Academic Profile

Statistics

Similar Authors

Papers on arXiv

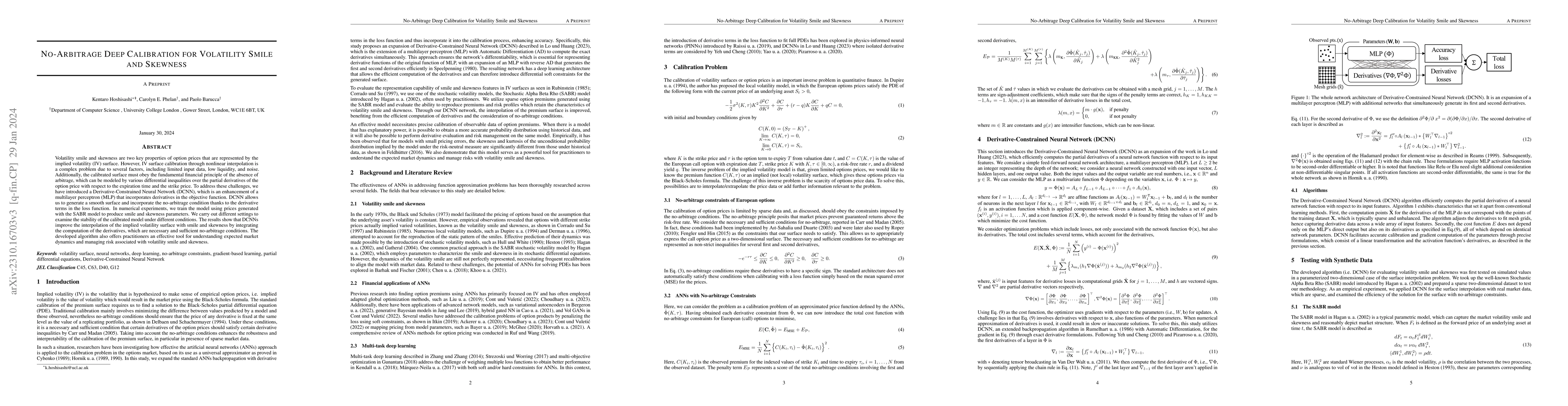

Volatility smile and skewness are two key properties of option prices that are represented by the implied volatility (IV) surface. However, IV surface calibration through nonlinear interpolation is ...

We present new numerical schemes for pricing perpetual Bermudan and American options as well as $\alpha$-quantile options. This includes a new direct calculation of the optimal exercise barrier for ...

