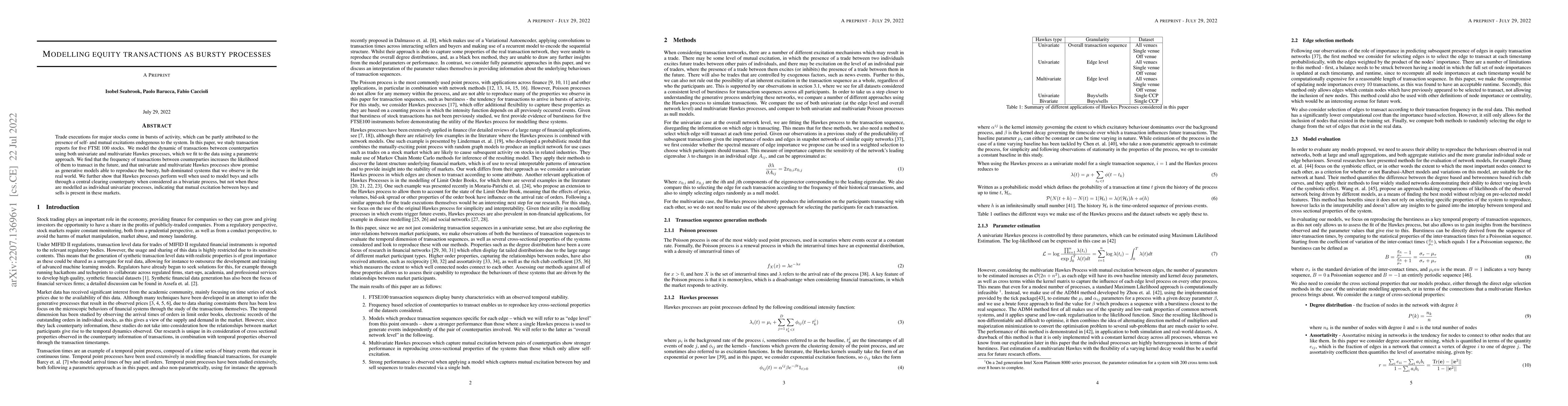

Academic Profile

Statistics

Similar Authors

Papers on arXiv

We introduce a general model for the balance-sheet consistent valuation of interbank claims within an interconnected financial system. Our model represents an extension of clearing models of interde...

We process private equity transactions to predict public market behavior with a logit model. Specifically, we estimate our model to predict quarterly returns for both the broad market and for indivi...

Volatility smile and skewness are two key properties of option prices that are represented by the implied volatility (IV) surface. However, IV surface calibration through nonlinear interpolation is ...

Trade executions for major stocks come in bursts of activity, which can be partly attributed to the presence of self- and mutual excitations endogenous to the system. In this paper, we study transac...

The transition from defined benefit to defined contribution pension plans shifts the responsibility for saving toward retirement from governments and institutions to the individuals. Determining opt...

We propose Variational Heteroscedastic Volatility Model (VHVM) -- an end-to-end neural network architecture capable of modelling heteroscedastic behaviour in multivariate financial time series. VHVM...

Inferring causal relationships in observational time series data is an important task when interventions cannot be performed. Granger causality is a popular framework to infer potential causal mecha...

We propose Neural GARCH, a class of methods to model conditional heteroskedasticity in financial time series. Neural GARCH is a neural network adaptation of the GARCH 1,1 model in the univariate cas...

