Academic Profile

Statistics

Similar Authors

Papers on arXiv

We show that a necessary and sufficient condition for the sum of iid random vectors to converge (under appropriate shifting and scaling) to a multivariate Gaussian distribution is that the truncated...

This paper serves a twofold purpose. First, a unified perspective on diversity indices is introduced based on an entropic basis. It is shown that the class of all linear combinations of the entropic...

We introduce a large and flexible class of discrete tempered stable distributions, and analyze the domains of attraction for both this class and the related class of positive tempered stable distrib...

We develop a Dickman approximation to the small jumps of multivariate L\'evy processes and related stochastic integral processes. Further, we show that the multivariate Dickman distribution is the u...

A multivariate extension of the Dickman distribution was recently introduced, but very few properties have been studied. We discuss several properties with an emphasis on simulation. Further, we int...

We develop efficient methods for simulating processes of Ornstein-Uhlenbeck type related to the class of $p$-tempered $\alpha$-stable ($\ts$) distributions. Our results hold for both the univariate ...

We prove an analog of the classical Zero-One Law for both homogeneous and nonhomogeneous Markov chains (MC). Its almost precise formulation is simple: given any event $A$ from the tail $\sigma$-alge...

Rapidly decreasing tempered stable distributions are useful models for financial applications. However, there has been no exact method for simulation available in the literature. We remedy this by i...

We derive an explicit representation for the transition law of a $p$-tempered $\alpha$-stable process of Ornstein-Uhlenbeck-type and use it to develop a methodology for simulation. Our results apply...

This article studies the expected occupancy probabilities on an alphabet. Unlike the standard situation, where observations are assumed to be independent and identically distributed (iid), we assume...

We extend the idea of tempering stable Levy processes to tempering more general classes of Levy processes. We show that the original process can be decomposed into the sum of the tempered process an...

Subordinators are infinitely divisible distributions on the positive half-line. They are often used as mixing distributions in Poisson mixtures. We show that appropriately scaled Poisson mixtures can ...

Turing's estimator allows one to estimate the probabilities of outcomes that either do not appear or only rarely appear in a given random sample. We perform a simulation study to understand the finite...

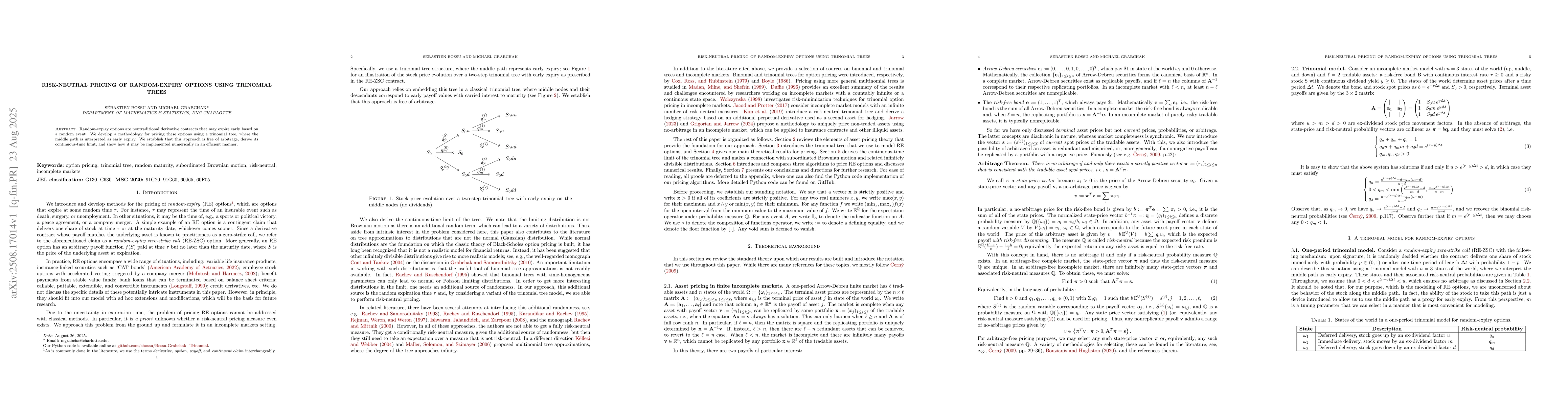

Random-expiry options are nontraditional derivative contracts that may expire early based on a random event. We develop a methodology for pricing these options using a trinomial tree, where the middle...

We develop the first exact and computationally tractable method for simulating from tempered stable distributions in the infinite variation case, which corresponds to $α\in[1,2)$. A small simulation s...