Academic Profile

Statistics

Similar Authors

Papers on arXiv

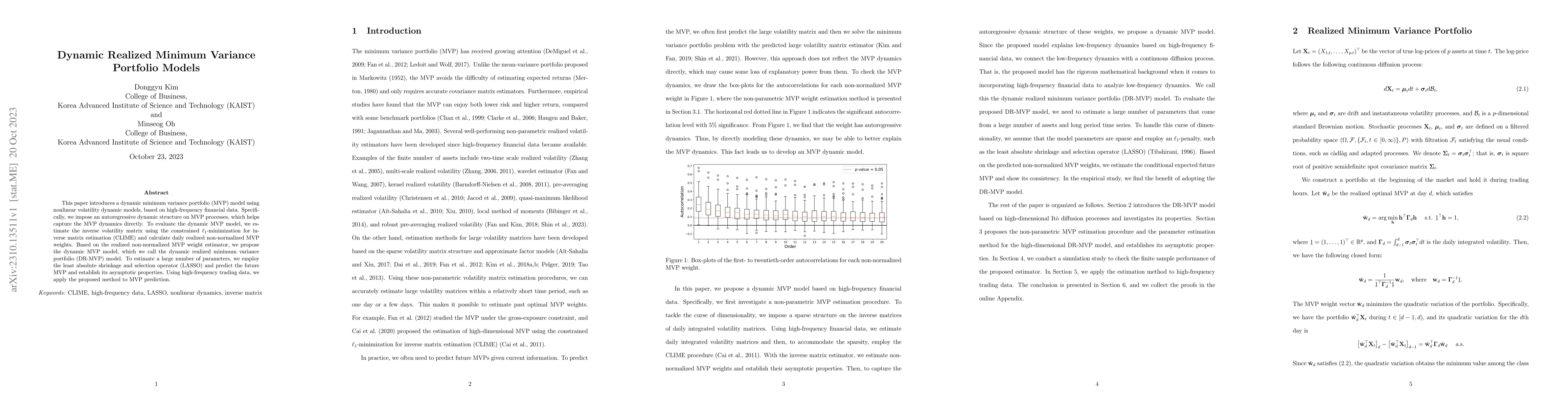

This paper introduces a dynamic minimum variance portfolio (MVP) model using nonlinear volatility dynamic models, based on high-frequency financial data. Specifically, we impose an autoregressive dy...

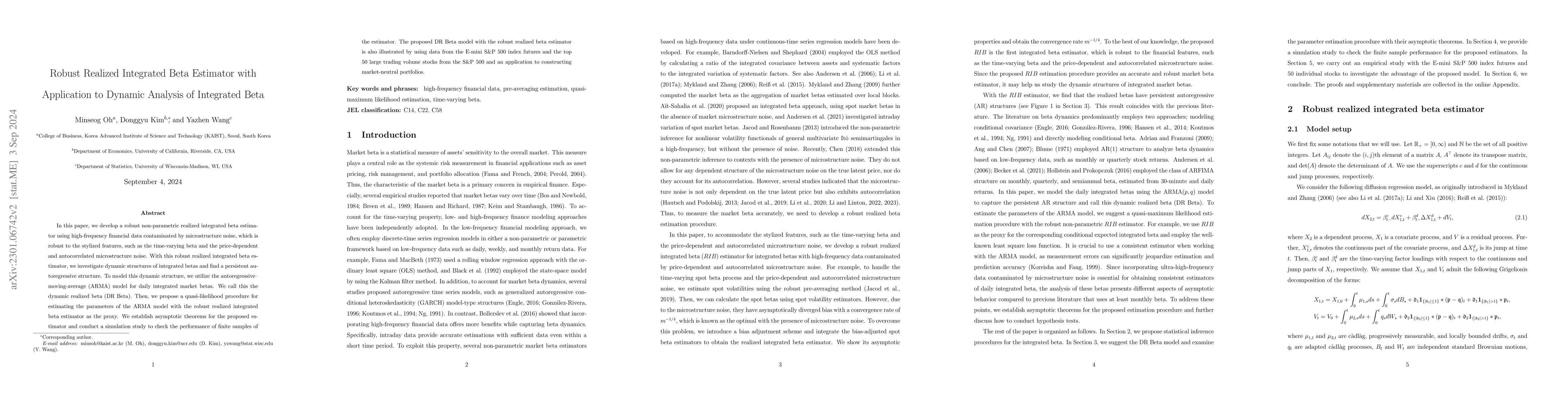

In this paper, we develop a robust non-parametric realized integrated beta estimator using high-frequency financial data contaminated by microstructure noises, which is robust to the stylized featur...