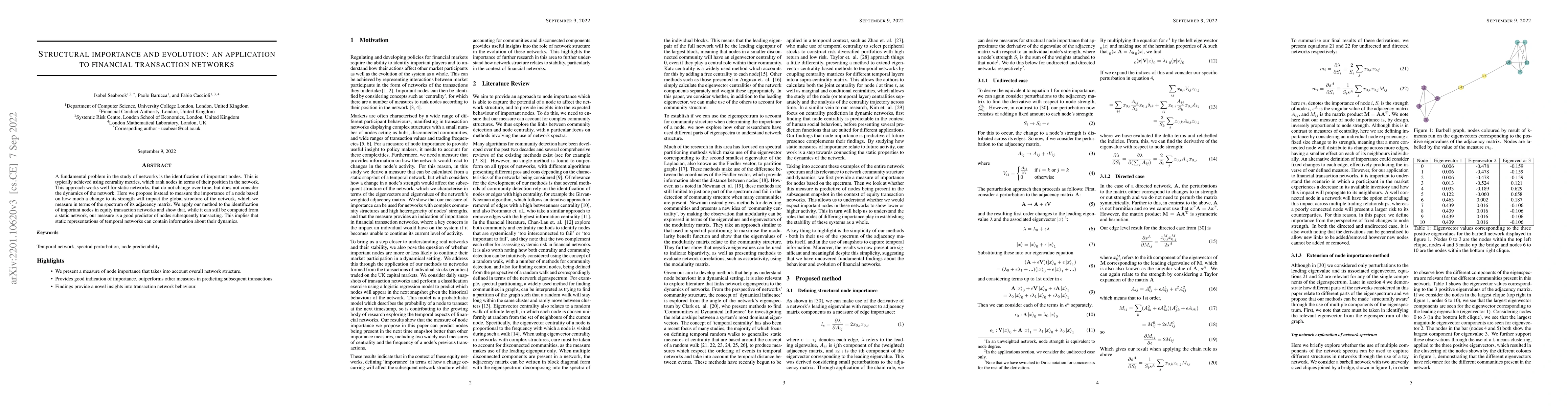

A fundamental problem in the study of networks is the identification of important nodes. This is typically achieved using centrality metrics, which rank nodes in terms of their position in the netwo...

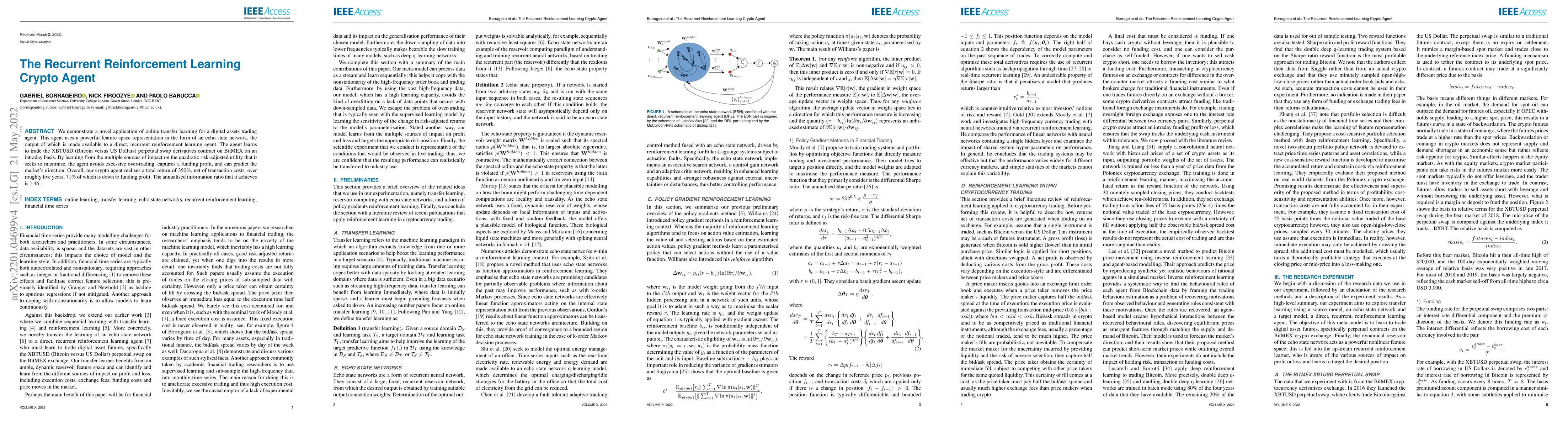

We demonstrate a novel application of online transfer learning for a digital assets trading agent. This agent uses a powerful feature space representation in the form of an echo state network, the o...

