Academic Profile

Statistics

Similar Authors

Papers on arXiv

Speeding up Markov Chain Monte Carlo (MCMC) for datasets with many observations by data subsampling has recently received considerable attention. A pseudo-marginal MCMC method is proposed that estim...

Synthetic likelihood is an attractive approach to likelihood-free inference when an approximately Gaussian summary statistic for the data, informative for inference about the parameters, is availabl...

A semi-parametric joint Value-at-Risk (VaR) and Expected Shortfall (ES) forecasting framework employing multiple realized measures is developed. The proposed framework extends the realized exponenti...

For years, researchers investigated the applications of deep learning in forecasting financial time series. However, they continued to rely on the conventional econometric approach for model trainin...

The Bayesian Synthetic Likelihood (BSL) method is a widely-used tool for likelihood-free Bayesian inference. This method assumes that some summary statistics are normally distributed, which can be i...

The Mean Field Variational Bayes (MFVB) method is one of the most computationally efficient techniques for Bayesian inference. However, its use has been restricted to models with conjugate priors or...

Evidence accumulation models (EAMs) are an important class of cognitive models used to analyze both response time and response choice data recorded from decision-making tasks. Developments in estima...

We propose a new approach to volatility modeling by combining deep learning (LSTM) and realized volatility measures. This LSTM-enhanced realized GARCH framework incorporates and distills modeling ad...

Quantum computers promise to surpass the most powerful classical supercomputers when it comes to solving many critically important practical problems, such as pharmaceutical and fertilizer design, s...

Variational Bayes (VB) is a critical method in machine learning and statistics, underpinning the recent success of Bayesian deep learning. The natural gradient is an essential component of efficient...

This tutorial gives a quick introduction to Variational Bayes (VB), also called Variational Inference or Variational Approximation, from a practical point of view. The paper covers a range of common...

In this study, we investigate learning rate adaption at different levels based on the hyper-gradient descent framework and propose a method that adaptively learns the optimizer parameters by combini...

A common method for assessing validity of Bayesian sampling or approximate inference methods makes use of simulated data replicates for parameters drawn from the prior. Under continuity assumptions,...

Bayesian inference using Markov Chain Monte Carlo (MCMC) on large datasets has developed rapidly in recent years. However, the underlying methods are generally limited to relatively simple settings ...

Variational Bayes (VB) has become a widely-used tool for Bayesian inference in statistics and machine learning. Nonetheless, the development of the existing VB algorithms is so far generally restric...

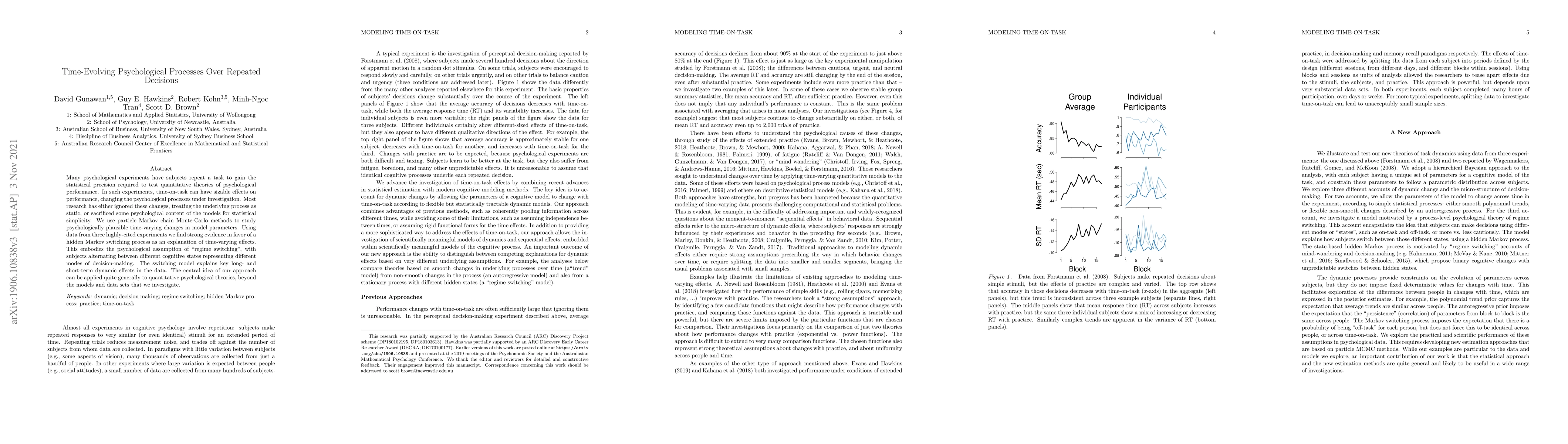

Many psychological experiments have subjects repeat a task to gain the statistical precision required to test quantitative theories of psychological performance. In such experiments, time-on-task ca...

The Stochastic Volatility (SV) model and its variants are widely used in the financial sector while recurrent neural network (RNN) models are successfully used in many large-scale industrial applica...

Gaussian variational approximation is a popular methodology to approximate posterior distributions in Bayesian inference especially in high dimensional and large data settings. To control the comput...

We show how to speed up Sequential Monte Carlo (SMC) for Bayesian inference in large data problems by data subsampling. SMC sequentially updates a cloud of particles through a sequence of distributi...

A long memory and non-linear realized volatility model class is proposed for direct Value at Risk (VaR) forecasting. This model, referred to as RNN-HAR, extends the heterogeneous autoregressive (HAR) ...

