Academic Profile

Statistics

Similar Authors

Papers on arXiv

It has been recently discovered that some random processes may satisfy limit theorems even though they exhibit intermittency, namely an unusual growth of moments. In this paper we provide a deeper u...

This is a survey of recent results on central and non-central limit theorems for quadratic functionals of stationary processes. The underlying processes are Gaussian, linear or L\'evy-driven linear ...

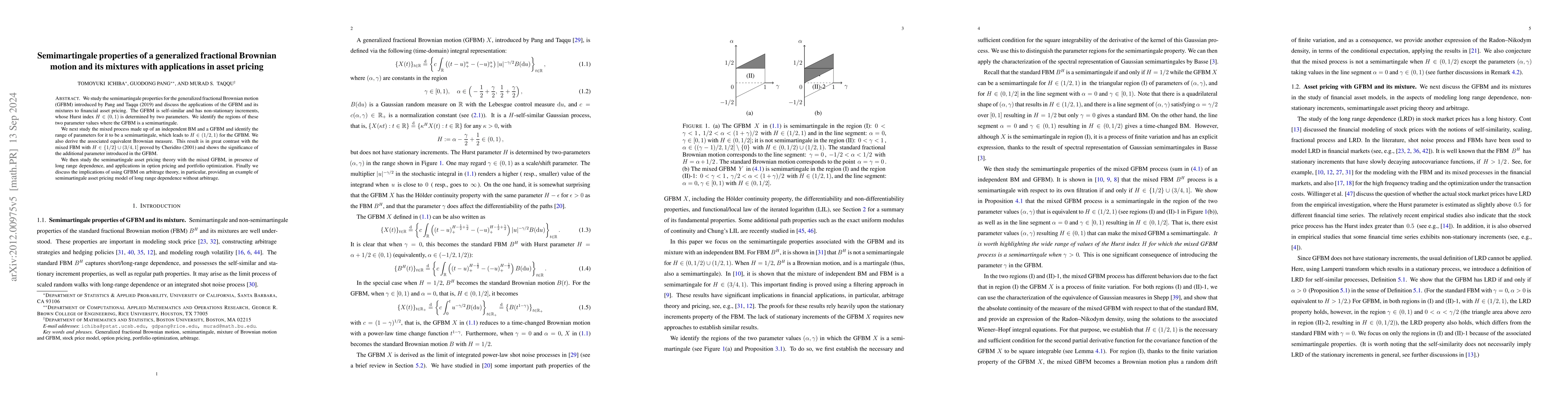

We study the semimartingale properties for the generalized fractional Brownian motion (GFBM) introduced by Pang and Taqqu (2019) and discuss the applications of the GFBM and its mixtures to financia...

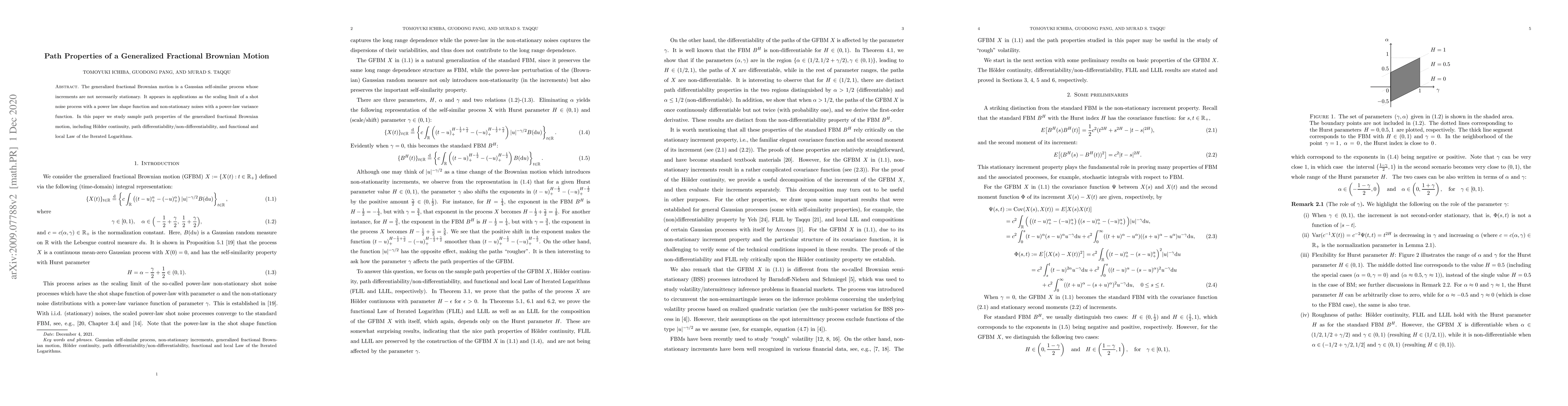

The generalized fractional Brownian motion is a Gaussian self-similar process whose increments are not necessarily stationary. It appears in applications as the scaling limit of a shot noise process...

One of the main problem in prediction theory of discrete-time second-order stationary processes $X(t)$ is to describe the asymptotic behavior of the best linear mean squared prediction error in pred...