Academic Profile

Statistics

Similar Authors

Papers on arXiv

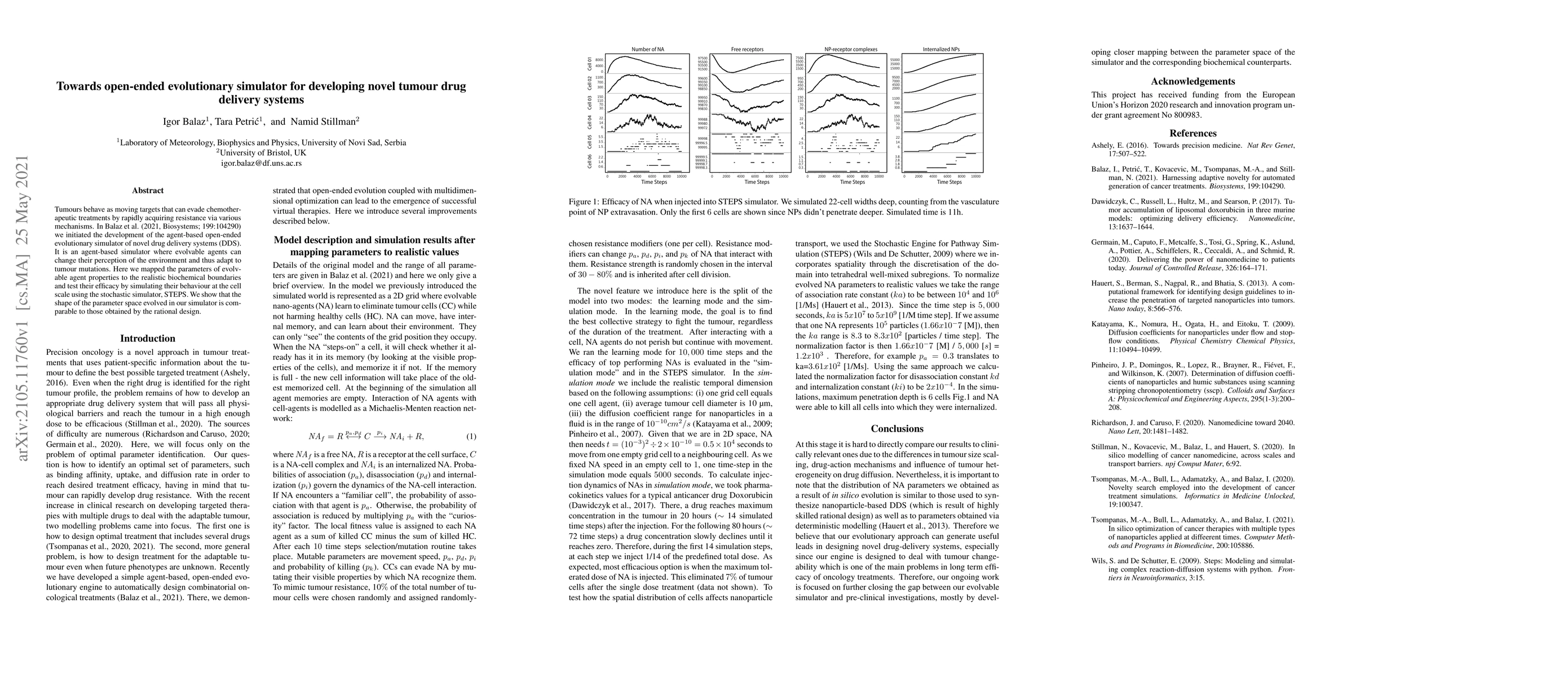

Tumours behave as moving targets that can evade chemotherapeutic treatments by rapidly acquiring resistance via various mechanisms. In Balaz et al. (2021, Biosystems; 199:104290) we initiated the de...

We present the EVONANO platform for the evolution of nanomedicines with application to anti-cancer treatments. EVONANO includes a simulator to grow tumours, extract representative scenarios, and the...