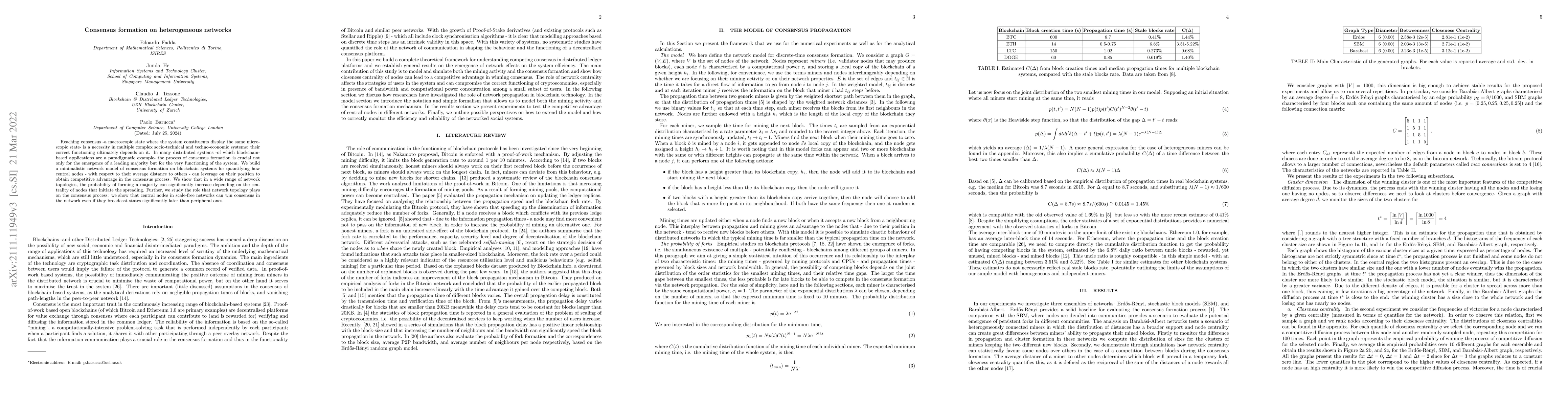

Reaching consensus -- a macroscopic state where the system constituents display the same microscopic state -- is a necessity in multiple complex socio-technical and techno-economic systems: their co...

We explore online inductive transfer learning, with a feature representation transfer from a radial basis function network formed of Gaussian mixture model hidden processing units to a direct, recur...

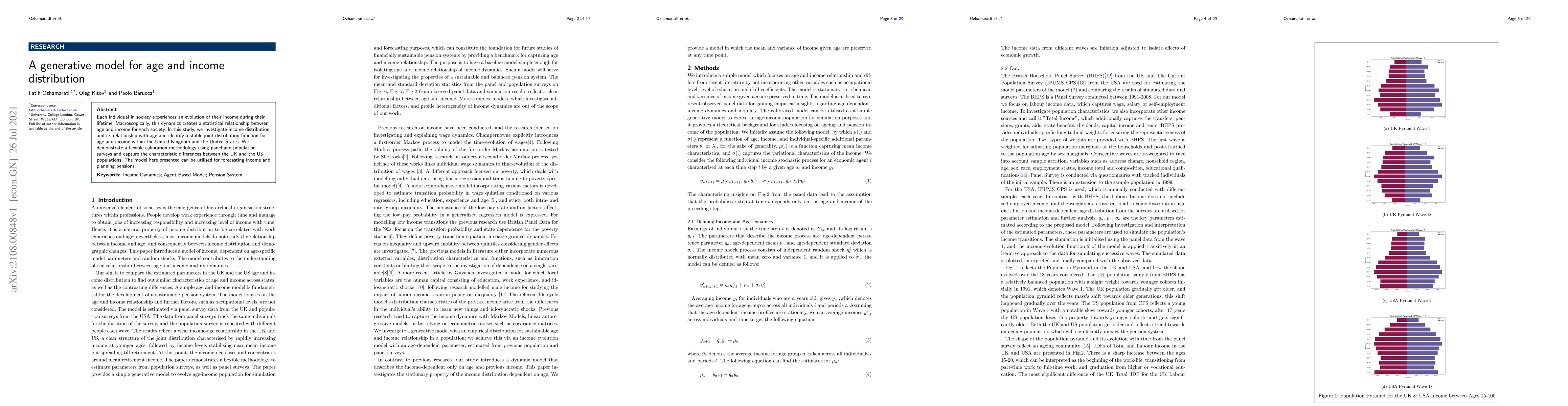

Each individual in society experiences an evolution of their income during their lifetime. Macroscopically, this dynamics creates a statistical relationship between age and income for each society. ...

