Academic Profile

Statistics

Similar Authors

Papers on arXiv

We discuss model and forecast combination in time series forecasting. A foundational Bayesian perspective based on agent opinion analysis theory defines a new framework for density forecast combinat...

The recently introduced class of simultaneous graphical dynamic linear models (SGDLMs) defines an ability to scale on-line Bayesian analysis and forecasting to higher-dimensional time series. This p...

We discuss Bayesian analysis of multivariate time series with dynamic factor models that exploit time-adaptive sparsity in model parametrizations via the latent threshold approach. One central focus...

We discuss probabilistic models of random covariance structures defined by distributions over sparse eigenmatrices. The decomposition of orthogonal matrices in terms of Givens rotations defines a na...

We discuss Bayesian forecasting of increasingly high-dimensional time series, a key area of application of stochastic dynamic models in the financial industry and allied areas of business. Novel sta...

We discuss the Bayesian emulation approach to computational solution of multi-step portfolio studies in financial time series. "Bayesian emulation for decisions" involves mapping the technical struc...

Traffic flow count data in networks arise in many applications, such as automobile or aviation transportation, certain directed social network contexts, and Internet studies. Using an example of Int...

The macroeconomy is a sophisticated dynamic system involving significant uncertainties that complicate modelling. In response, decision makers consider multiple models that provide different predict...

Theoretical developments in sequential Bayesian analysis of multivariate dynamic models underlie new methodology for causal prediction. This extends the utility of existing models with computational...

We discuss and develop Bayesian dynamic modelling and predictive decision synthesis for portfolio analysis. The context involves model uncertainty with a set of candidate models for financial time s...

We are most grateful to all discussants for their positive comments and many thought-provoking questions. In addition, the discussants provide a number of useful leads into various areas of the lite...

Bayesian forecasting is developed in multivariate time series analysis for causal inference. Causal evaluation of sequentially observed time series data from control and treated units focuses on the...

Entropic tilting (ET) is a Bayesian decision-analytic method for constraining distributions to satisfy defined targets or bounds for sets of expectations. This report recapitulates the foundations a...

Decision-guided perspectives on model uncertainty expand traditional statistical thinking about managing, comparing and combining inferences from sets of models. Bayesian predictive decision synthes...

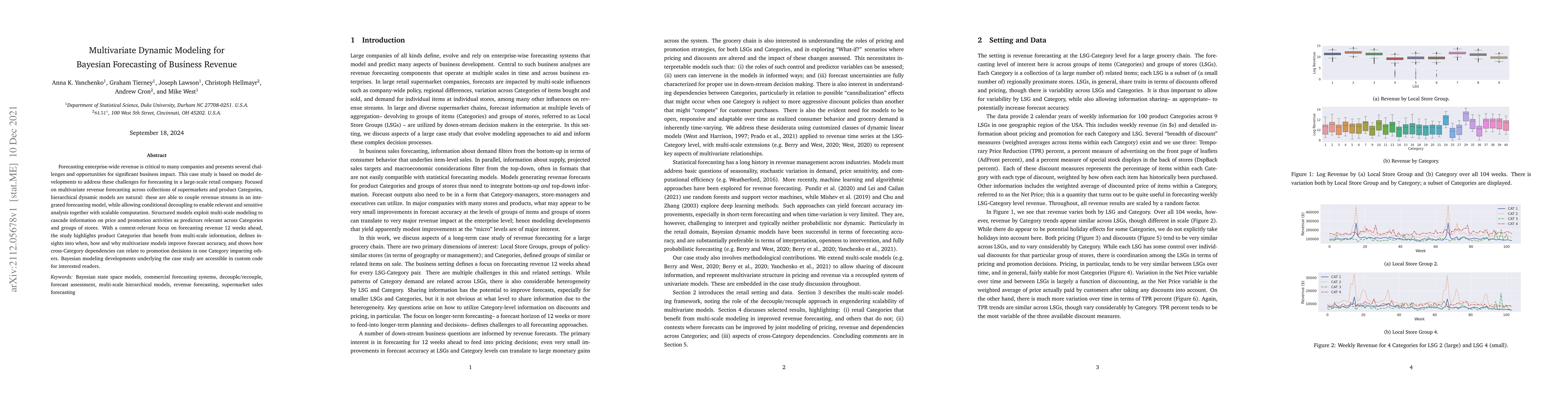

Forecasting enterprise-wide revenue is critical to many companies and presents several challenges and opportunities for significant business impact. This case study is based on model developments to...

We present a case study and methodological developments in large-scale hierarchical dynamic modeling for personalized prediction in commerce. The context is supermarket sales, where improved forecas...

This expository paper discusses Bayesian decision analysis perspectives on problems of constrained forecasting. Foundational and pedagogic discussion contrasts decision analytic approaches with the ...

Bayesian computation for filtering and forecasting analysis is developed for a broad class of dynamic models. The ability to scale-up such analyses in non-Gaussian, nonlinear multivariate time serie...

