Nalini Ravishanker

6 papers on arXiv

Academic Profile

Statistics

Similar Authors

Papers on arXiv

Modeling Multiple Irregularly Spaced Financial Time Series

In this paper we propose univariate volatility models for irregularly spaced financial time series by modifying the regularly spaced stochastic volatility models. We also extend this approach to pro...

Modeling Multivariate Positive-Valued Time Series Using R-INLA

In this paper we describe fast Bayesian statistical analysis of vector positive-valued time series, with application to interesting financial data streams. We discuss a flexible level correlated mod...

Anomaly Detection in Energy Usage Patterns

Energy usage monitoring on higher education campuses is an important step for providing satisfactory service, lowering costs and supporting the move to green energy. We present a collaboration betwe...

Spatiotemporal Analysis of Ridesourcing and Taxi Demand by Taxi zones in New York City

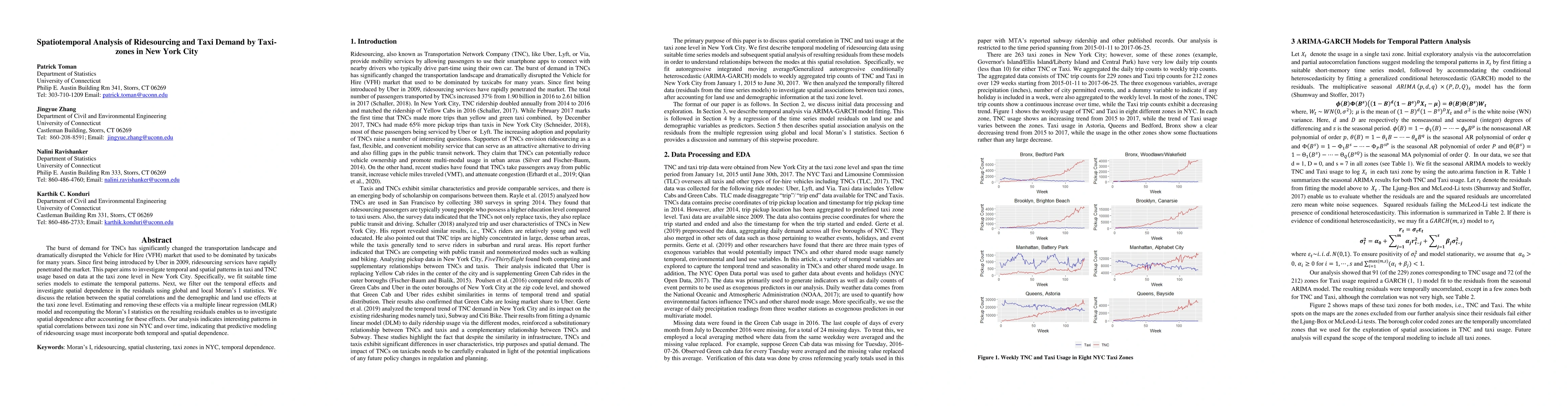

The burst of demand for TNCs has significantly changed the transportation landscape and dramatically disrupted the Vehicle for Hire (VFH) market that used to be dominated by taxicabs for many years....

Nonlinear Time Series Classification Using Bispectrum-based Deep Convolutional Neural Networks

Time series classification using novel techniques has experienced a recent resurgence and growing interest from statisticians, subject-domain scientists, and decision makers in business and industry...

Topological Data Analysis (TDA) for Time Series

The study of topology is strictly speaking, a topic in pure mathematics. However in only a few years, Topological Data Analysis (TDA), which refers to methods of utilizing topological features in da...