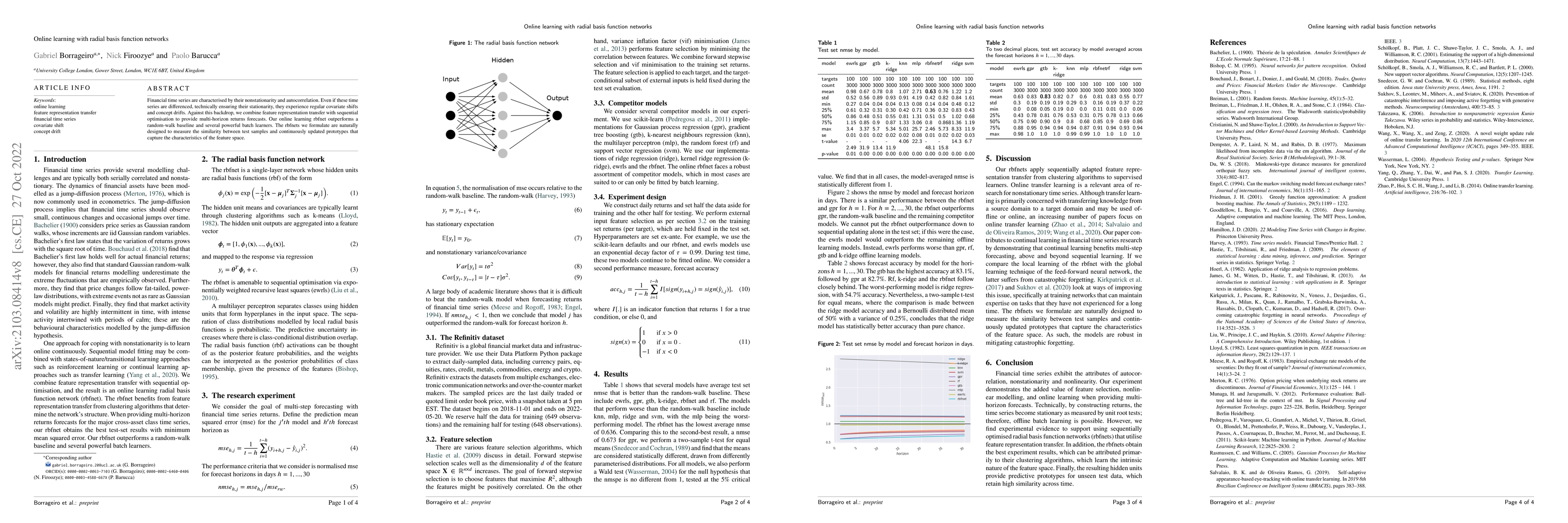

Financial time series are characterised by their nonstationarity and autocorrelation. Even if these time series are differenced, technically ensuring their stationarity, they experience regular cova...

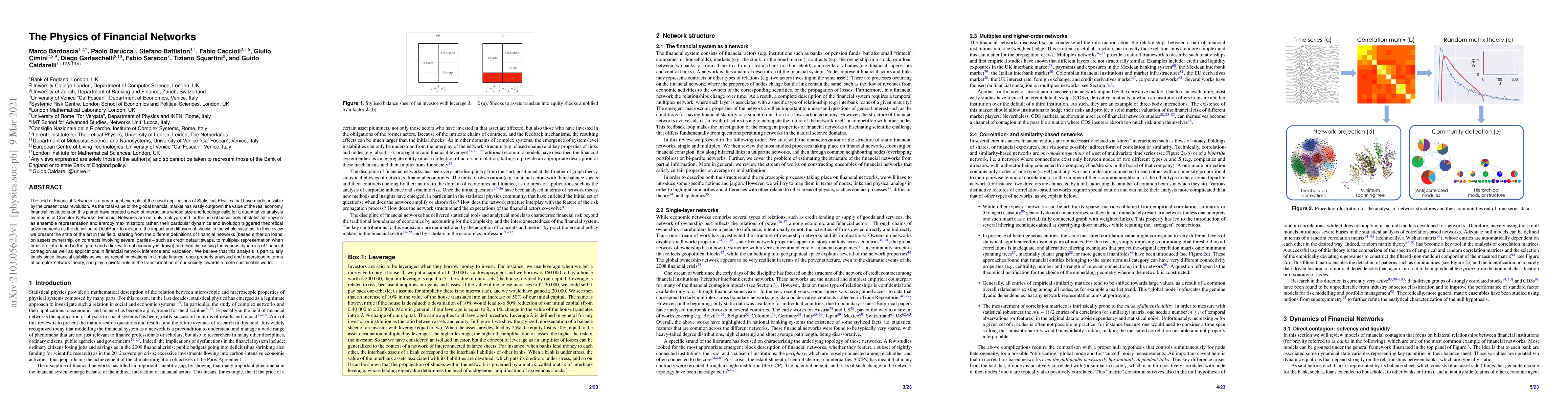

The field of Financial Networks is a paramount example of the novel applications of Statistical Physics that have made possible by the present data revolution. As the total value of the global finan...

To monitor risk in temporal financial networks, we need to understand how individual behaviours affect the global evolution of networks. Here we define a structural importance metric - which we deno...

We introduce simplicial persistence, a measure of time evolution of network motifs in subsequent temporal layers. We observe long memory in the evolution of structures from correlation filtering, wi...

The application of deep learning to time series forecasting is one of the major challenges in present machine learning. We propose a novel methodology that combines machine learning and image proces...

The study of correlated time-series is ubiquitous in statistical analysis, and the matrix decomposition of the cross-correlations between time series is a universal tool to extract the principal pat...

Core-periphery structure is an emerging property of a wide range of complex systems and indicate the presence of group of actors in the system with an higher number of connections among them and a l...

