Academic Profile

Statistics

Similar Authors

Papers on arXiv

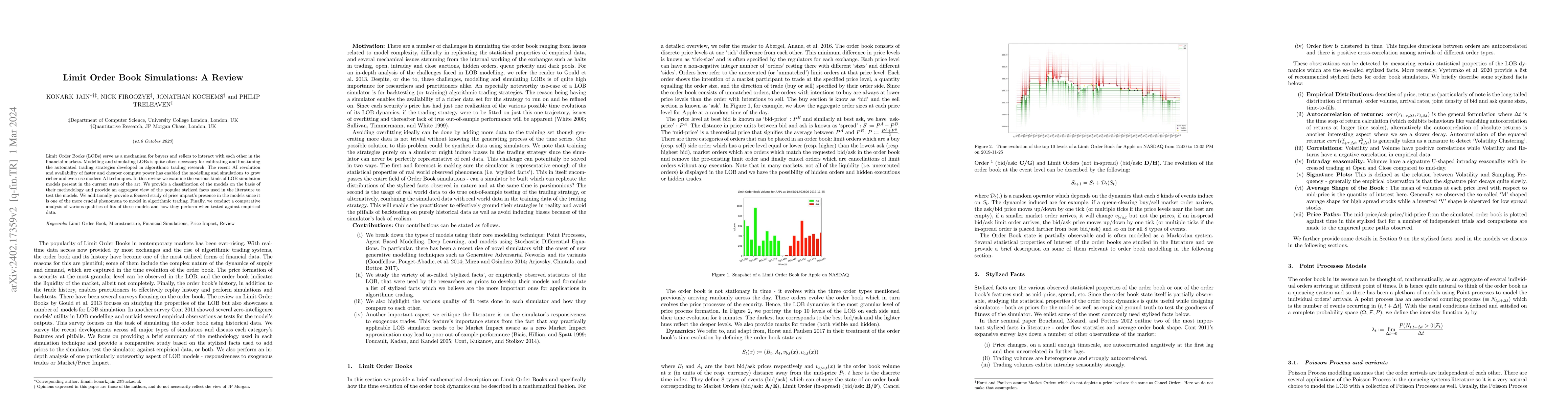

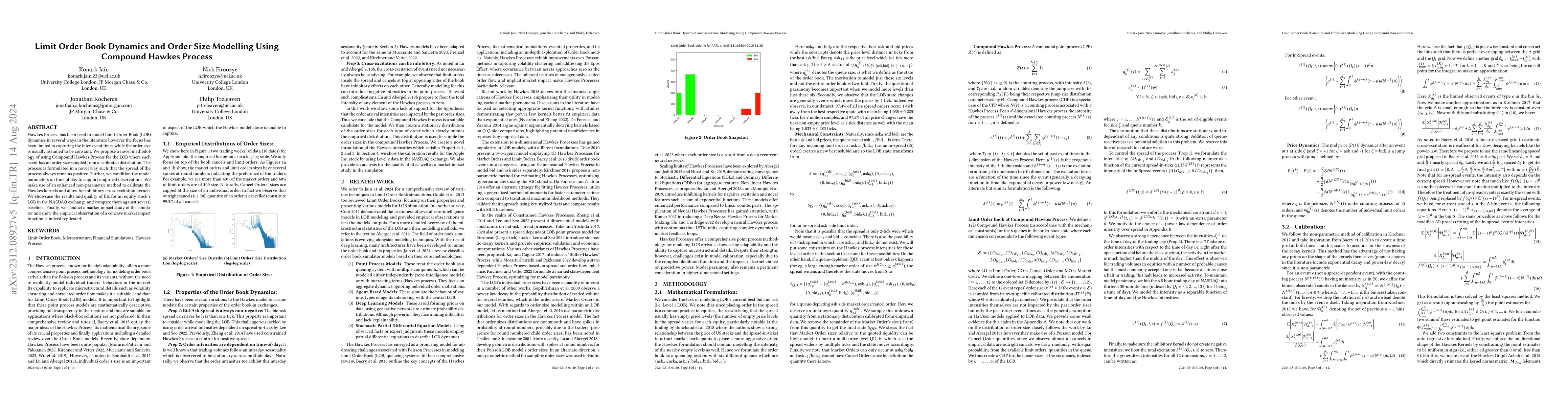

Limit Order Books (LOBs) serve as a mechanism for buyers and sellers to interact with each other in the financial markets. Modelling and simulating LOBs is quite often necessary for calibrating and ...

