Academic Profile

Statistics

Similar Authors

Papers on arXiv

Portfolio managers' orders trade off return and trading cost predictions. Return predictions rely on alpha models, whereas price impact models quantify trading costs. This paper studies what happens...

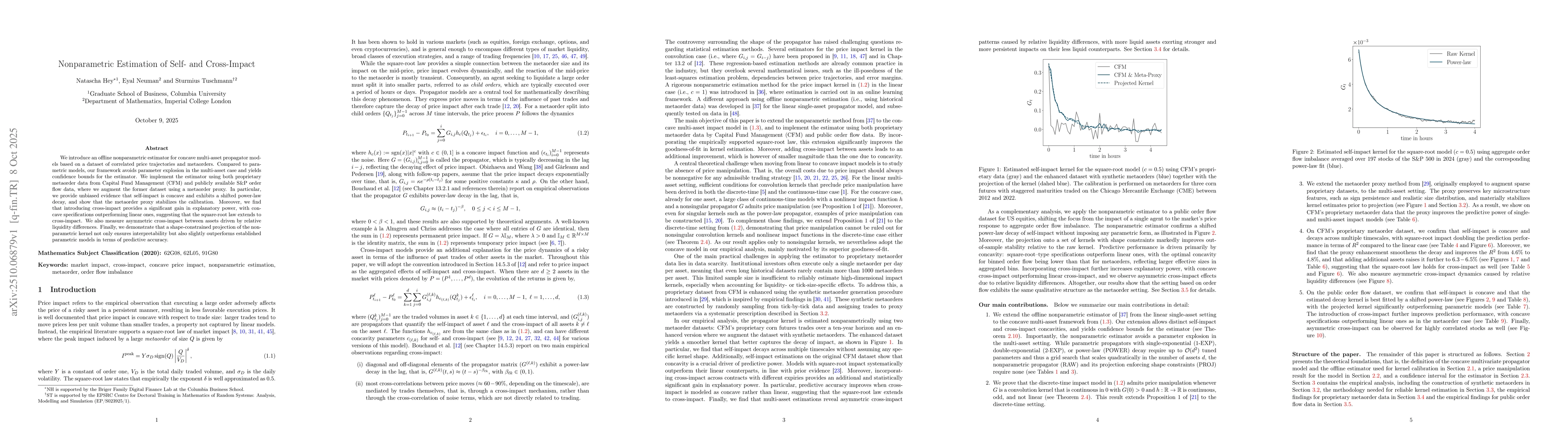

We introduce an offline nonparametric estimator for concave multi-asset propagator models based on a dataset of correlated price trajectories and metaorders. Compared to parametric models, our framewo...

Auto-deleveraging (ADL) mechanisms are a critical yet understudied component of risk management on cryptocurrency futures exchanges. When available margin and other loss-absorbing resources are insuff...