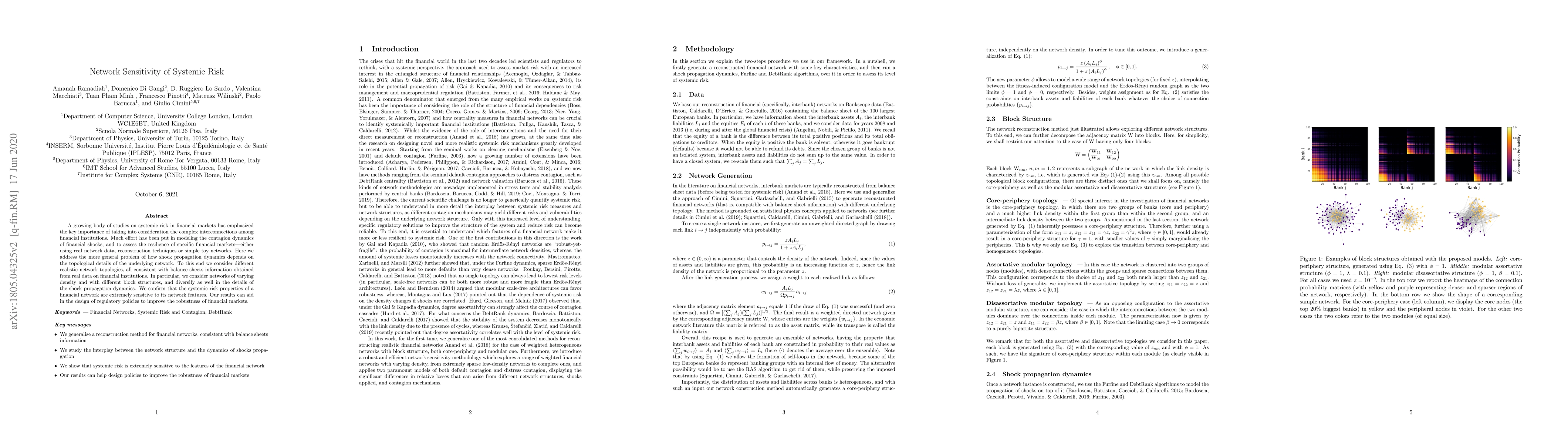

A growing body of studies on systemic risk in financial markets has emphasized the key importance of taking into consideration the complex interconnections among financial institutions. Much effort ...

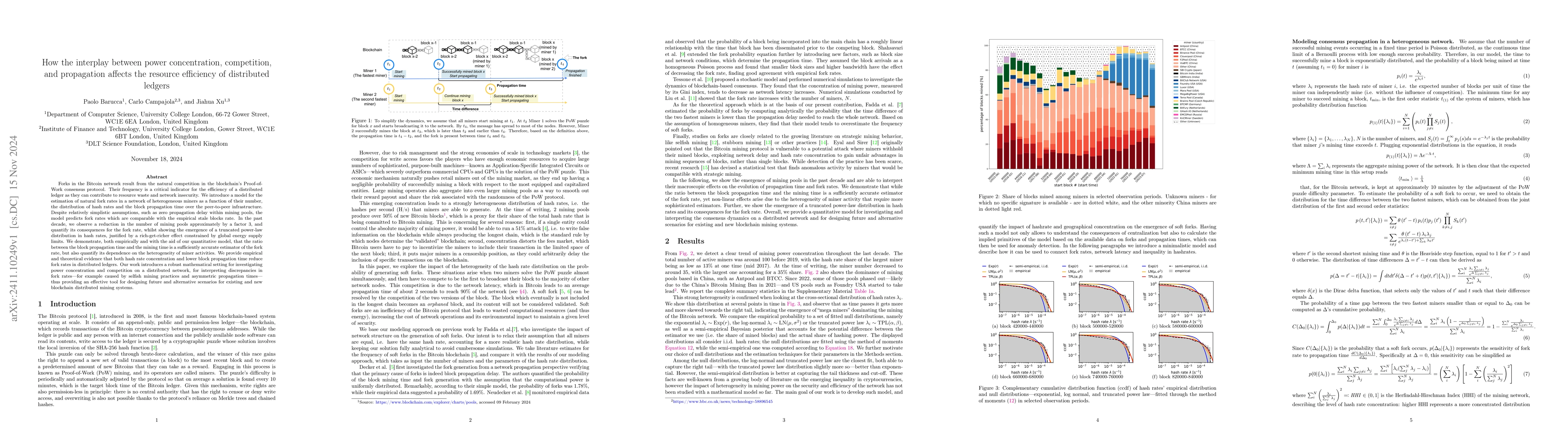

Forks in the Bitcoin network result from the natural competition in the blockchain's Proof-of-Work consensus protocol. Their frequency is a critical indicator for the efficiency of a distributed ledge...

