Academic Profile

Statistics

Similar Authors

Papers on arXiv

Off-policy actor-critic algorithms have shown promise in deep reinforcement learning for continuous control tasks. Their success largely stems from leveraging pessimistic state-action value function...

We introduce Probabilistic Actor-Critic (PAC), a novel reinforcement learning algorithm with improved continuous control performance thanks to its ability to mitigate the exploration-exploitation tr...

Stochastic optimization methods encounter new challenges in the realm of streaming, characterized by a continuous flow of large, high-dimensional data. While first-order methods, like stochastic gra...

Stochastic gradient descent (SGD) and its variants are the main workhorses for solving large-scale optimization problems with nonconvex objective functions. Although the convergence of SGDs in the (...

We propose a novel Bayesian-Optimistic Frequentist Upper Confidence Bound (BOF-UCB) algorithm for stochastic contextual linear bandits in non-stationary environments. This unique combination of Baye...

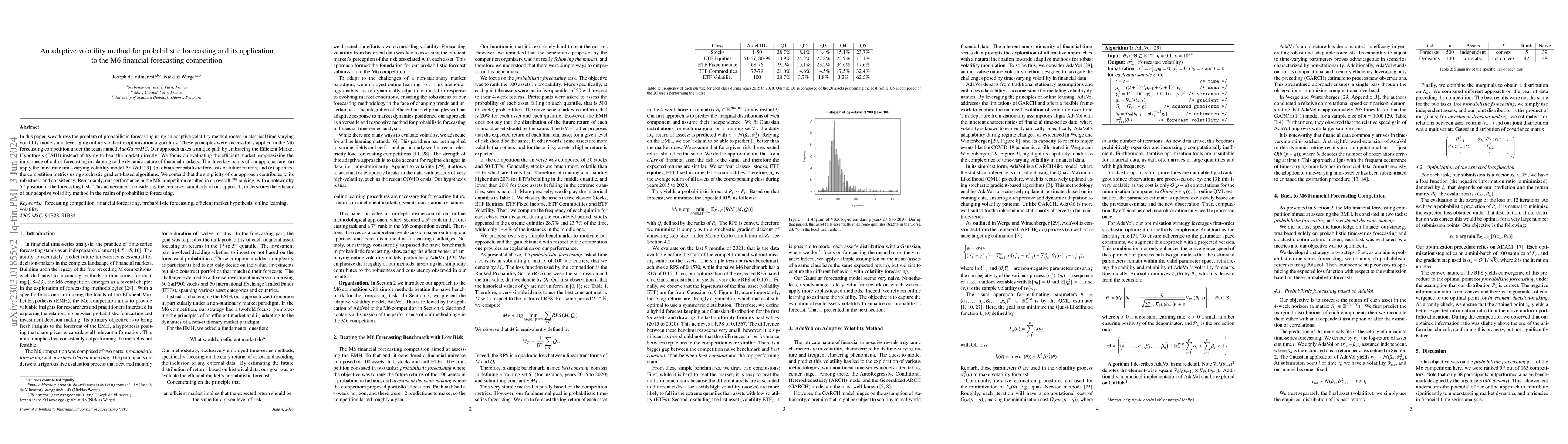

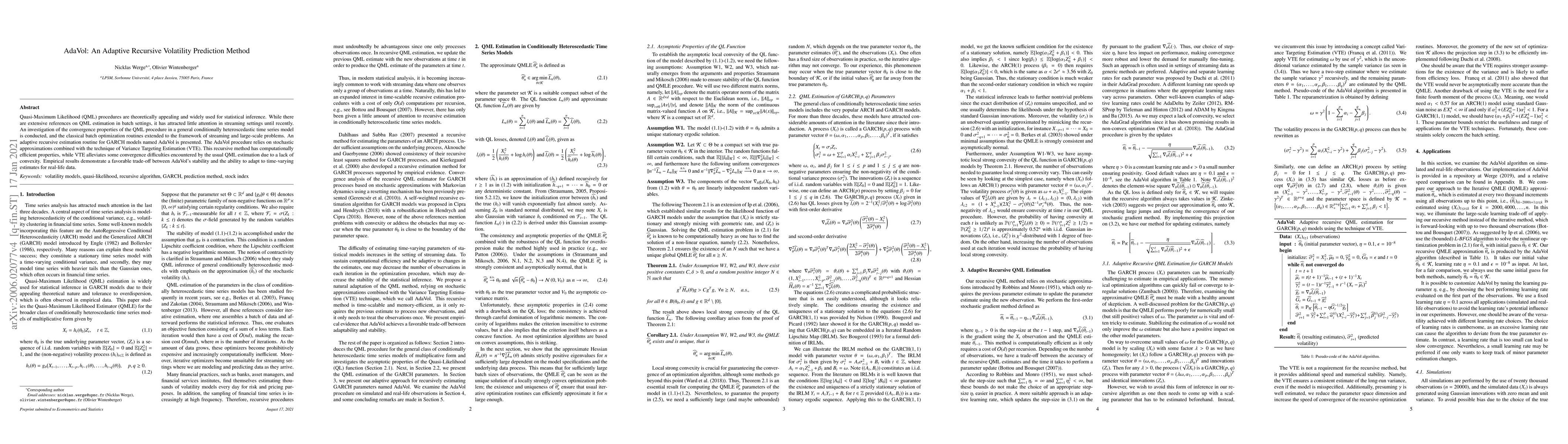

In this paper, we address the problem of probabilistic forecasting using an adaptive volatility method rooted in classical time-varying volatility models and leveraging online stochastic optimizatio...

