Academic Profile

Statistics

Similar Authors

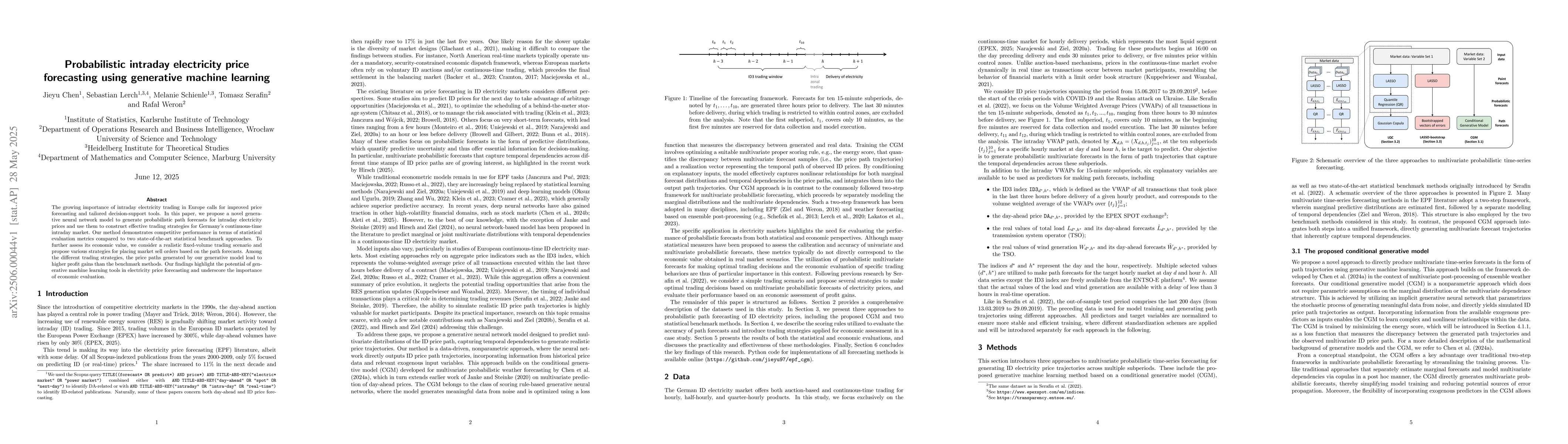

Papers on arXiv

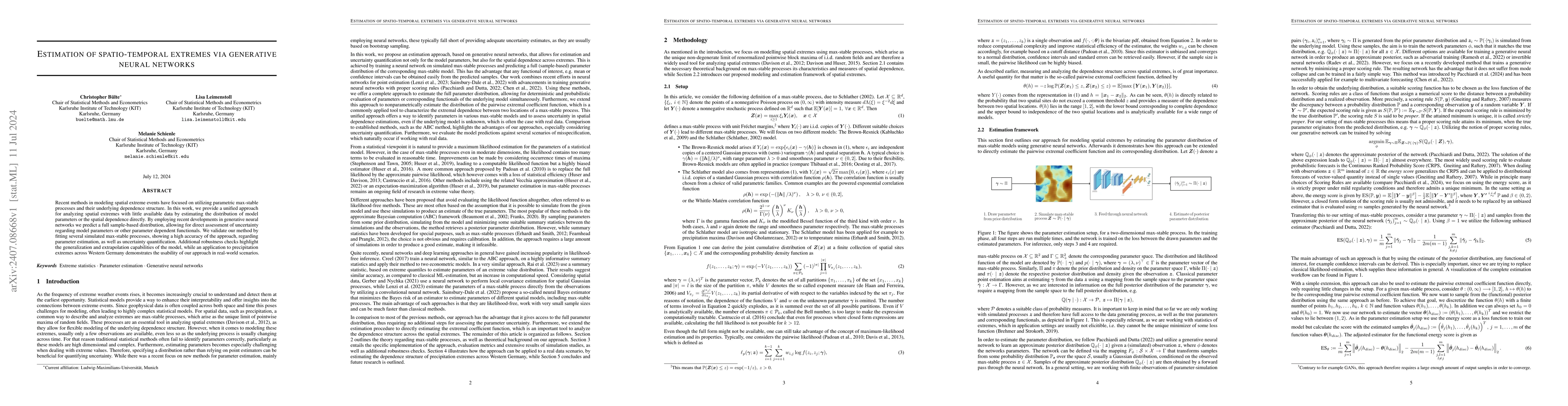

Recent methods in modeling spatial extreme events have focused on utilizing parametric max-stable processes and their underlying dependence structure. In this work, we provide a unified approach for a...