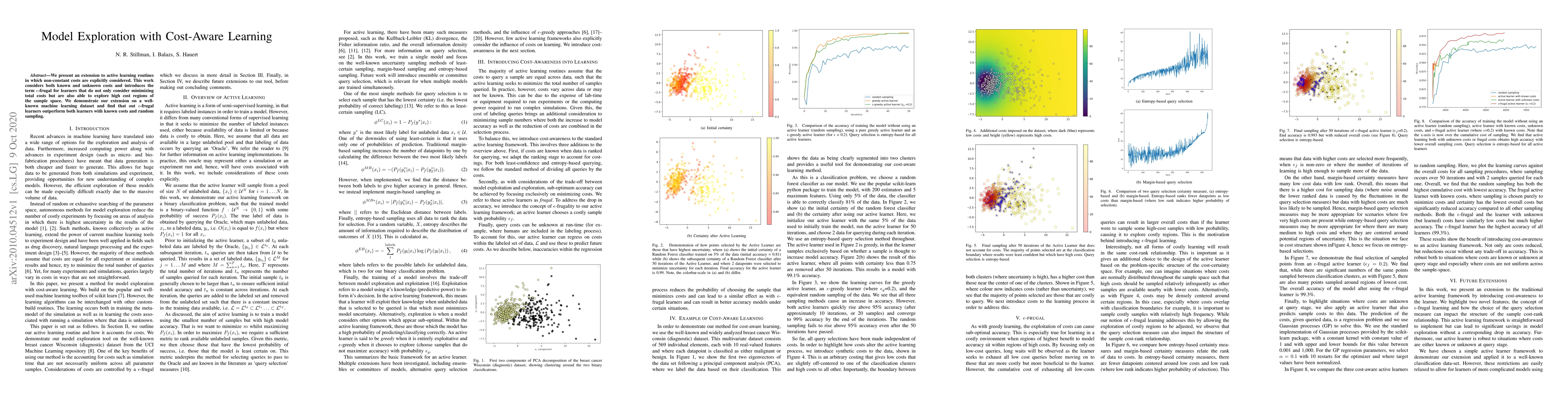

We present an extension to active learning routines in which non-constant costs are explicitly considered. This work considers both known and unknown costs and introduces the term \epsilon-frugal fo...

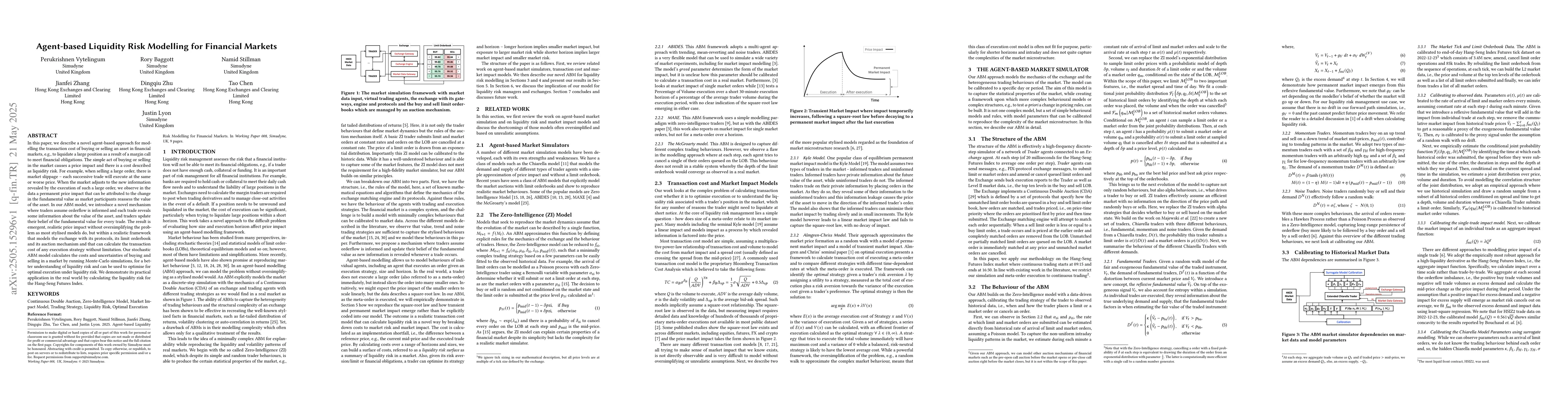

In this paper, we describe a novel agent-based approach for modelling the transaction cost of buying or selling an asset in financial markets, e.g., to liquidate a large position as a result of a marg...

