bet on potential future outcomes. These markets exist for weather, political, sports, and economic forecasting. Within this work we consider a decentralized frame...

Within this work we consider an axiomatic framework for Automated Market Makers (AMMs). By imposing reasonable axioms on the underlying utility function, we are able to characterize the properties o...

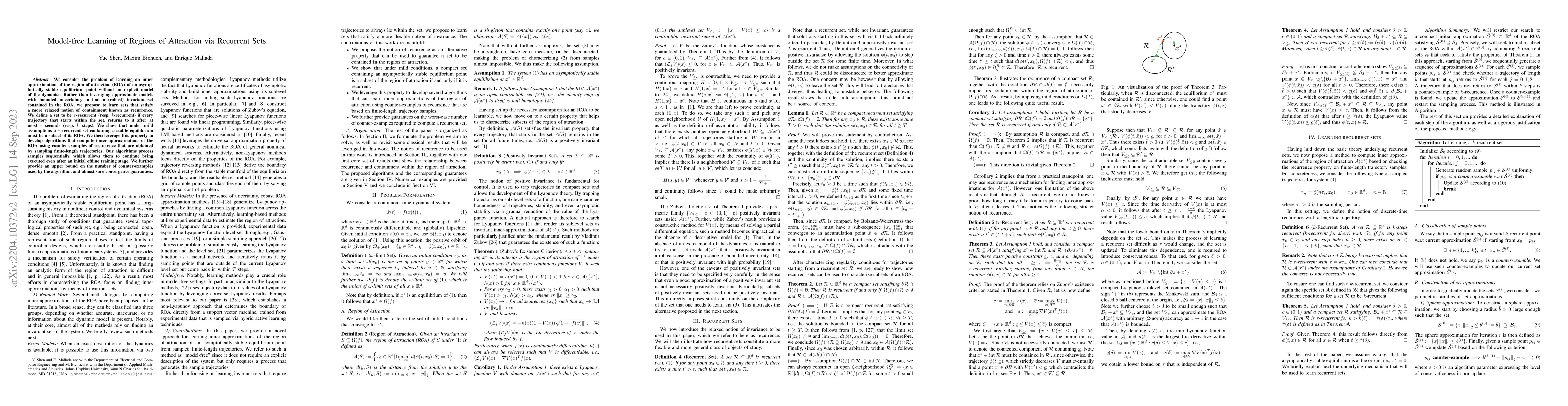

We consider the problem of learning an inner approximation of the region of attraction (ROA) of an asymptotically stable equilibrium point without an explicit model of the dynamics. Rather than leve...

We consider a network of bank holdings, where every holding has two subsidiaries of different types. A subsidiary can trade with another holding's subsidiary of the same type. Holdings support their...

Learning is a process which can update decision rules, based on past experience, such that future performance improves. Traditionally, machine learning is often evaluated under the assumption that t...

In this paper, we construct a decentralized clearing mechanism which endogenously and automatically provides a claims resolution procedure. This mechanism can be used to clear a network of obligatio...

In this work we present an equilibrium formulation for price impacts. This is motivated by the Buhlmann equilibrium in which assets are sold into a system of market participants, e.g. a fire sale in...

This work seeks to quantify the benefits of using energy storage toward the reduction of the energy generation cost of a power system. A two-fold optimization framework is provided where the first o...

We consider a network of banks that optimally choose a strategy of asset liquidations and borrowing in order to cover short term obligations. The borrowing is done in the form of collateralized repu...

The problem of portfolio allocation in the context of stocks evolving in random environments, that is with volatility and returns depending on random factors, has attracted a lot of attention. The p...

We introduce an arbitrage-free framework for robust valuation adjustments. An investor trades a credit default swap portfolio with a risky counterparty, and hedges credit risk by taking a position i...

Empirically, the prevailing market prices for liquidity tokens of the constant product market maker (CPMM) -- as offered in practice by companies such as Uniswap -- readily permit arbitrage opportunit...

An automated market maker (AMM) provides a method for creating a decentralized exchange on the blockchain. For this purpose, individual investors lend liquidity to the AMM pool in exchange for a strea...

Financial options are fundamental to traditional markets, enabling strategies ranging from hedging to speculating. Yet, while the Automated Market Maker paradigm has revolutionized decentralized spot ...