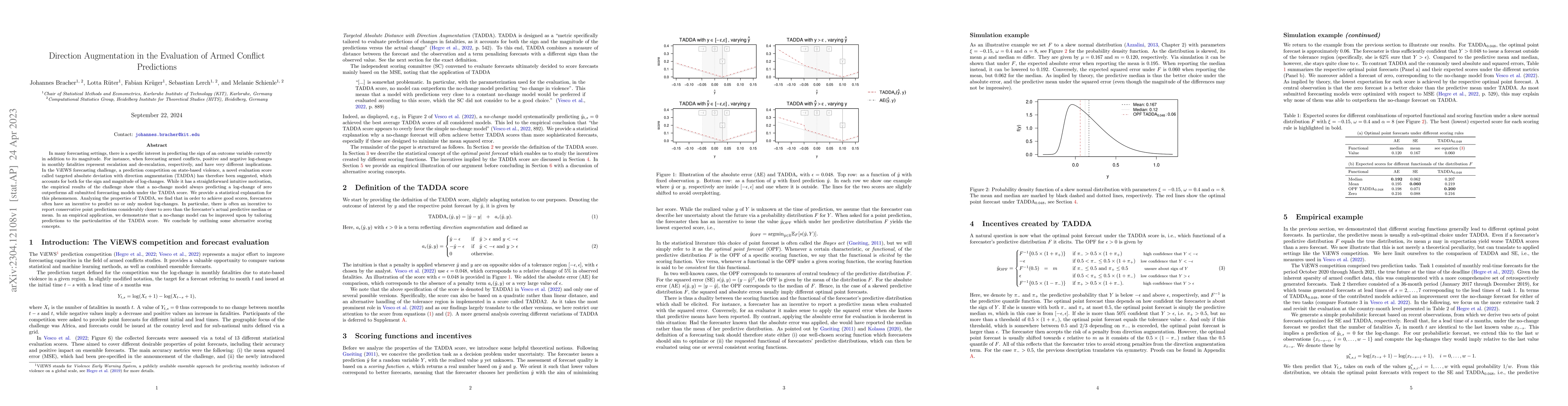

In many forecasting settings, there is a specific interest in predicting the sign of an outcome variable correctly in addition to its magnitude. For instance, when forecasting armed conflicts, posit...

We address challenges in variable selection with highly correlated data that are frequently present in finance, economics, but also in complex natural systems as e.g. weather. We develop a robustifi...

