Academic Profile

Statistics

Similar Authors

Papers on arXiv

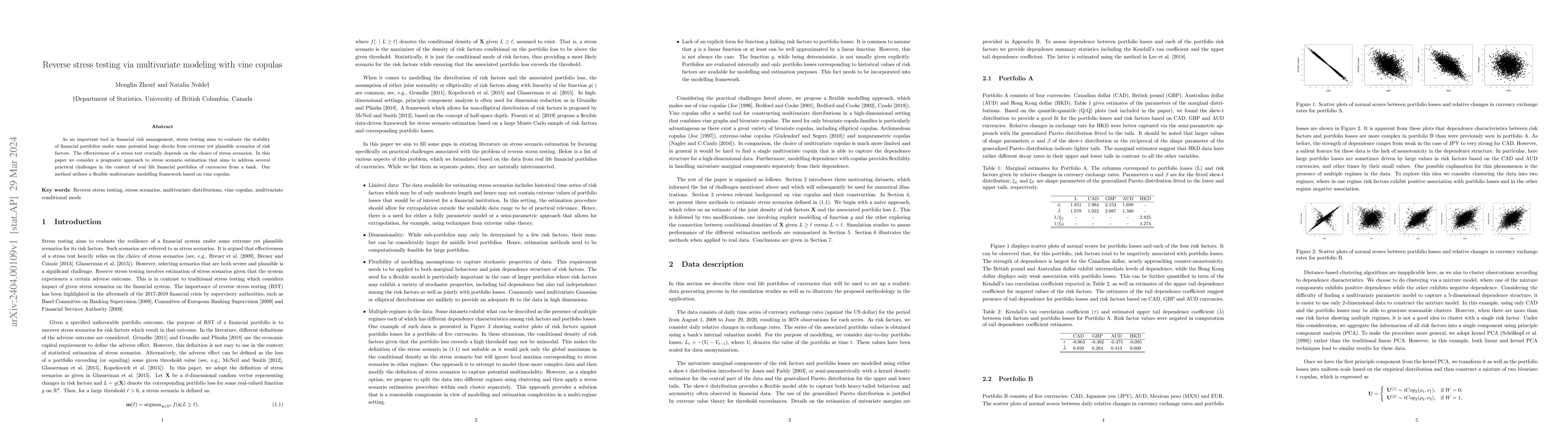

As an important tool in financial risk management, stress testing aims to evaluate the stability of financial portfolios under some potential large shocks from extreme yet plausible scenarios of ris...

A regime-switching multivariate time series model which is closed under margins is built. The model imposes a restriction on all lower-dimensional sub-processes to follow a regime-switching process ...

Conditions are obtained for a Gaussian vector autoregressive time series of order $k$, VAR($k$), to have univariate margins that are autoregressive of order $k$ or lower-dimensional margins that are...

The global financial crisis of 2007-2009 highlighted the crucial role systemic risk plays in ensuring stability of financial markets. Accurate assessment of systemic risk would enable regulators to ...

Accurate modeling of operational risk is important for a bank and the finance industry as a whole to prepare for potentially catastrophic losses. One approach to modeling operational is the loss dis...

The study of multivariate extremes is dominated by multivariate regular variation, although it is well known that this approach does not provide adequate distinction between random vectors whose com...

Panel data arise in a wide range of application areas, and developing modelling methods for extreme values under such a setup is essential for reliable risk assessment and management. When choosing to...

The tail index parameter of heavy-tailed probability models plays a key role in characterizing the tail decay of the underlying distribution function and is often involved in extrapolation procedures ...