2

arXiv Papers

3

Total Publications

Profile

Academic Profile

Metrics

Statistics

2

arXiv Papers

3

Total Publications

Network

Similar Authors

Publications

Papers on arXiv

arXiv

Correlation scenarios and correlation stress testing

We develop a general approach for stress testing correlations of financial asset portfolios. The correlation matrix of asset returns is specified in a parametric form, where correlations are represe...

arXiv

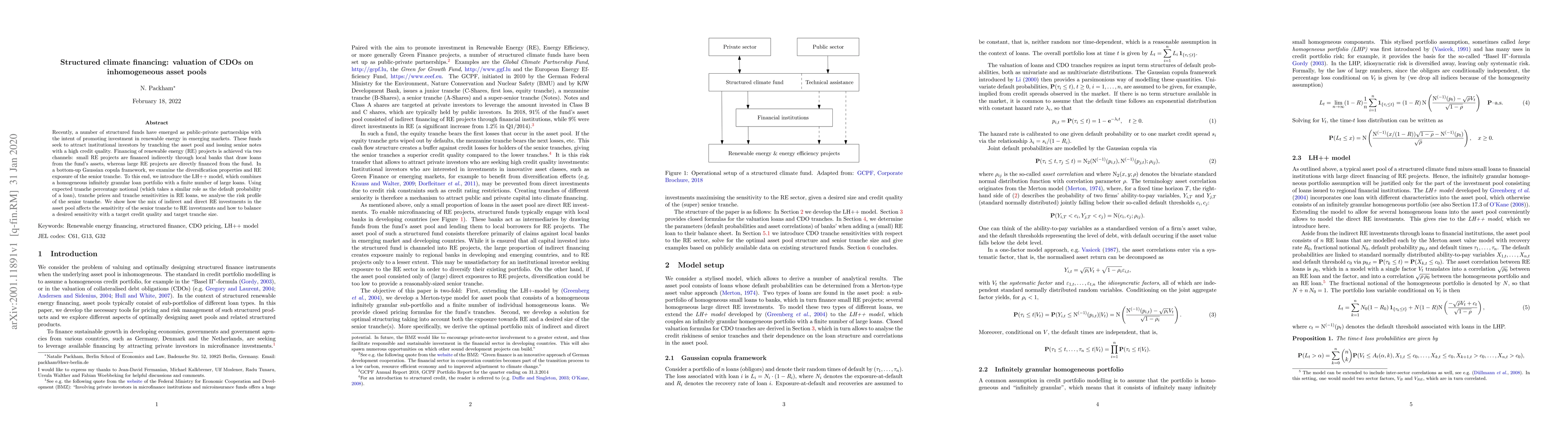

Structured climate financing: valuation of CDOs on inhomogeneous asset

pools

Recently, a number of structured funds have emerged as public-private partnerships with the intent of promoting investment in renewable energy in emerging markets. These funds seek to attract instit...