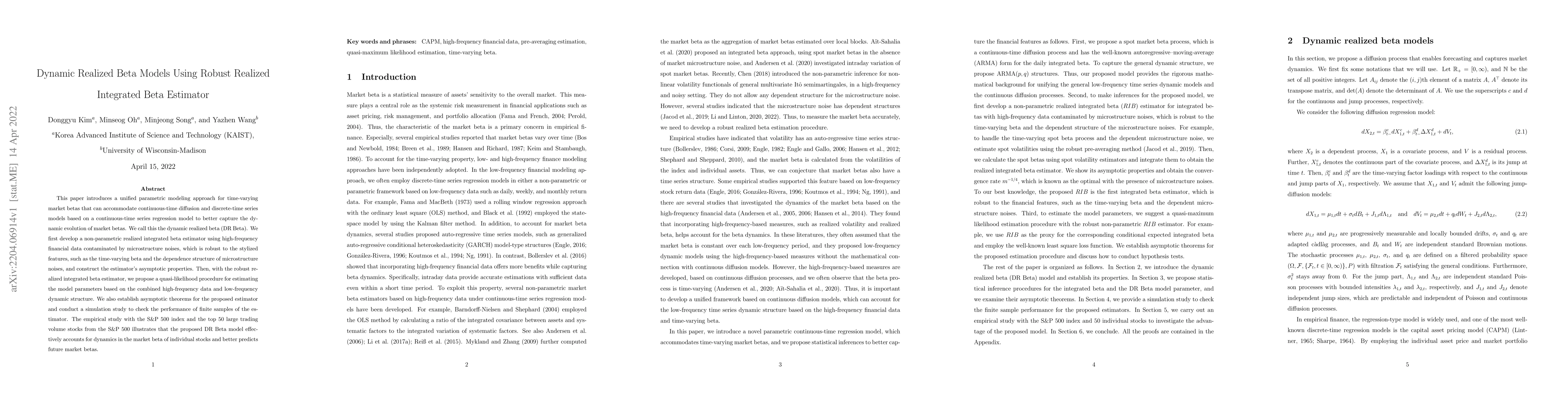

This paper introduces a unified parametric modeling approach for time-varying market betas that can accommodate continuous-time diffusion and discrete-time series models based on a continuous-time s...

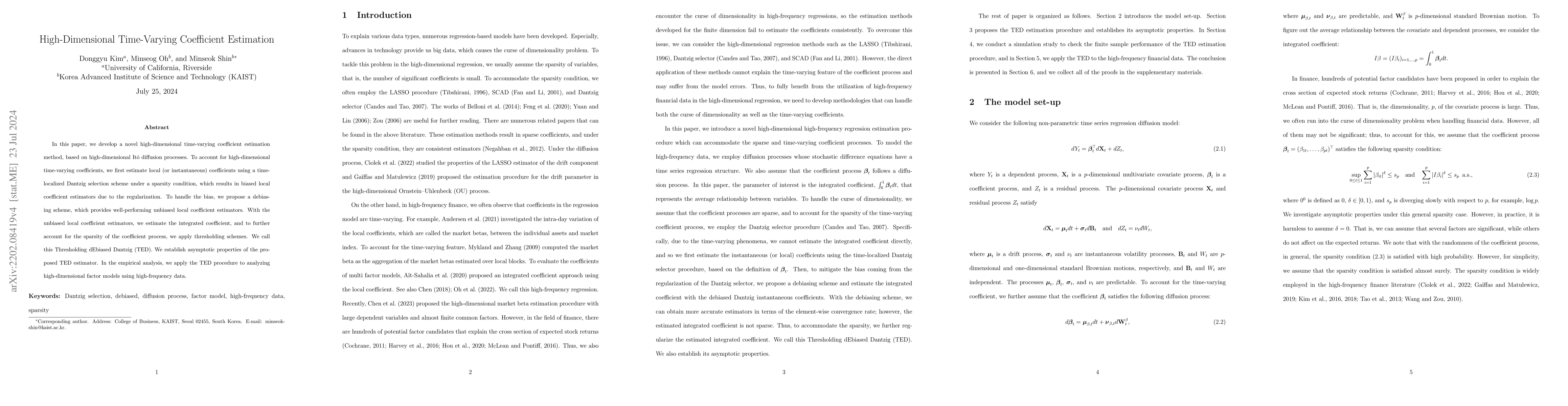

In this paper, we develop a novel high-dimensional time-varying coefficient estimation method, based on high-dimensional Ito diffusion processes. To account for high-dimensional time-varying coeffic...

In this paper, we investigate the effect of the U.S.--China trade war on stock markets from a financial contagion perspective, based on high-frequency financial data. Specifically, to account for ri...

This paper introduces a novel quantile approach to harness the high-frequency information and improve the daily conditional quantile estimation. Specifically, we model the conditional standard devia...

In financial applications, we often observe both global and local factors that are modeled by a multi-level factor model. When detecting unknown local group memberships under such a model, employing a...