Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper proposes a simple method to extract from a set of multiple related time series a compressed representation for each time series based on statistics for the entire set of all time series. ...

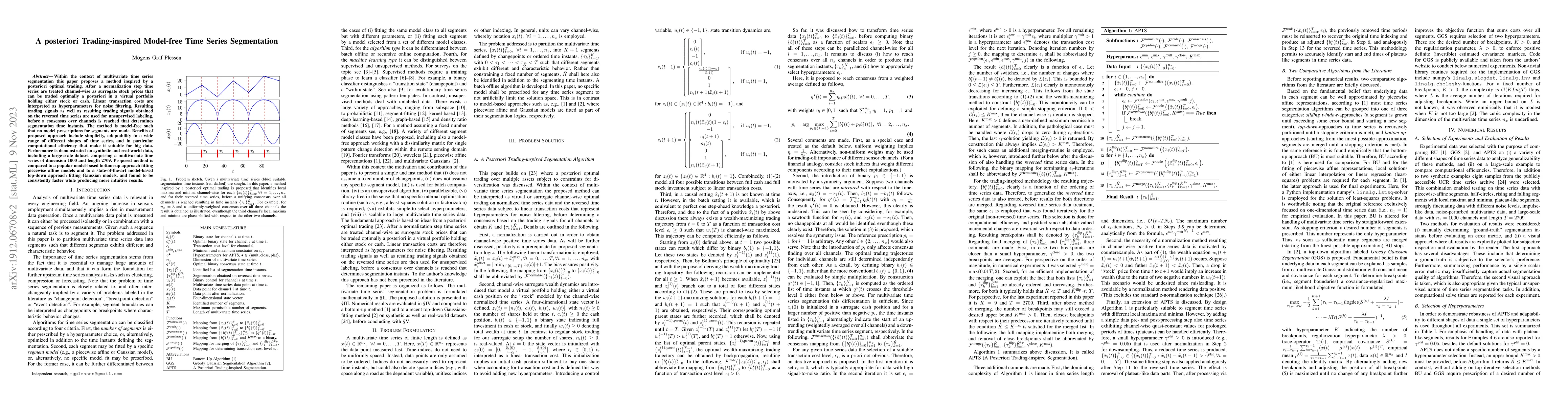

Within the context of multivariate time series segmentation this paper proposes a method inspired by a posteriori optimal trading. After a normalization step time series are treated channel-wise as ...

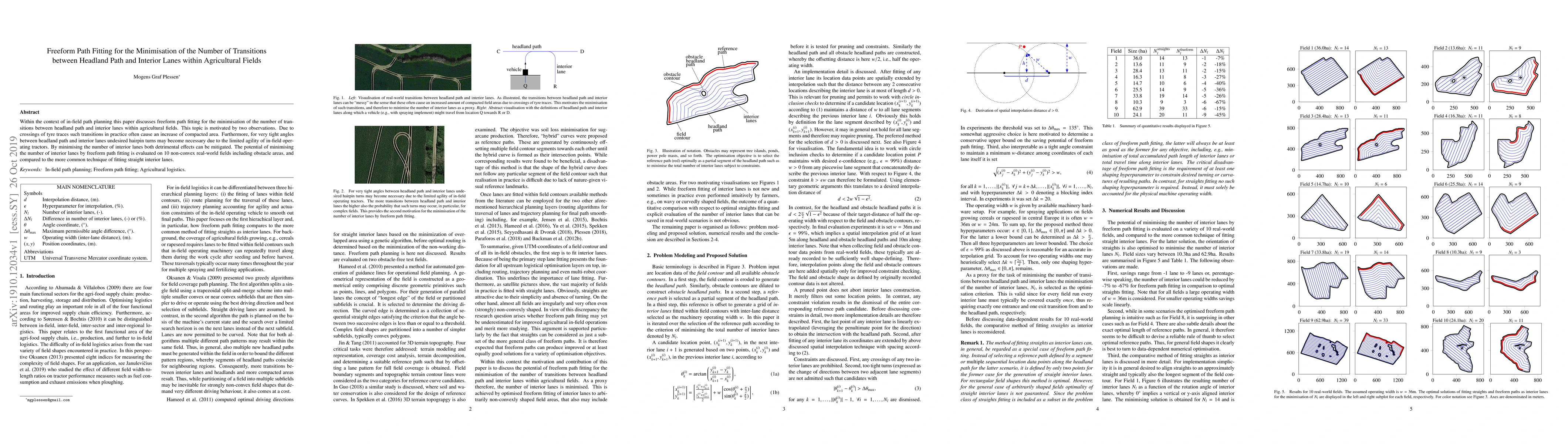

Within the context of in-field path planning this paper discusses freeform path fitting for the minimisation of the number of transitions between headland path and interior lanes within agricultural...