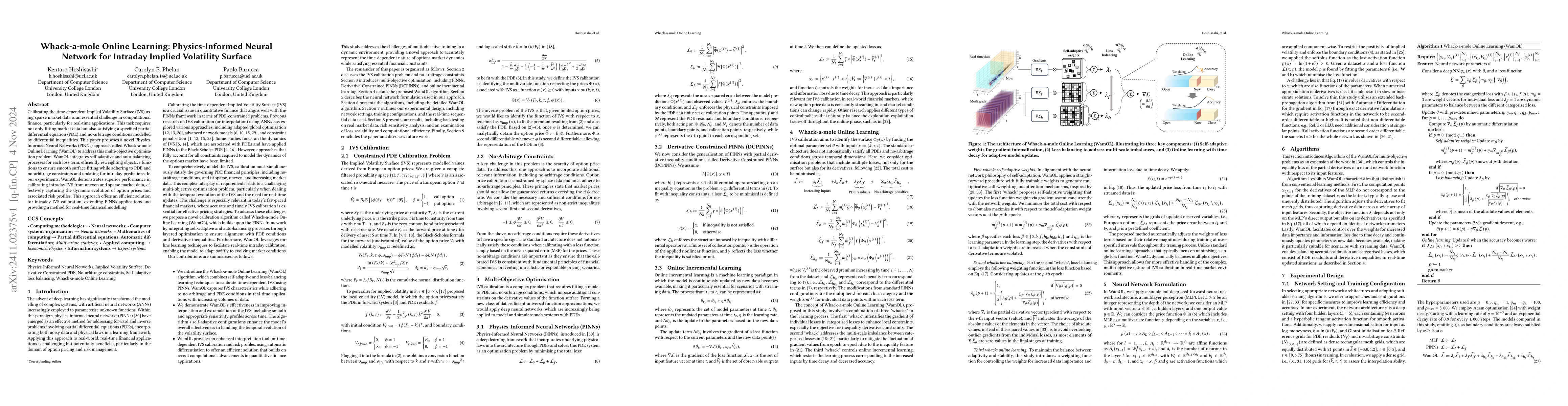

Calibrating the time-dependent Implied Volatility Surface (IVS) using sparse market data is an essential challenge in computational finance, particularly for real-time applications. This task requires...

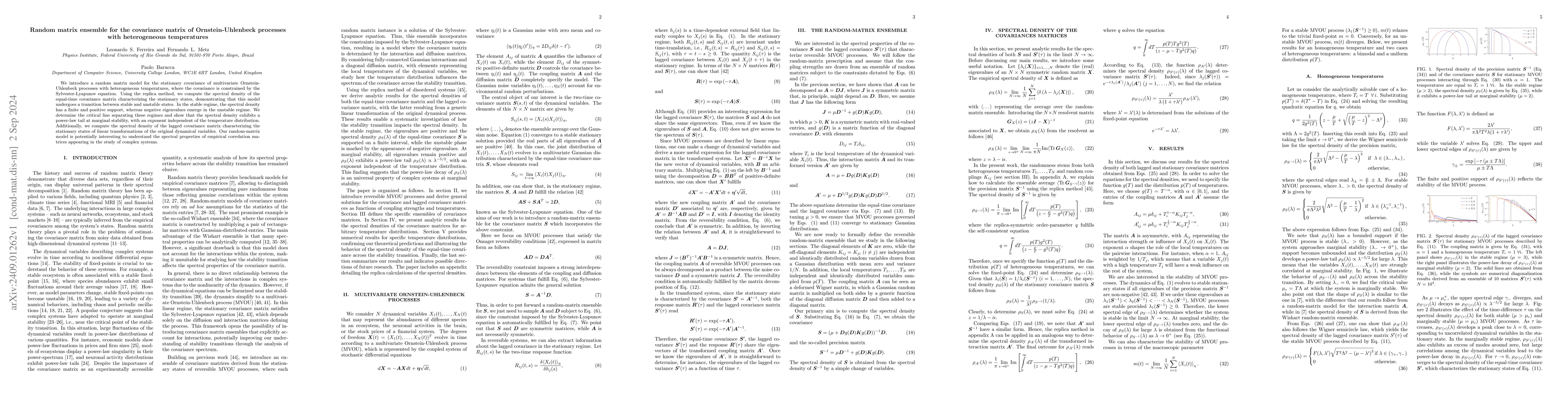

We introduce a random matrix model for the stationary covariance of multivariate Ornstein-Uhlenbeck processes with heterogeneous temperatures, where the covariance is constrained by the Sylvester-Lyap...