Hawkes Process has been used to model Limit Order Book (LOB) dynamics in several ways in the literature however the focus has been limited to capturing the inter-event times while the order size is ...

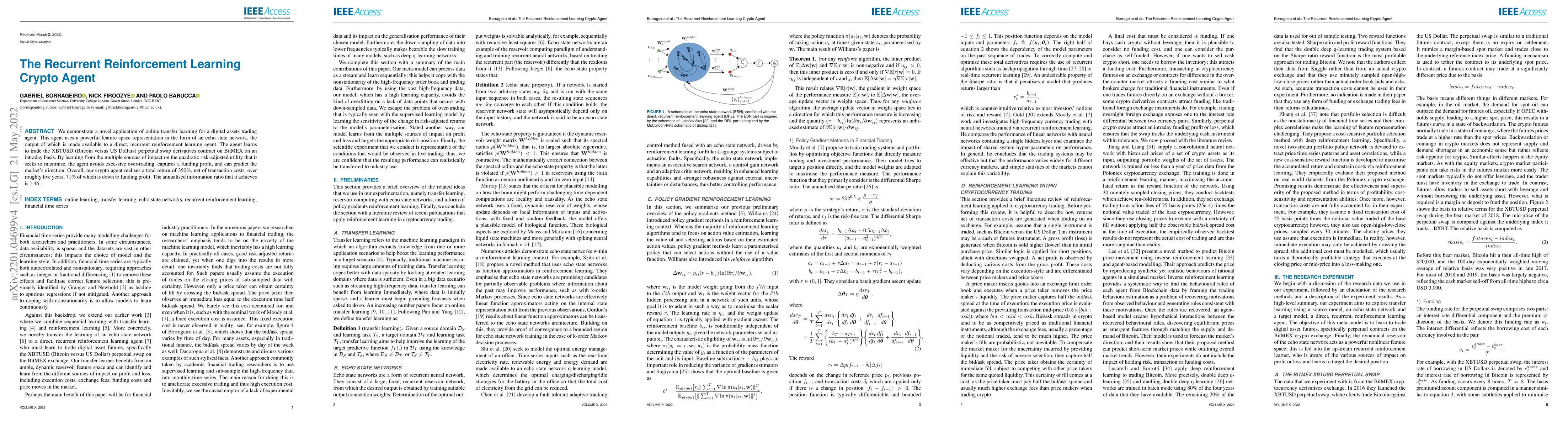

We demonstrate a novel application of online transfer learning for a digital assets trading agent. This agent uses a powerful feature space representation in the form of an echo state network, the o...

