The Recurrent Reinforcement Learning Crypto Agent

Publication

Metrics

AI Quick Summary

This paper presents a crypto trading agent utilizing online transfer learning and recurrent reinforcement learning to trade Bitcoin perpetual swaps, achieving a 350% total return over five years, largely due to funding profit, with an annualized information ratio of 1.46. The agent effectively manages risk and predicts market direction.

Paper Preview

Abstract

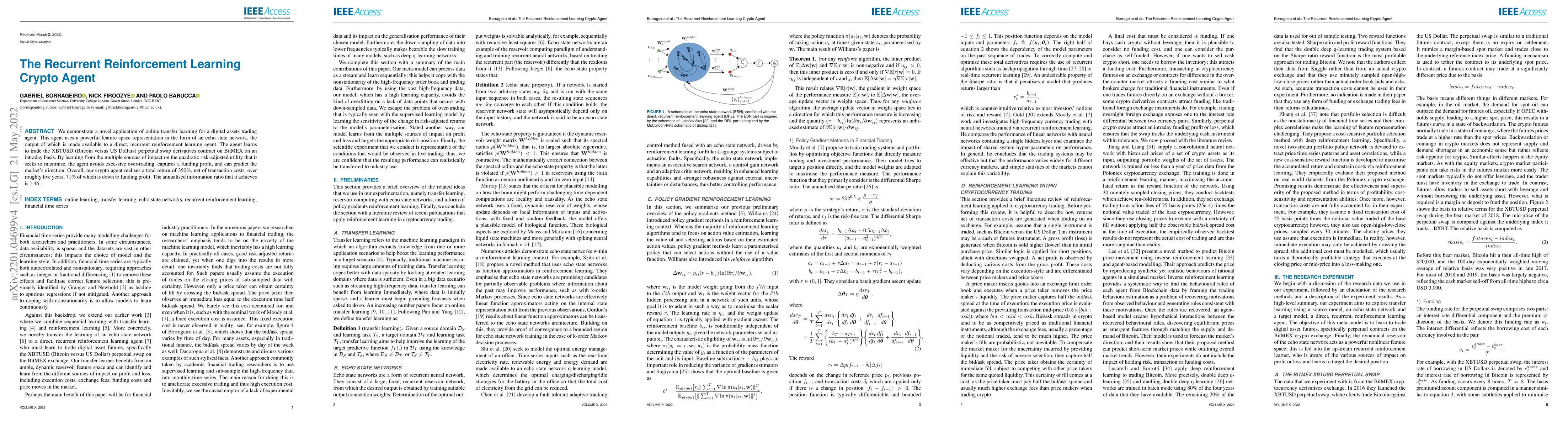

We demonstrate a novel application of online transfer learning for a digital assets trading agent. This agent uses a powerful feature space representation in the form of an echo state network, the output of which is made available to a direct, recurrent reinforcement learning agent. The agent learns to trade the XBTUSD (Bitcoin versus US Dollars) perpetual swap derivatives contract on BitMEX on an intraday basis. By learning from the multiple sources of impact on the quadratic risk-adjusted utility that it seeks to maximise, the agent avoids excessive over-trading, captures a funding profit, and can predict the market's direction. Overall, our crypto agent realises a total return of 350\%, net of transaction costs, over roughly five years, 71\% of which is down to funding profit. The annualised information ratio that it achieves is 1.46.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0