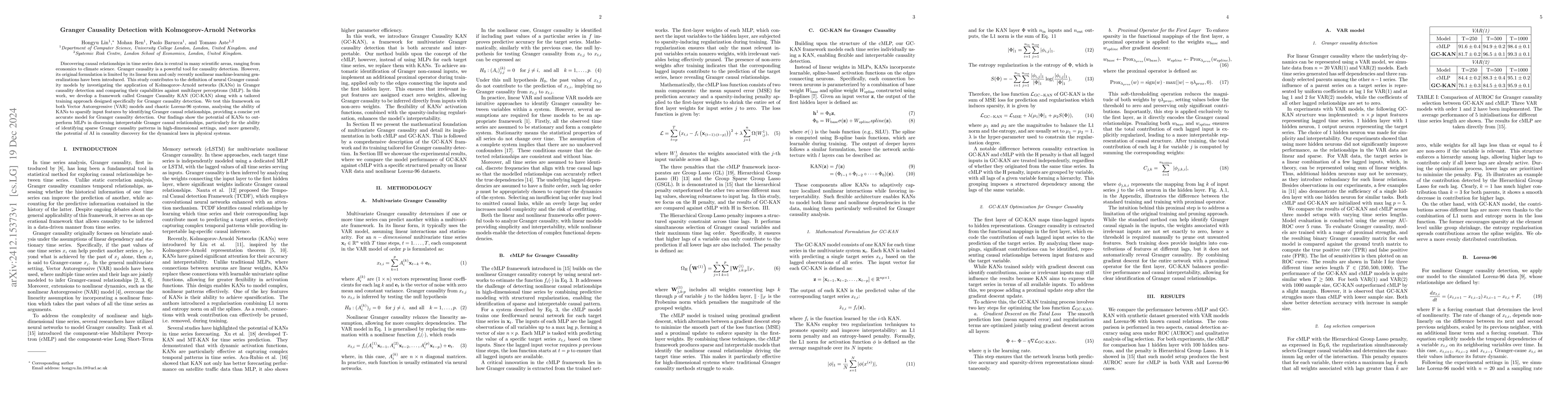

Discovering causal relationships in time series data is central in many scientific areas, ranging from economics to climate science. Granger causality is a powerful tool for causality detection. Howev...

The efficient market hypothesis (EMH) famously stated that prices fully reflect the information available to traders. This critically depends on the transfer of information into prices through trading...

Temporal networks are characterised by interdependent link events between nodes, forming ordered sequences of links that may represent specific information flows in the system. Nevertheless, represent...

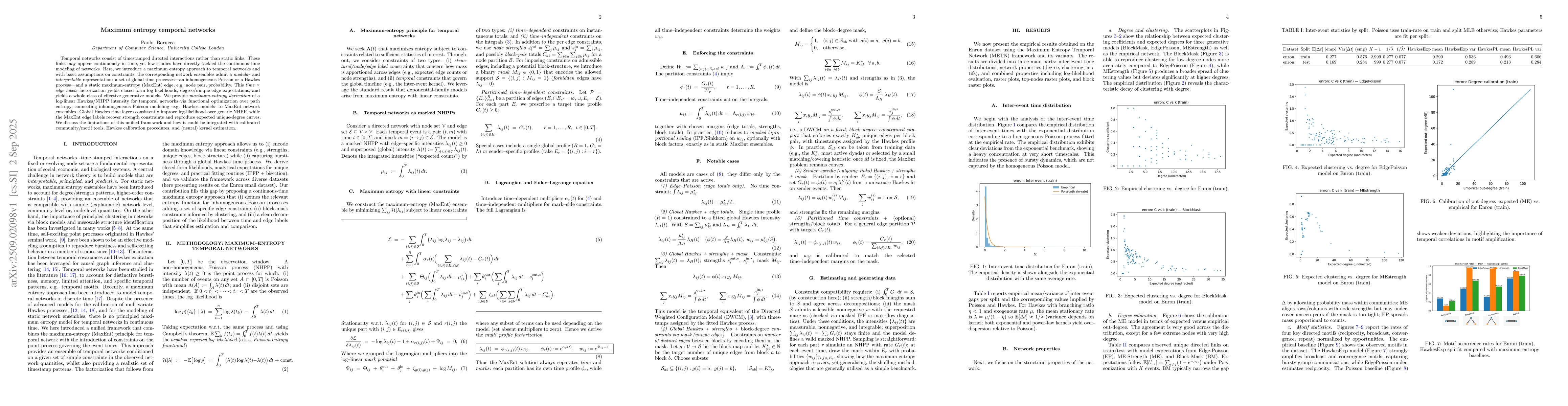

Temporal networks consist of timestamped directed interactions rather than static links. These links may appear continuously in time, yet few studies have directly tackled the continuous-time modeling...