This paper addresses stochastic optimization in a streaming setting with time-dependent and biased gradient estimates. We analyze several first-order methods, including Stochastic Gradient Descent (...

We introduce a streaming framework for analyzing stochastic approximation/optimization problems. This streaming framework is analogous to solving optimization problems using time-varying mini-batche...

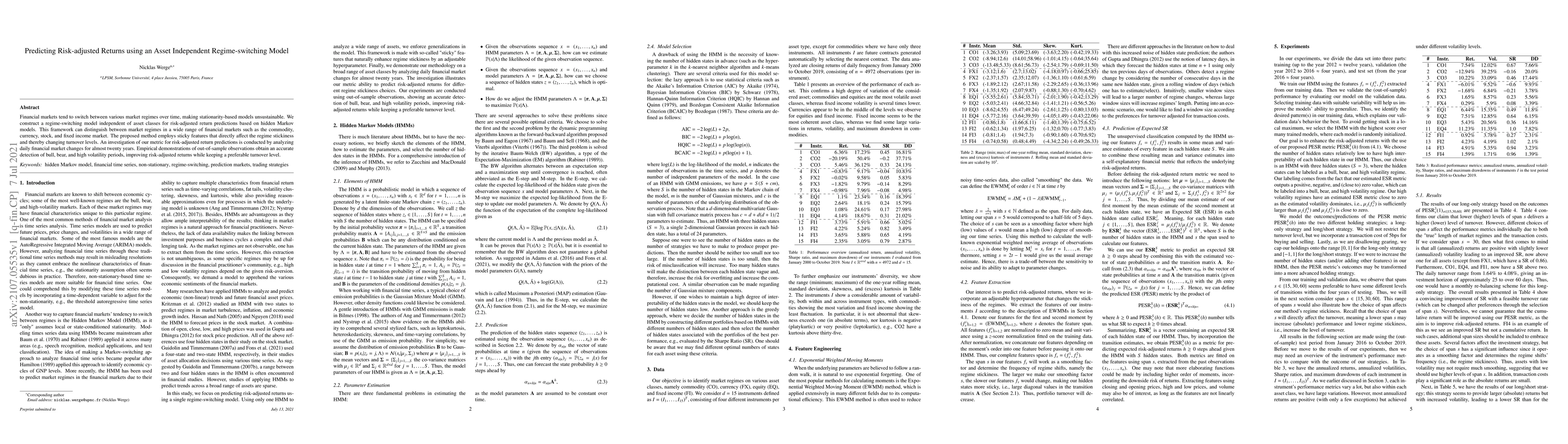

Financial markets tend to switch between various market regimes over time, making stationarity-based models unsustainable. We construct a regime-switching model independent of asset classes for risk...

Quasi-Maximum Likelihood (QML) procedures are theoretically appealing and widely used for statistical inference. While there are extensive references on QML estimation in batch settings, it has attr...

ObjectRL is an open-source Python codebase for deep reinforcement learning (RL), designed for research-oriented prototyping with minimal programming effort. Unlike existing codebases, ObjectRL is buil...

Off-policy reinforcement learning in continuous control tasks depends critically on accurate $Q$-value estimates. Conservative aggregation over ensembles, such as taking the minimum, is commonly used ...