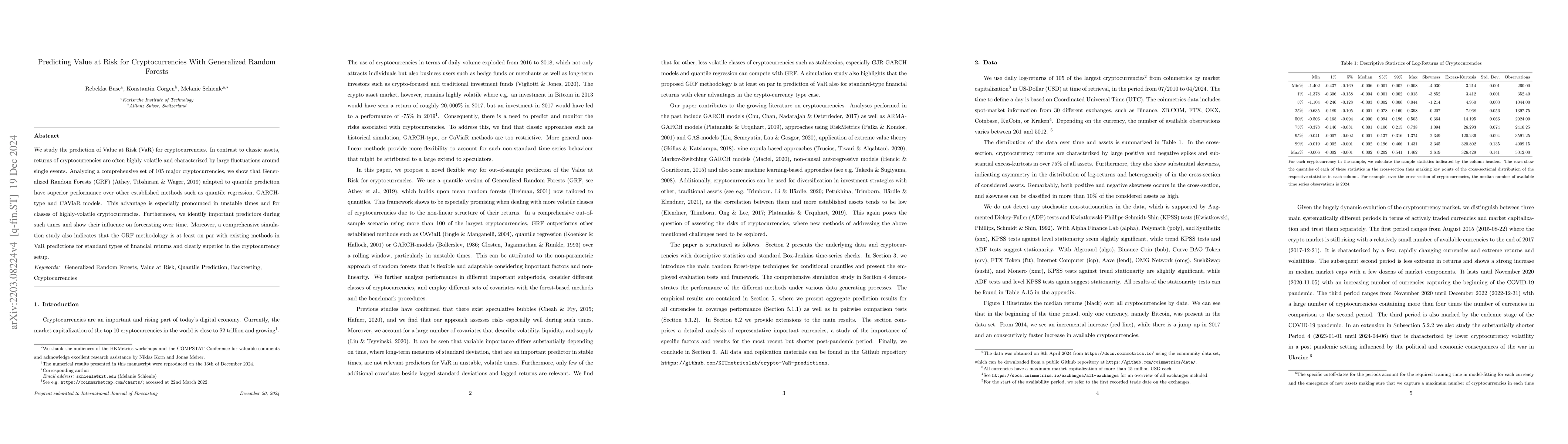

We study the prediction of Value at Risk (VaR) for cryptocurrencies. In contrast to classic assets, returns of cryptocurrencies are often highly volatile and characterized by large fluctuations arou...

We propose an adaption of the multiple imputation random lasso procedure tailored to longitudinal data with unobserved fixed effects which provides robust variable selection in the presence of complex...

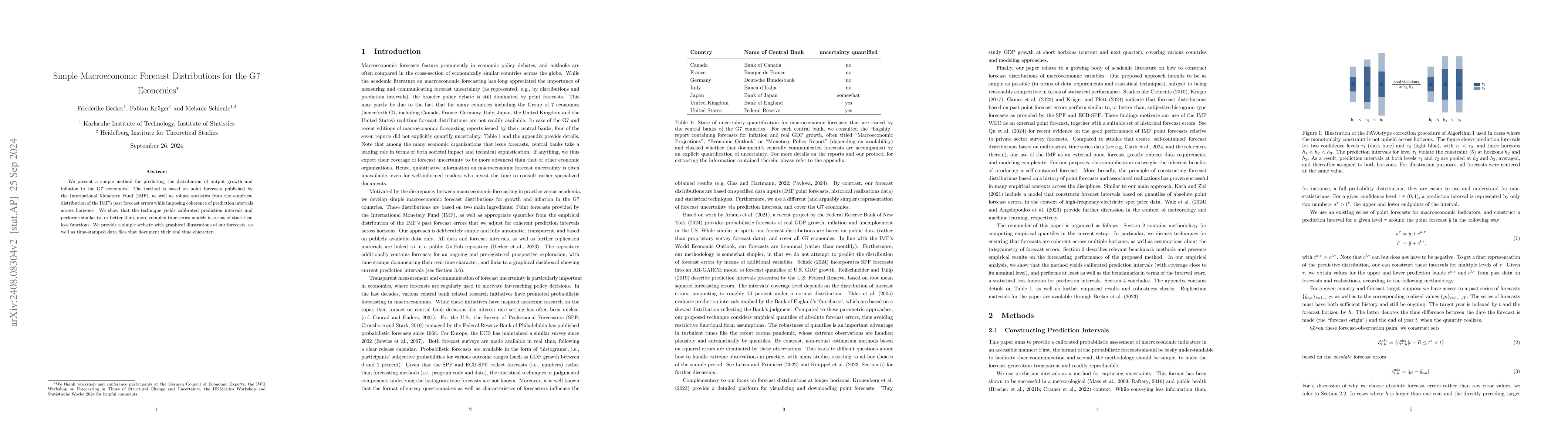

We present a simple method for predicting the distribution of output growth and inflation in the G7 economies. The method is based on point forecasts published by the International Monetary Fund (IMF)...

The growing importance of intraday electricity trading in Europe calls for improved price forecasting and tailored decision-support tools. In this paper, we propose a novel generative neural network m...

Energy forecasting research faces a persistent comparability gap that makes it difficult to measure consistent progress over time. Reported accuracy gains are often not directly comparable because mod...