Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper axiomatizes, in a two-stage setup, a new theory for decision under risk and ambiguity. The axiomatized preference relation $\succeq$ on the space $\tilde{V}$ of random variables induces a...

We derive consistency and asymptotic normality results for quasi-maximum likelihood methods for drift parameters of ergodic stochastic processes observed in discrete time in an underlying continuous...

Demographic changes increase the necessity to base the pension system more and more on the second and the third pillar, namely the occupational and private pension plans; this paper deals with Targe...

We develop a method to solve, theoretically and numerically, general optimal stopping problems. Our general setting allows for multiple exercise rights, i.e., optimal multiple stopping, for a robust...

We consider an expected utility maximization problem where the utility function is not necessarily concave and the time horizon is uncertain. We establish a necessary and sufficient condition for th...

We study the expected utility maximization problem of a large investor who is allowed to make transactions on tradable assets in an incomplete financial market with endogenous permanent market impac...

We study a non-concave optimization problem in which a financial company maximizes the expected utility of the surplus under a risk-based regulatory constraint. For this problem, we consider four di...

Suppose an investor aims at Delta hedging a European contingent claim $h(S(T))$ in a jump-diffusion model, but incorrectly specifies the stock price's volatility and jump sensitivity, so that any he...

We consider a time-consistent mean-variance portfolio selection problem of an insurer and allow for the incorporation of basis (mortality) risk. The optimal solution is identified with a Nash subgam...

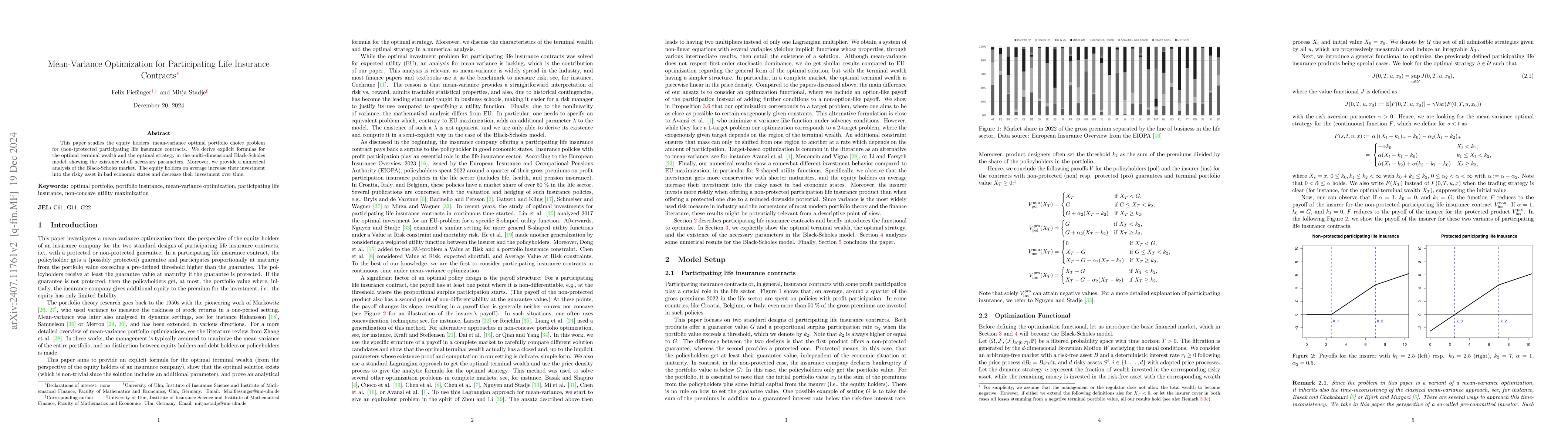

This paper studies the equity holders' mean-variance optimal portfolio choice problem for (non-)protected participating life insurance contracts. We derive explicit formulas for the optimal terminal w...

We introduce a model-free preference under ambiguity, as a primitive trait of behavior, which we apply once as well as repeatedly. Its single and double application yield simple, easily interpretable ...

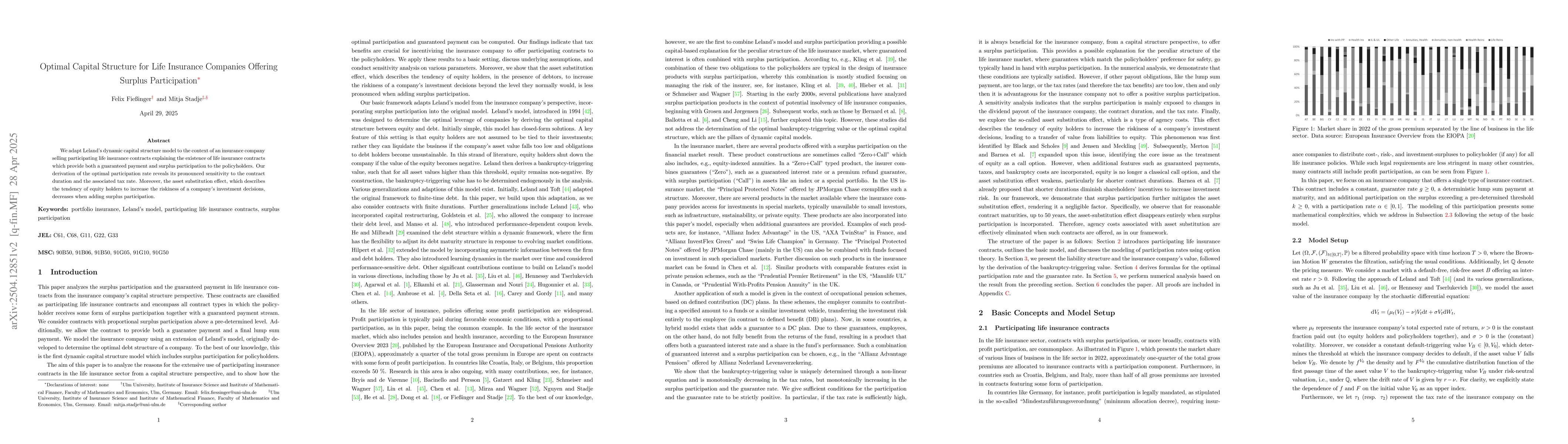

We adapt Leland's dynamic capital structure model to the context of an insurance company selling participating life insurance contracts explaining the existence of life insurance contracts which provi...