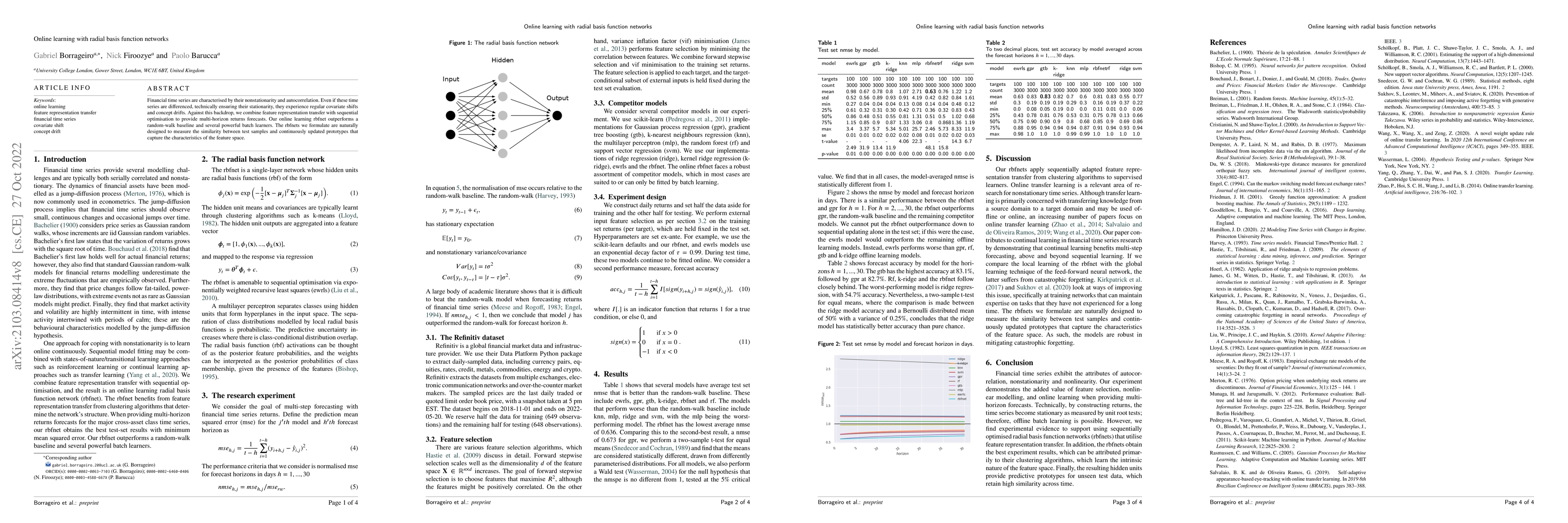

We explore online inductive transfer learning, with a feature representation transfer from a radial basis function network formed of Gaussian mixture model hidden processing units to a direct, recur...

Financial time series are characterised by their nonstationarity and autocorrelation. Even if these time series are differenced, technically ensuring their stationarity, they experience regular cova...

Systematic financial trading strategies account for over 80% of trade volume in equities and a large chunk of the foreign exchange market. In spite of the availability of data from multiple markets,...

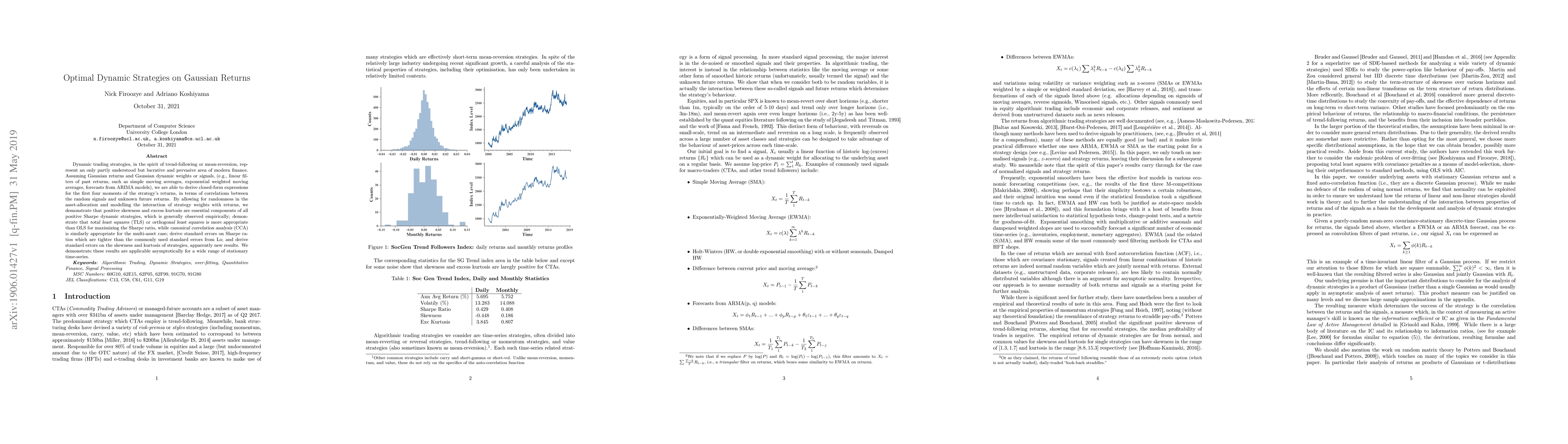

Dynamic trading strategies, in the spirit of trend-following or mean-reversion, represent an only partly understood but lucrative and pervasive area of modern finance. Assuming Gaussian returns and ...

Robust optimization provides a principled framework for decision-making under uncertainty, with broad applications in finance, engineering, and operations research. In portfolio optimization, uncertai...

We study the optimal Market Making problem in a Limit Order Book (LOB) market simulated using a high-fidelity, mutually exciting Hawkes process. Departing from traditional Brownian-driven mid-price mo...

We investigate the mechanisms by which medium-frequency trading agents are adversely selected by opportunistic high-frequency traders. We use reinforcement learning (RL) within a Hawkes Limit Order Bo...

Overparameterized models have recently challenged conventional learning theory by exhibiting improved generalization beyond the interpolation limit, a phenomenon known as benign overfitting. This work...