Whack-a-mole Online Learning: Physics-Informed Neural Network for Intraday Implied Volatility Surface

Publication

Metrics

AI Quick Summary

This paper introduces Whack-a-mole Online Learning (WamOL), a novel Physics-Informed Neural Network (PINN) method for calibrating intraday Implied Volatility Surfaces using sparse market data. WamOL effectively balances loss terms to satisfy partial differential equations and no-arbitrage conditions, demonstrating superior performance in real-time financial modelling.

Paper Preview

Abstract

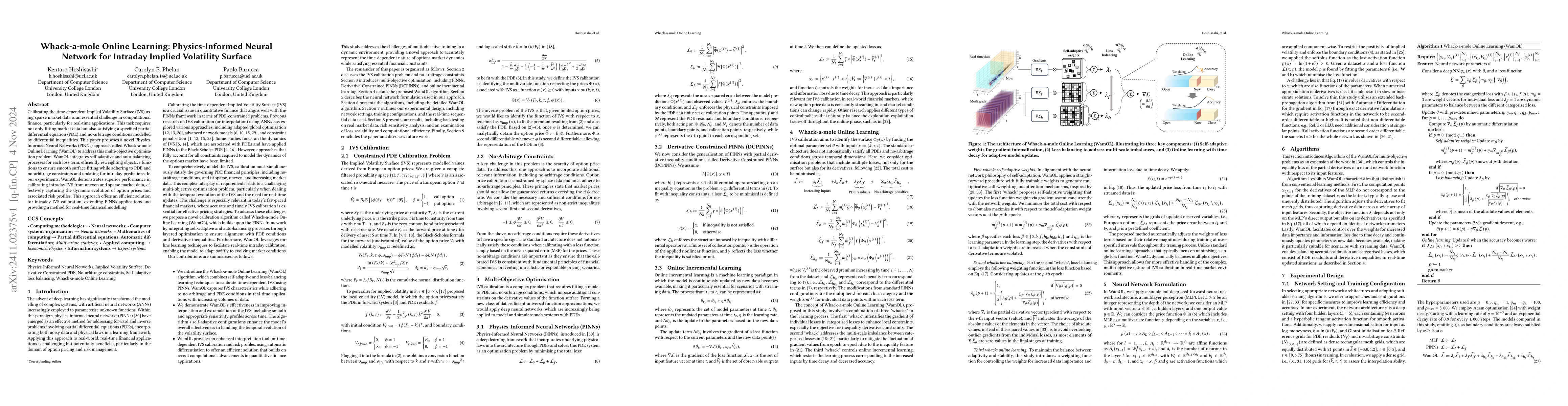

Calibrating the time-dependent Implied Volatility Surface (IVS) using sparse market data is an essential challenge in computational finance, particularly for real-time applications. This task requires not only fitting market data but also satisfying a specified partial differential equation (PDE) and no-arbitrage conditions modelled by differential inequalities. This paper proposes a novel Physics-Informed Neural Networks (PINNs) approach called Whack-a-mole Online Learning (WamOL) to address this multi-objective optimisation problem. WamOL integrates self-adaptive and auto-balancing processes for each loss term, efficiently reweighting objective functions to ensure smooth surface fitting while adhering to PDE and no-arbitrage constraints and updating for intraday predictions. In our experiments, WamOL demonstrates superior performance in calibrating intraday IVS from uneven and sparse market data, effectively capturing the dynamic evolution of option prices and associated risk profiles. This approach offers an efficient solution for intraday IVS calibration, extending PINNs applications and providing a method for real-time financial modelling.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0