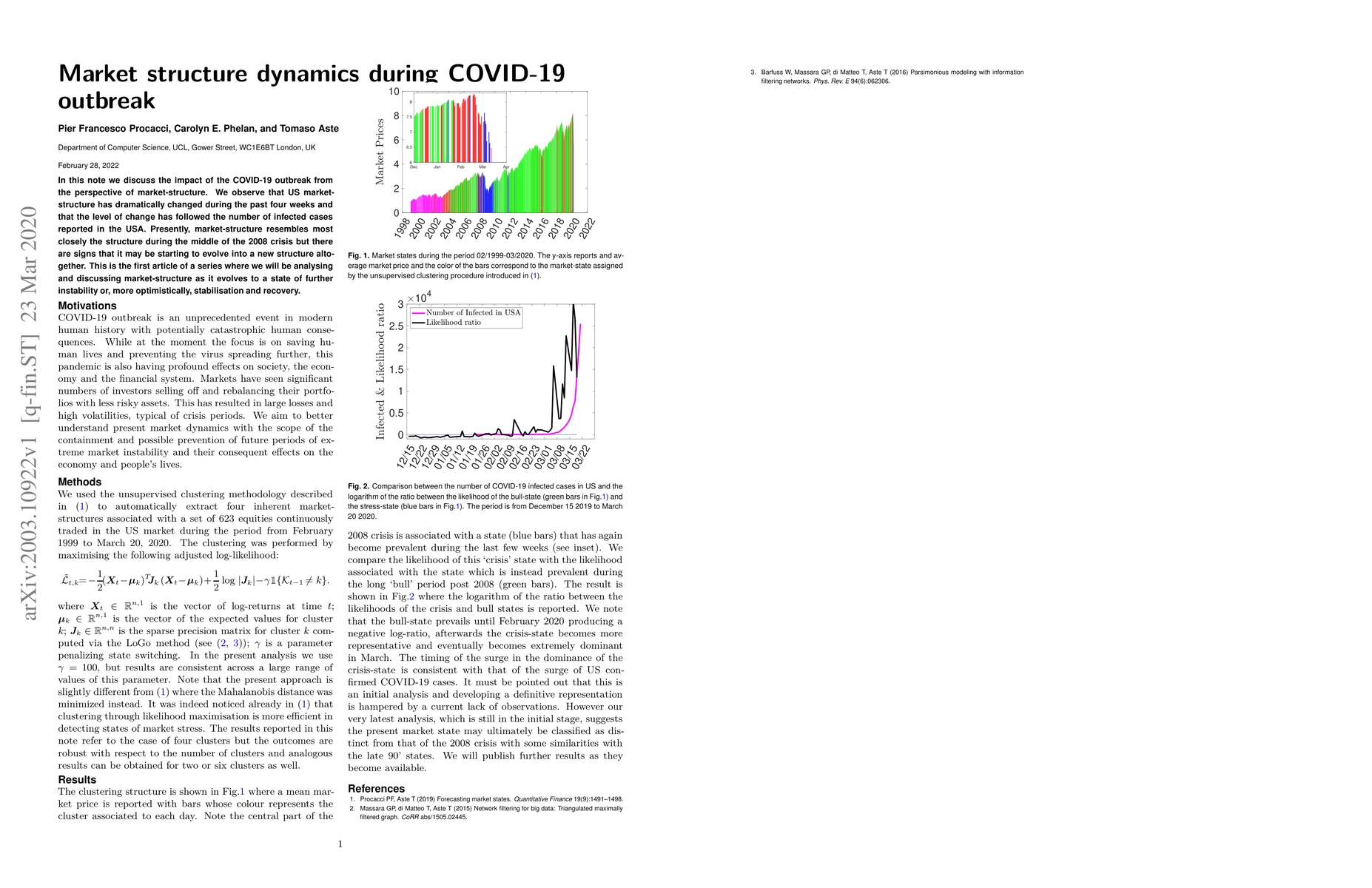

In this note, we discuss the impact of the COVID-19 outbreak from the perspective of the market-structure. We observe that the US market-structure has dramatically changed during the past four weeks...

We show how spectral filters can improve the convergence of numerical schemes which use discrete Hilbert transforms based on a sinc function expansion, and thus ultimately on the fast Fourier transf...

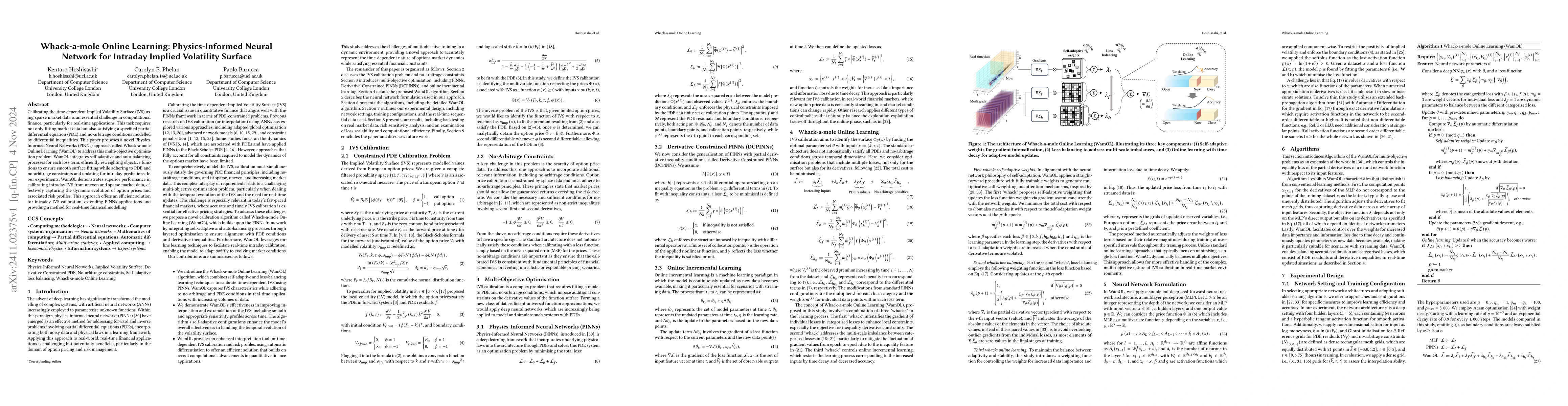

Calibrating the time-dependent Implied Volatility Surface (IVS) using sparse market data is an essential challenge in computational finance, particularly for real-time applications. This task requires...