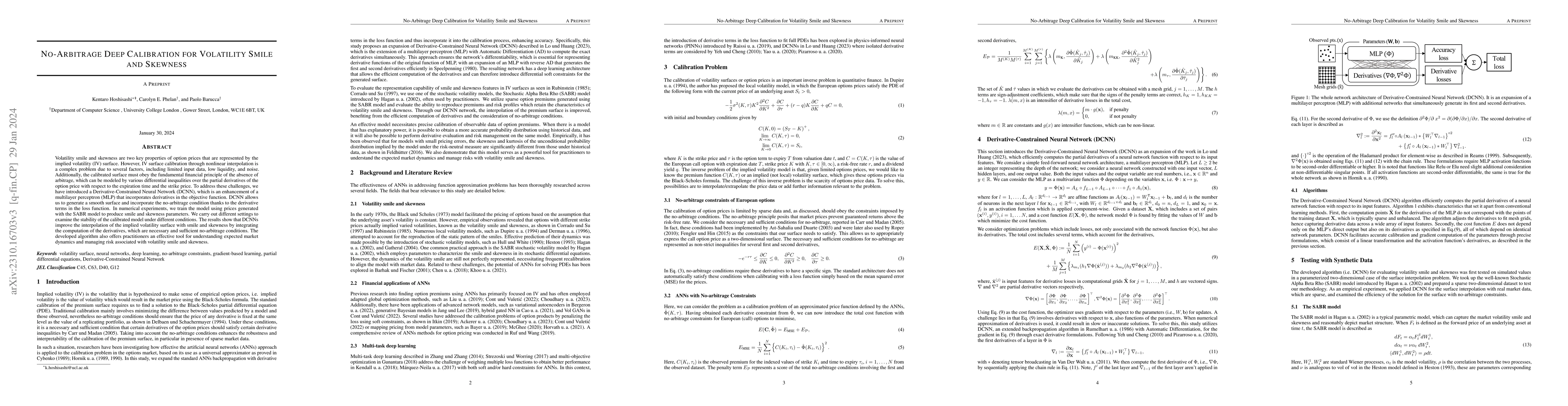

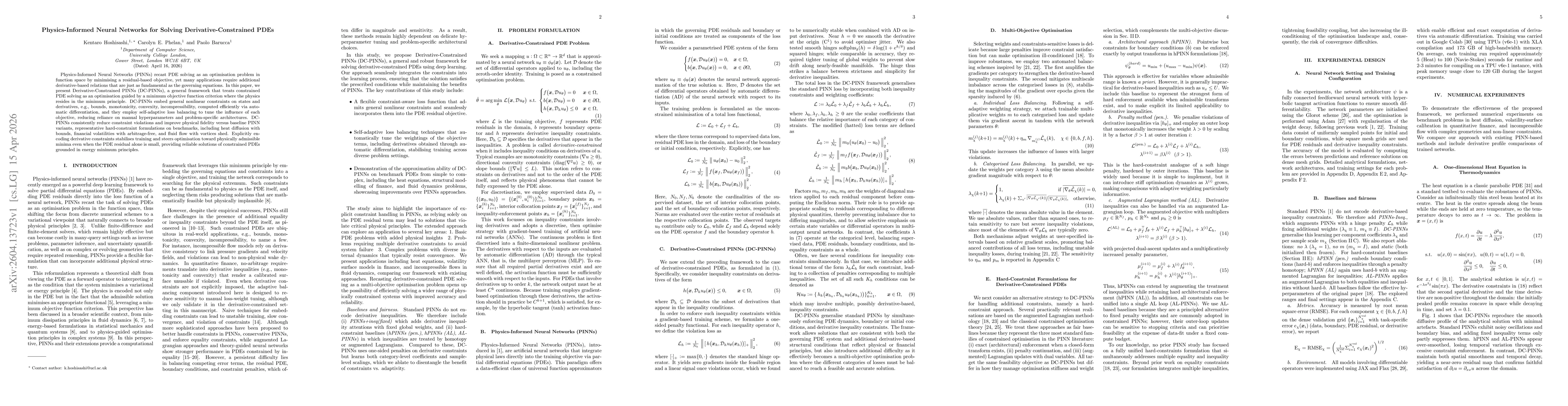

Physics-Informed Neural Networks (PINNs) recast PDE solving as an optimisation problem in function space by minimising a residual-based objective, yet many applications require additional derivative-b...

Many complex systems, including ecosystems, neural circuits, and financial markets, are inferred to operate close to a threshold of instability, at which a small perturbation can propagate across the ...

Hessian spectral properties are a standard tool in analysing neural-network training, with eigenvalues linked to sharpness, generalization, and optimization dynamics. Eigenvalues quantify curvature ma...