Academic Profile

Statistics

Similar Authors

Papers on arXiv

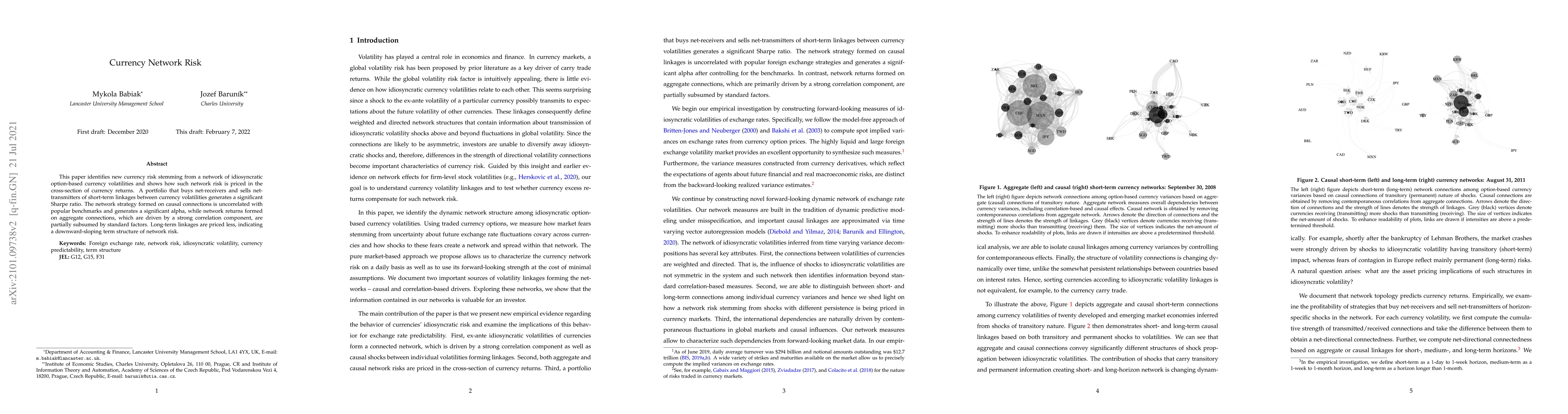

This paper identifies new currency risk stemming from a network of idiosyncratic option-based currency volatilities and shows how such network risk is priced in the cross-section of currency returns...

We study dynamic portfolio choice of a long-horizon investor who uses deep learning methods to predict equity returns when forming optimal portfolios. Our results show statistically and economically...

Cross-sectional dispersion in firm-level realized skewness is significantly and negatively related to future stock market returns. The predictive power of skewness dispersion is robust to in-sample an...