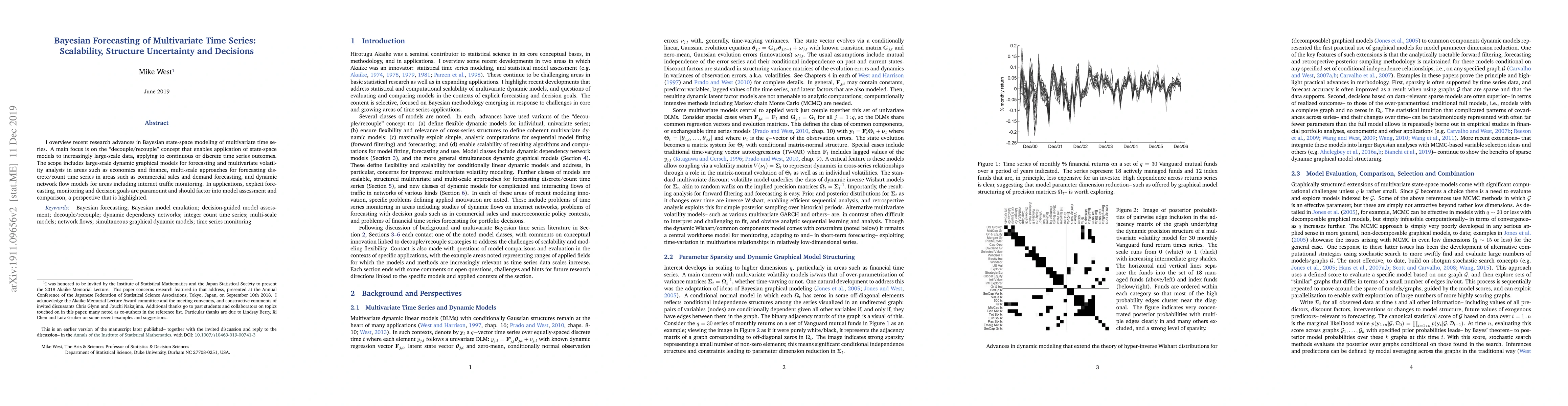

I overview recent research advances in Bayesian state-space modeling of multivariate time series. A main focus is on the decouple/recouple concept that enables application of state-space models to i...

We discuss Bayesian model uncertainty analysis and forecasting in sequential dynamic modeling of multivariate time series. The perspective is that of a decision-maker with a specific forecasting obj...

We present new Bayesian methodology for consumer sales forecasting. With a focus on multi-step ahead forecasting of daily sales of many supermarket items, we adapt dynamic count mixture models to fo...

This paper develops forecasting methodology and application of new classes of dynamic models for time series of non-negative counts. Novel univariate models synthesise dynamic generalized linear mod...

In the context of a motivating study of dynamic network flow data on a large-scale e-commerce web site, we develop Bayesian models for on-line/sequential analysis for monitoring and adapting to chan...

This paper reviews background and examples of Bayesian predictive synthesis (BPS), and develops details in a subset of BPS mixture models. BPS expands on standard Bayesian model uncertainty analysis...

We develop the methodology and a detailed case study in use of a class of Bayesian predictive synthesis (BPS) models for multivariate time series forecasting. This extends the recently introduced fo...

Simultaneous graphical dynamic linear models (SGDLMs) provide advances in flexibility, parsimony and scalability of multivariate time series analysis, with proven utility in forecasting. Core theoreti...

We introduce methodology to bridge scenario analysis and model-based risk forecasting, leveraging their respective strengths in policy settings. Our Bayesian framework addresses the fundamental challe...

We present a new class of Bayesian dynamic models for bivariate price-realized volatility time series in financial forecasting. A novel dynamic gamma process model adopted for realized volatility is i...

We discuss probabilistic measures of concordance between two probability distributions based on the expected misclassification rate (EMR). The focus is on comparing a given reference distribution with...

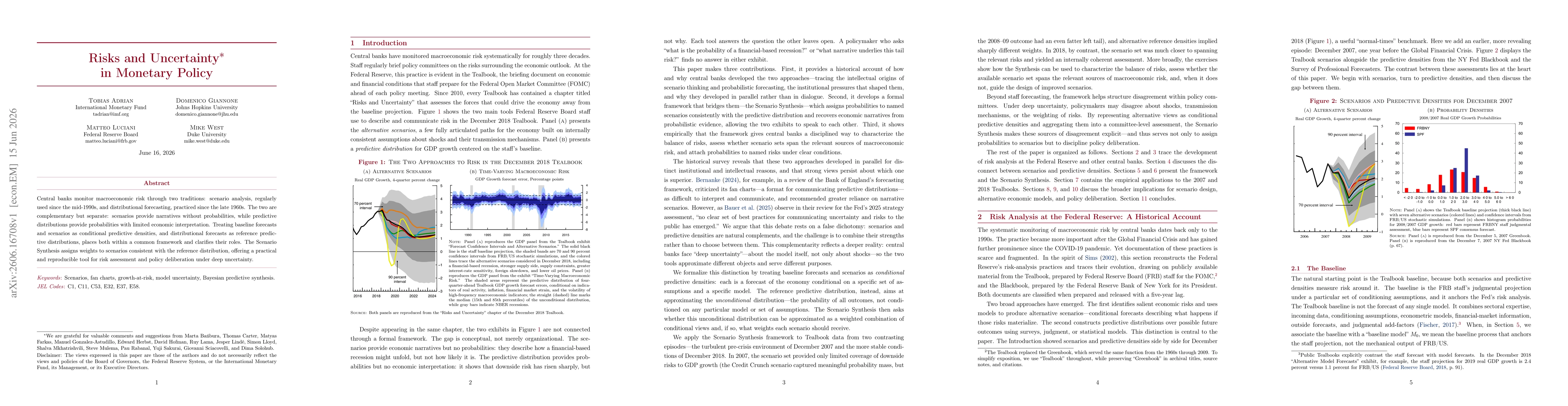

Central banks monitor macroeconomic risk through two traditions: scenario analysis, regularly used since the mid-1990s, and distributional forecasting, practiced since the late 1960s. The two are comp...