This paper introduces a novel multivariate volatility modeling framework, named Long Short-Term Memory enhanced BEKK (LSTM-BEKK), that integrates deep learning into multivariate GARCH processes. By co...

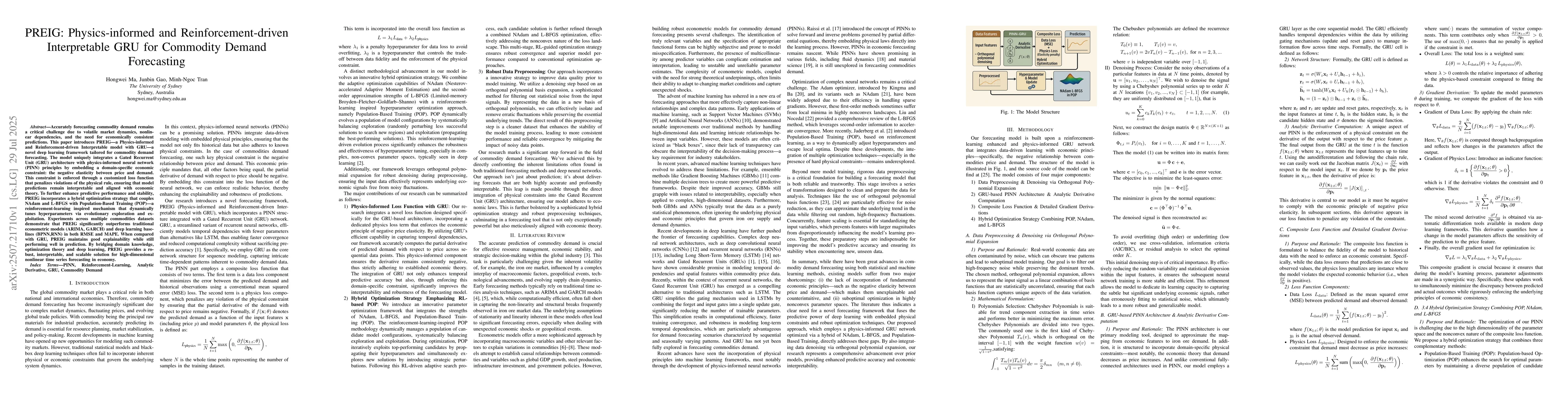

Accurately forecasting commodity demand remains a critical challenge due to volatile market dynamics, nonlinear dependencies, and the need for economically consistent predictions. This paper introduce...

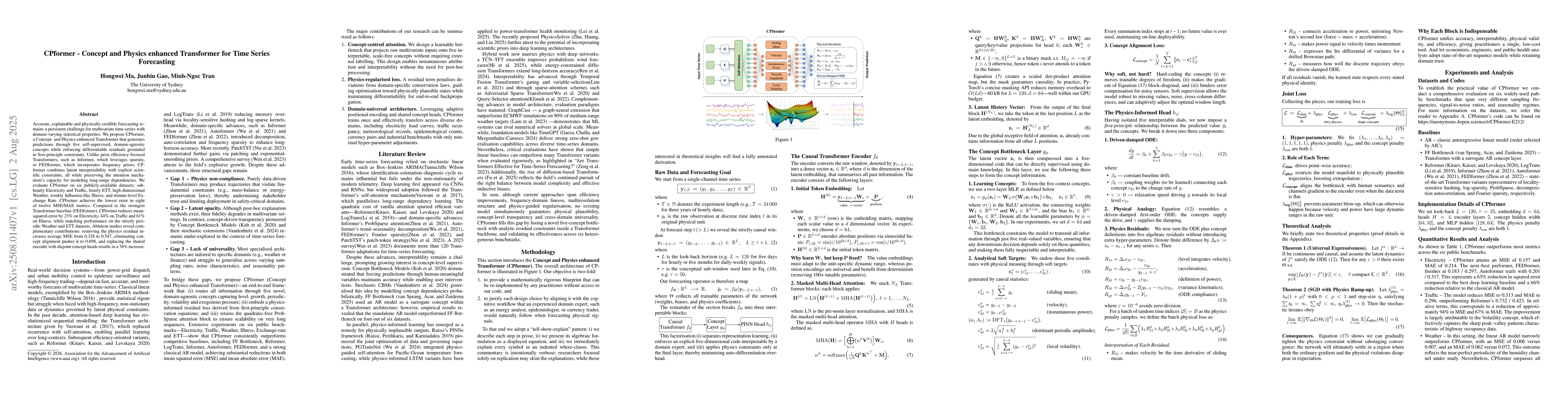

Accurate, explainable and physically-credible forecasting remains a persistent challenge for multivariate time-series whose statistical properties vary across domains. We present CPformer, a Concept- ...

The Importance-Weighted Evidence Lower Bound (IW-ELBO) has emerged as an effective objective for variational inference (VI), tightening the standard ELBO and mitigating the mode-seeking behaviour. H...

This paper studies the optimization of the KL functional on the Wasserstein space of probability measures, and develops a sampling framework based on Wasserstein gradient descent (WGD). We identify tw...

Importance weighted variational inference (VI) approximates densities known up to a normalizing constant by optimizing bounds that tighten with the number of Monte Carlo samples $N$. Standard optimiza...

The natural gradient method is widely used in statistical optimization, but its standard formulation assumes a Euclidean parameter space. This paper proposes an inversion-free stochastic natural gradi...

Exponential smoothing (ES) often outperforms other techniques in time series forecasting across a wide range of data-generating processes. While ES has traditionally been applied to time series in $\m...