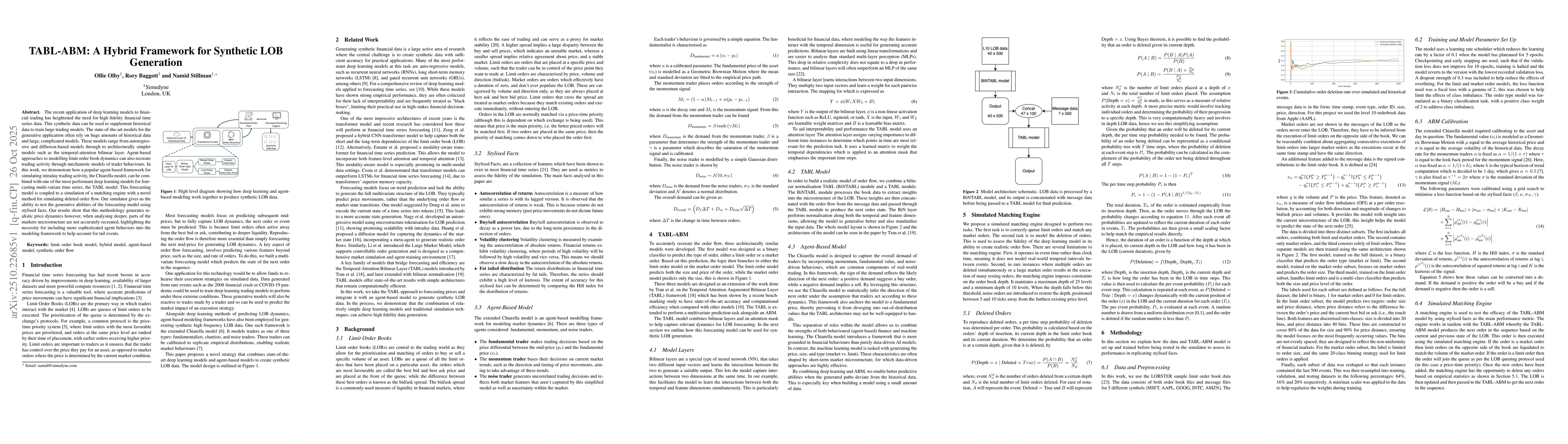

The recent application of deep learning models to financial trading has heightened the need for high fidelity financial time series data. This synthetic data can be used to supplement historical data ...

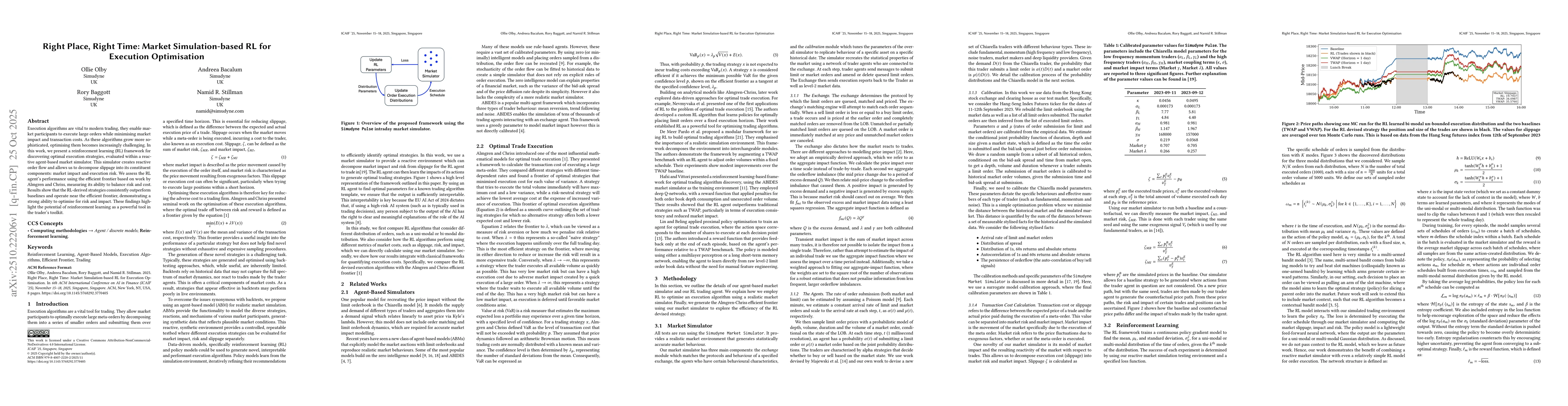

Execution algorithms are vital to modern trading, they enable market participants to execute large orders while minimising market impact and transaction costs. As these algorithms grow more sophistica...