Academic Profile

Statistics

Similar Authors

Papers on arXiv

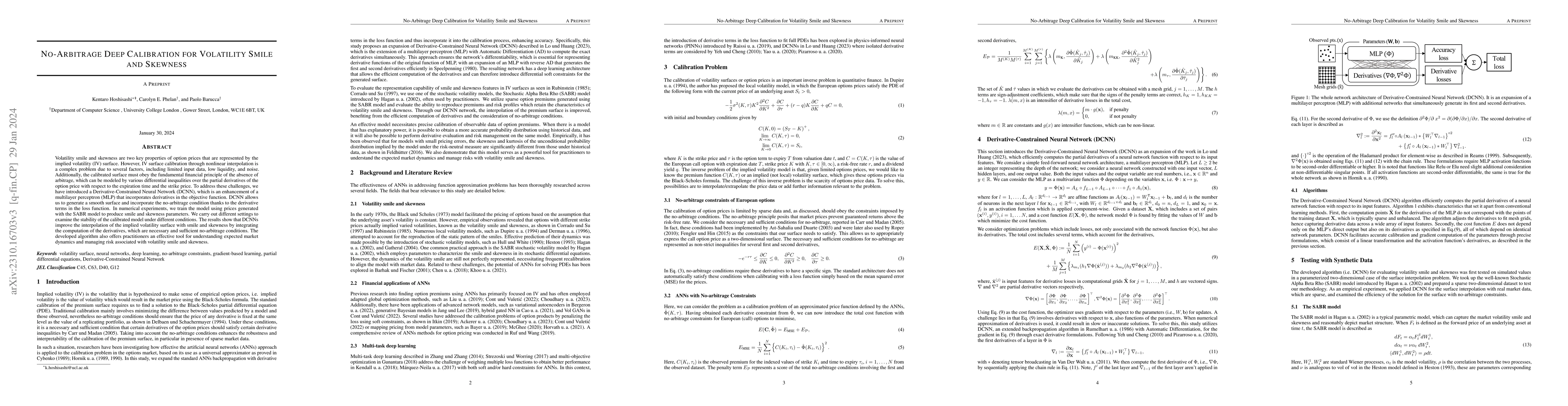

Volatility smile and skewness are two key properties of option prices that are represented by the implied volatility (IV) surface. However, IV surface calibration through nonlinear interpolation is ...

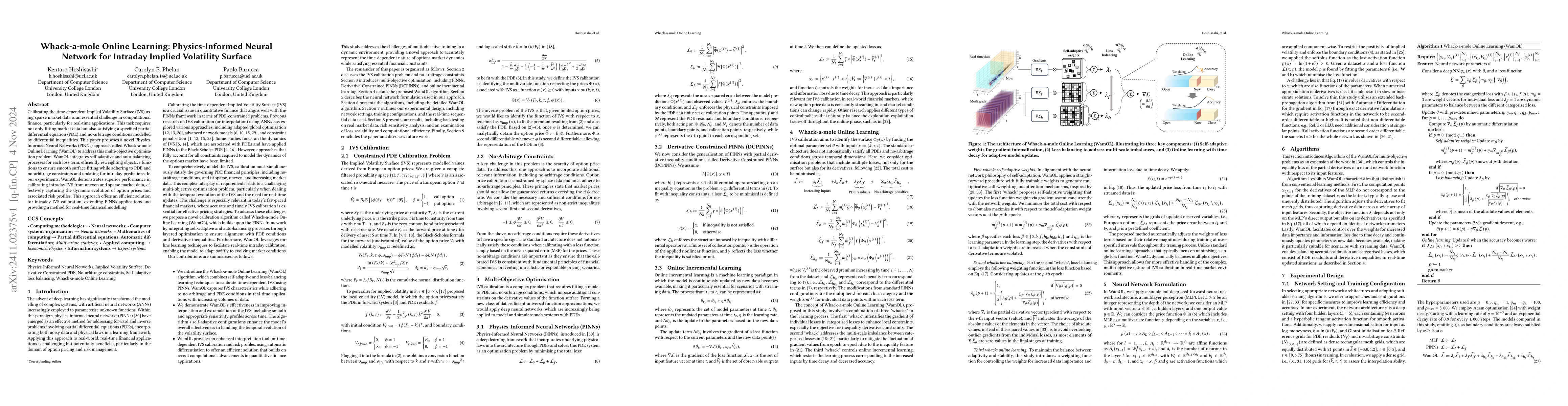

Calibrating the time-dependent Implied Volatility Surface (IVS) using sparse market data is an essential challenge in computational finance, particularly for real-time applications. This task requires...

Physics-Informed Neural Networks (PINNs) recast PDE solving as an optimisation problem in function space by minimising a residual-based objective, yet many applications require additional derivative-b...

Many complex systems, including ecosystems, neural circuits, and financial markets, are inferred to operate close to a threshold of instability, at which a small perturbation can propagate across the ...