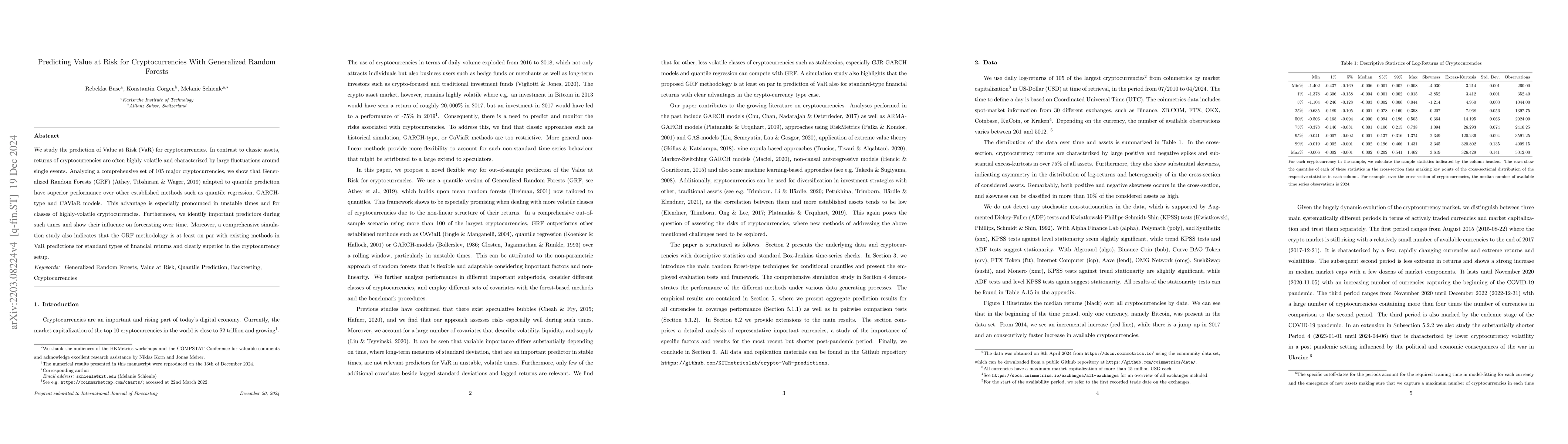

We study the prediction of Value at Risk (VaR) for cryptocurrencies. In

contrast to classic assets, returns of cryptocurrencies are often highly

volatile and characterized by large fluctuations around single events.

Analyzing a comprehensive set of 105 major cryptocurrencies, we show that

Generalized Random Forests (GRF) (Athey et al., 2019) adapted to quantile

prediction have superior performance over other established methods such as

quantile regression, GARCH-type and CAViaR models. This advantage is especially

pronounced in unstable times and for classes of highly-volatile

cryptocurrencies. Furthermore, we identify important predictors during such

times and show their influence on forecasting over time. Moreover, a

comprehensive simulation study also indicates that the GRF methodology is at

least on par with existing methods in VaR predictions for standard types of

financial returns and clearly superior in the cryptocurrency setup.

Discussion 0