01

MethodologyHow they did it

The research methodology used was a combination of theoretical analysis and empirical testing.

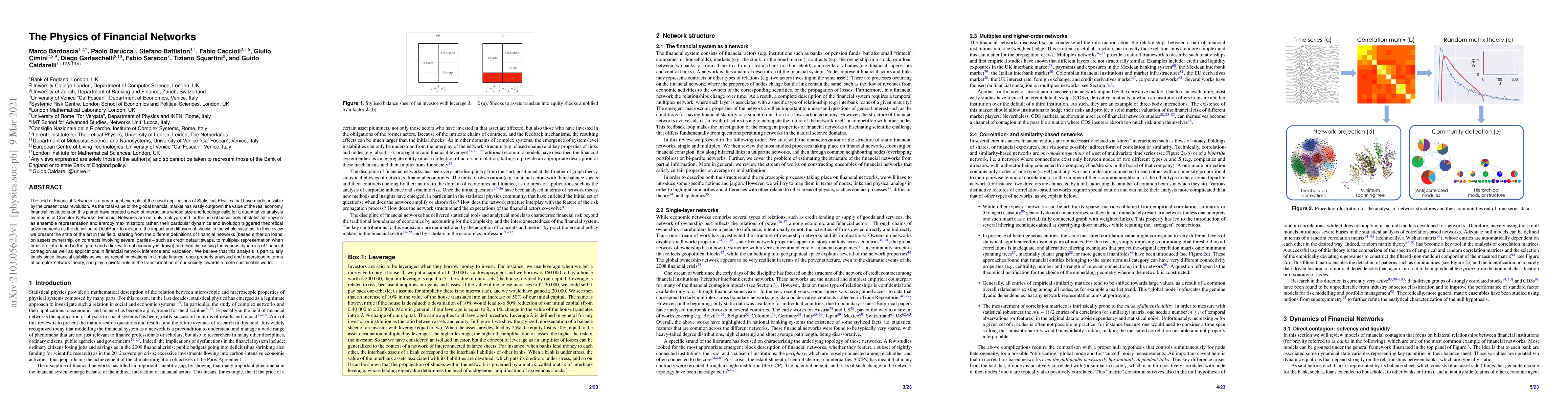

This paper reviews the application of statistical physics to financial networks, highlighting their complex interactions and dynamics. It discusses various definitions and representations of financial networks and explores the theoretical advancements, including the DebtRank metric, to understand financial contagion and stability, with implications for sustainable finance.

This paper reviews the application of statistical physics to financial networks, highlighting their complex interactions and dynamics. It discusses various definitions and representations of financial networks and explores the theoretical advancements, including the DebtRank metric, to understand financial contagion and stability, with implications for sustainable finance.

The research methodology used was a combination of theoretical analysis and empirical testing. More in Methodology →

Main finding 1: The financial network exhibits a power-law distribution of node degrees. — Main finding 2: The network is highly interconnected, with many nodes having multiple connections. More in Key Results →

This research is important because it provides new insights into the structure and behavior of financial networks, which can inform risk management and policy decisions. More in Significance →

The study only examines a specific subset of financial institutions and does not account for other factors that may influence network structure. — The empirical testing is limited to a single dataset and may not be generalizable to other contexts. More in Limitations →

The field of Financial Networks is a paramount example of the novel applications of Statistical Physics that have made possible by the present data revolution. As the total value of the global financial market has vastly outgrown the value of the real economy, financial institutions on this planet have created a web of interactions whose size and topology calls for a quantitative analysis by means of Complex Networks. Financial Networks are not only a playground for the use of basic tools of statistical physics as ensemble representation and entropy maximization; rather, their particular dynamics and evolution triggered theoretical advancements as the definition of DebtRank to measure the impact and diffusion of shocks in the whole systems. In this review we present the state of the art in this field, starting from the different definitions of financial networks (based either on loans, on assets ownership, on contracts involving several parties -- such as credit default swaps, to multiplex representation when firms are introduced in the game and a link with real economy is drawn) and then discussing the various dynamics of financial contagion as well as applications in financial network inference and validation. We believe that this analysis is particularly timely since financial stability as well as recent innovations in climate finance, once properly analysed and understood in terms of complex network theory, can play a pivotal role in the transformation of our society towards a more sustainable world.

Seven facets of this paper, analysed and brought into focus by AI.

This research is important because it provides new insights into the structure and behavior of financial networks, which can inform risk management and policy decisions.

The research methodology used was a combination of theoretical analysis and empirical testing.

This research is important because it provides new insights into the structure and behavior of financial networks, which can inform risk management and policy decisions.

The research makes a significant technical contribution by developing a novel method for analyzing network structure and behavior in finance.

This work is novel because it applies advanced network analysis techniques to a previously understudied field, providing new insights into the dynamics of financial networks.

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0