Academic Profile

Statistics

Similar Authors

Papers on arXiv

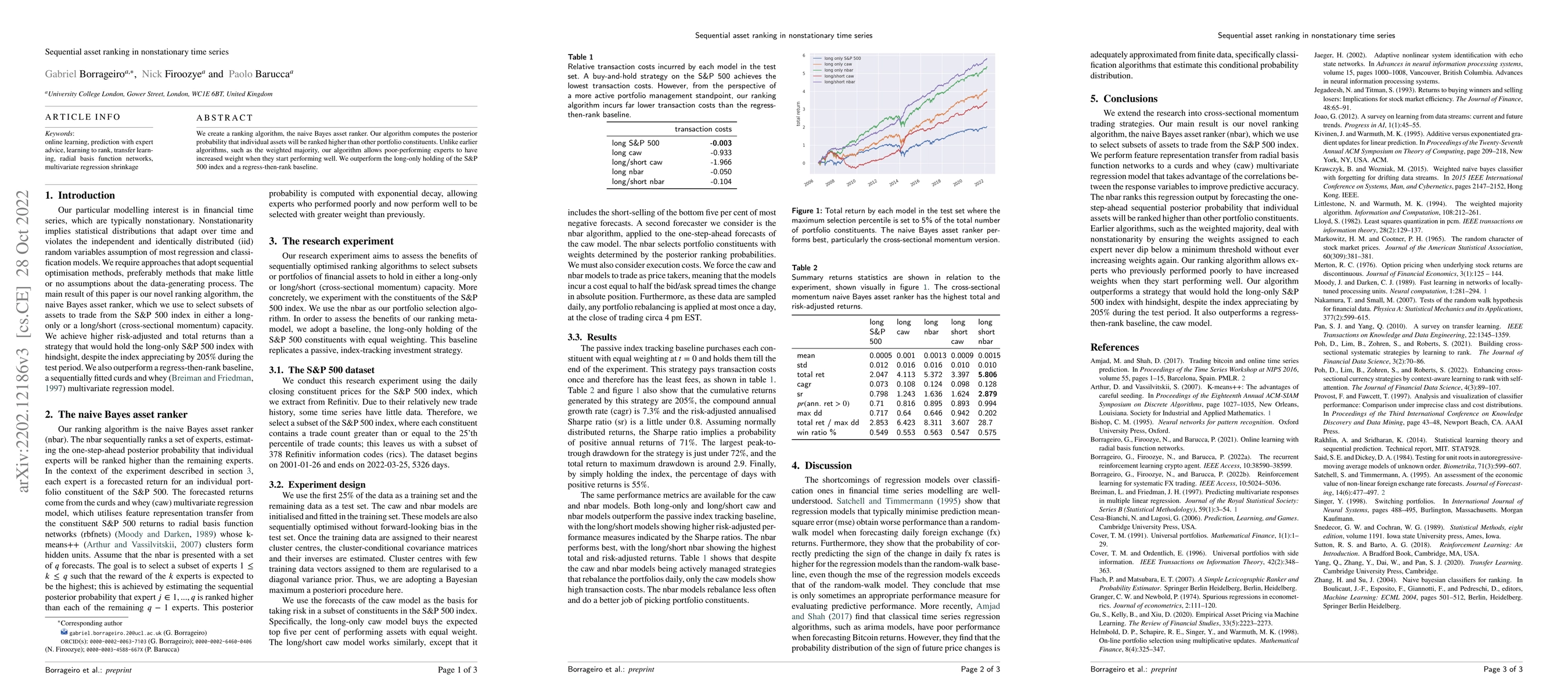

We create a ranking algorithm, the naive Bayes asset ranker. Our algorithm computes the posterior probability that individual assets will be ranked higher than other portfolio constituents. Unlike e...

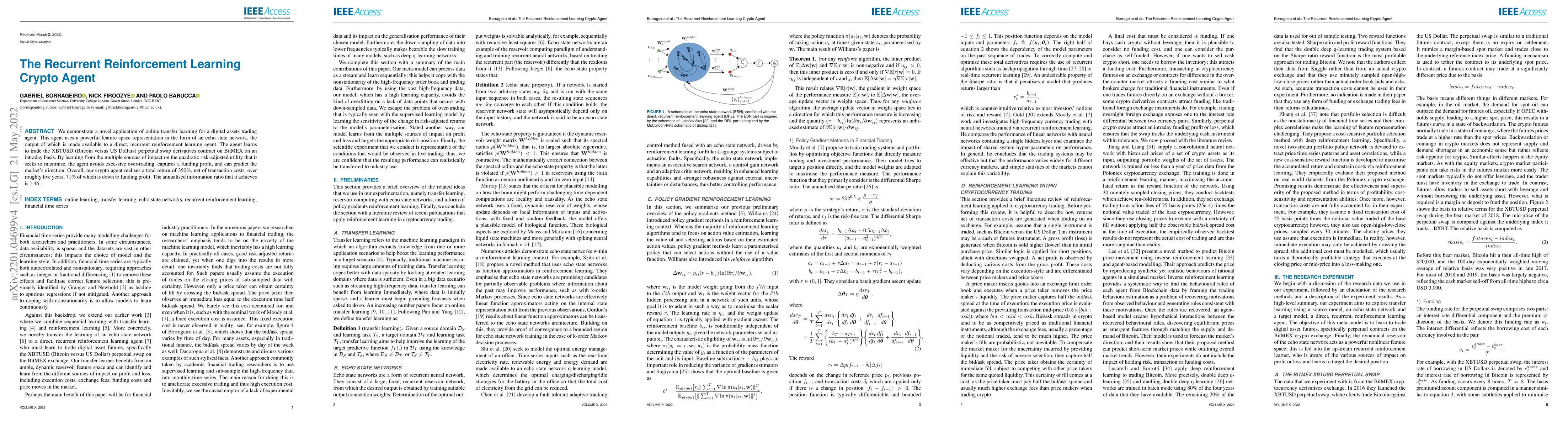

We demonstrate a novel application of online transfer learning for a digital assets trading agent. This agent uses a powerful feature space representation in the form of an echo state network, the o...

We explore online inductive transfer learning, with a feature representation transfer from a radial basis function network formed of Gaussian mixture model hidden processing units to a direct, recur...

Financial time series are characterised by their nonstationarity and autocorrelation. Even if these time series are differenced, technically ensuring their stationarity, they experience regular cova...